How Much Trading in TFSA Is Considered Excessive?

How much trading is too much in TFSA? When it comes to trading in a Tax-Free Savings Account (TFSA), there is no set limit on how much trading is …

Read Article

A Schedule K1 is a tax document used to report business income, deductions, credits, and losses from partnerships, S corporations, estates, and trusts to the Internal Revenue Service (IRS). It is an important form that provides detailed information about a taxpayer’s share of the partnership or corporation’s income or loss.

Box 20 on Schedule K1 is specifically used to report the taxpayer’s share of the partner or shareholder’s self-employment earnings or losses. This box is typically associated with partnerships or S corporations, where the income or loss may be subject to self-employment taxes.

The amount reported in Box 20 represents the individual partner or shareholder’s share of the business’s net earnings from self-employment activities. This includes income or loss generated by the business that is subject to self-employment tax, such as income from a sole proprietorship or a partnership engaged in a trade or business.

It is important to note that not all partnerships or S corporations will report amounts in Box 20 on Schedule K1. The reporting requirements depend on the nature of the business and the activities it engages in. If a partner or shareholder receives income subject to self-employment tax, it will be reflected in Box 20 along with any deductions or credits associated with that income.

Overall, Box 20 on Schedule K1 provides valuable information for taxpayers and the IRS regarding self-employment earnings or losses. It is crucial to accurately report the information in this box to ensure compliance with tax regulations and to properly calculate and pay self-employment taxes.

Box 20 on Schedule K1 is an important section that provides information about the partner’s share of the liabilities of the partnership. This box is specifically labeled “Partner’s Share of Liabilities at Year-End”. It is essential for partners to understand the details mentioned in this box in order to accurately report their taxable income.

This box reports the partner’s share of partnership liabilities as of the last day of the tax year. It includes both recourse and non-recourse liabilities that the partner is obligated to repay. Recourse liabilities are those for which the partner has personal liability, while non-recourse liabilities are those for which the partner is only responsible to the extent of their share of the partnership. The amount reported in this box is typically used to calculate the partner’s basis in the partnership.

Partners should carefully review the information in Box 20 to ensure that it accurately reflects their share of the partnership liabilities. If there are any discrepancies or errors, it is important to contact the partnership and request the necessary corrections. Failing to report the correct amount of liabilities can result in inaccurate tax calculations and potentially lead to penalties from the IRS.

When preparing your tax return, it is recommended to consult a tax professional who can guide you through the process and ensure accurate reporting of partnership liabilities. They can also help you understand any tax implications that may arise from the information reported in Box 20 on Schedule K1.

Read Also: Is a 1.5 Risk-Reward Ratio Good for Investing or Trading?

The Schedule K1 is a tax form that is used by partnerships, S corporations, and certain other entities to report the income, deductions, and credits allocated to each partner or shareholder. This form is an essential part of the tax reporting process for these types of entities.

Partnerships and S corporations are both pass-through entities, which means that the income, deductions, and credits of the business are passed through to the partners or shareholders, who then report them on their individual tax returns. The Schedule K1 provides a detailed breakdown of this information, allowing each partner or shareholder to accurately report their share of the entity’s taxable income or loss.

The Schedule K1 includes several sections that provide information about different types of income, deductions, and credits. These sections may include items such as ordinary business income, interest income, rental income, foreign income, and capital gains or losses. The specific items reported on the Schedule K1 will vary depending on the nature of the entity and its activities.

In addition to reporting income, deductions, and credits, the Schedule K1 may also include other important information such as the partner or shareholder’s share of the entity’s liabilities, changes in ownership during the tax year, and any other relevant details. This information is used to ensure that each partner or shareholder accurately reports their share of the entity’s financial activity and meets their tax obligations.

It is important for partners and shareholders to carefully review the information reported on their Schedule K1 and use it to accurately complete their individual tax returns. Any errors or discrepancies could result in additional taxes, penalties, or audits. Therefore, it is recommended to seek the assistance of a qualified tax professional to ensure the proper completion of the Schedule K1 and compliance with all applicable tax laws and regulations.

Box 20 on Schedule K1 is an important box that provides information about any foreign transactions that the partnership or S corporation engaged in during the tax year. This box is specifically related to the partner’s or shareholder’s share of the foreign income or loss.

The information reported in Box 20 is essential for the IRS to determine if any foreign tax credits are applicable. Foreign tax credits can help offset the taxes paid to a foreign country against the partner’s or shareholder’s U.S. tax liability.

By accurately reporting the foreign transactions in Box 20, individuals can ensure that they are properly claiming any applicable foreign tax credits and avoiding potential double taxation. It allows the IRS to ensure that the appropriate taxes are being paid on income earned abroad.

Read Also: Exploring the Different Types of Credit Risk: A Comprehensive Guide

Ensuring the correct reporting of Box 20 is crucial to avoid any potential penalties or audits. The IRS closely scrutinizes foreign transactions, and having accurate information in Box 20 can help prevent any issues with the tax return.

In conclusion, Box 20 on Schedule K1 is of great importance as it provides crucial information about foreign transactions and helps determine the eligibility for foreign tax credits. Accurate reporting of Box 20 is essential to avoid penalties and ensure compliance with tax regulations.

Box 20 on Schedule K1 represents the taxpayer’s share of the beginning capital account.

The amount in Box 20 is calculated by taking the taxpayer’s share of the partnership’s beginning capital account and any adjustments made during the tax year.

The purpose of Box 20 is to report the taxpayer’s share of the beginning capital account, which is important for determining the partner’s basis in the partnership.

No, the amount in Box 20 is not included in the partner’s taxable income. It is used to calculate the partner’s basis in the partnership.

It is important for partners to know the amount in Box 20 because it helps determine the partner’s basis in the partnership. The partner’s basis is used to determine their share of partnership liabilities and to calculate any gain or loss on the sale or disposition of their partnership interest.

Box 20 on Schedule K1 is used to report the taxpayer’s share of the total estate tax deduction. This deduction represents the portion of the estate tax paid by the partnership or S corporation that is allocable to the taxpayer. The amount reported in Box 20 reduces the taxpayer’s taxable income for the year.

How much trading is too much in TFSA? When it comes to trading in a Tax-Free Savings Account (TFSA), there is no set limit on how much trading is …

Read Article

3 Technical Analysis Approaches You Need to Know Technical analysis is a crucial tool for investors and traders to make informed decisions in the …

Read Article

Understanding the Significance of USD JPY The USD/JPY currency pair is one of the most important in the forex market. It represents the exchange rate …

Read Article

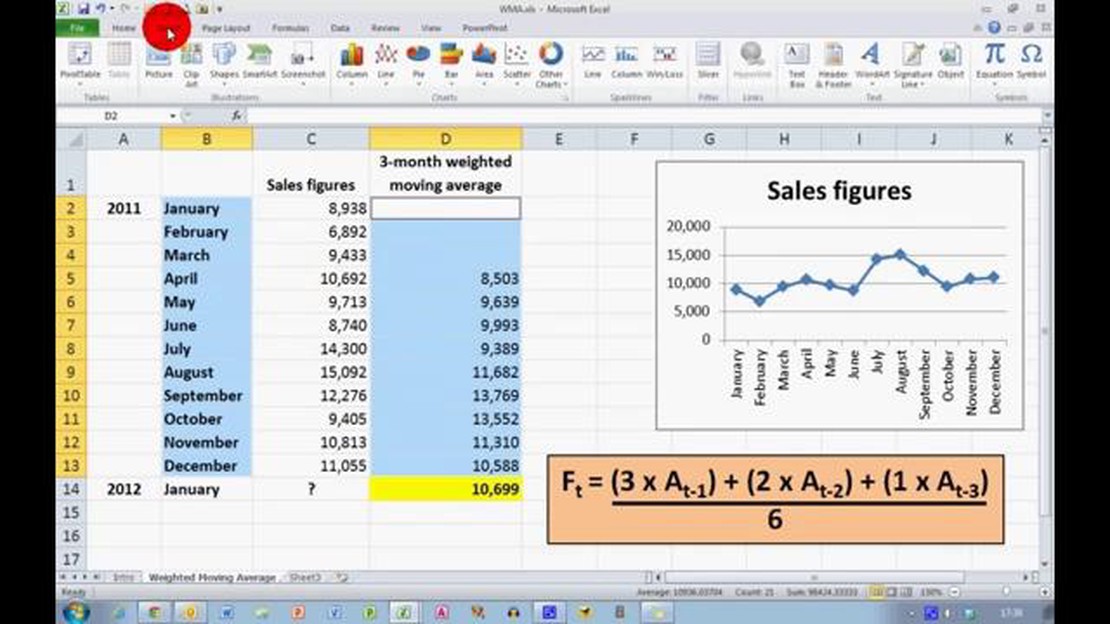

Calculating Weighted Moving Averages in Excel Calculating weighted moving averages in Excel can be a useful tool for analyzing data trends over time. …

Read Article

Best Time Frame for MACD Divergence Divergence analysis is a popular technique used by traders to identify potential trend reversals in the financial …

Read Article

Understanding Stock Options in a Compensation Plan Stock options are a commonly used form of compensation in many modern employment packages. These …

Read Article