What is the exchange rate of ZAR to USD?

ZAR to Dollar Exchange Rate: Current Conversion Rate and Factors Influencing the Value When it comes to international trade and travel, understanding …

Read Article

Employee Stock Ownership Plans (ESOPs) have become increasingly popular as a way for employers to offer their employees a stake in the company’s success. These plans allow employees to own a portion of the company’s stock, providing them with a long-term financial incentive and aligning their interests with those of the company.

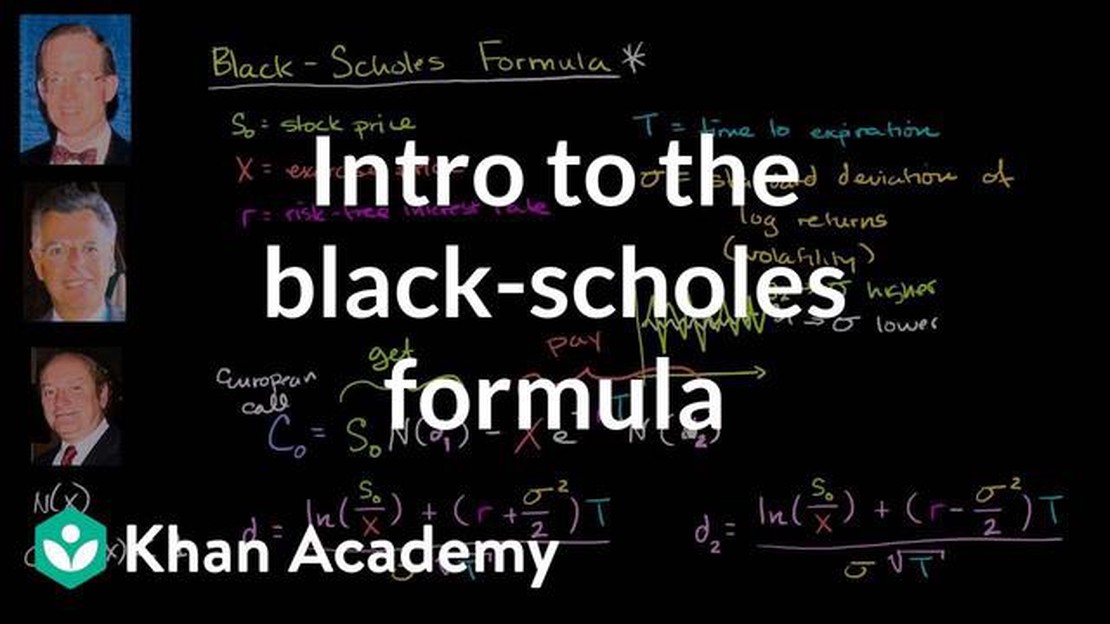

One key aspect of ESOPs is the valuation of the stock options given to employees. The Black-Scholes model is a widely used mathematical tool that helps determine the fair value of these stock options. Developed by economists Fischer Black and Myron Scholes in 1973, the model takes into account various factors such as the stock price, strike price, time to expiration, interest rates, and volatility.

Understanding the Black-Scholes model is essential for both employers and employees involved in ESOPs. This comprehensive guide aims to demystify the model and provide an overview of its key components. We will delve into the assumptions underlying the model, the variables it considers, and the calculations involved in determining the fair value of stock options.

Additionally, this guide will explore the limitations of the Black-Scholes model and the various modifications that have been proposed to address these limitations. It will also discuss practical considerations when implementing the model, such as the choice of inputs and the role of professional valuation experts.

By gaining a deep understanding of the Black-Scholes model for ESOPs, employers and employees can make more informed decisions about stock option grants, better align their interests, and ensure fair and equitable compensation for employees. Whether you are new to ESOPs or seeking to enhance your knowledge, this guide will serve as an invaluable resource for navigating the complexities of the Black-Scholes model.

The Black-Scholes Model is a mathematical model used to calculate the theoretical price of options. It was developed by economists Fischer Black and Myron Scholes in 1973 and is widely used by financial professionals to value options and other derivatives.

The Black-Scholes Model considers several factors to determine the fair value of an option, including the current price of the underlying asset, the strike price of the option, the time remaining until expiration, the risk-free interest rate, and the volatility of the underlying asset.

The model assumes that the price of the underlying asset follows a geometric Brownian motion and that the returns on the asset are normally distributed. It also assumes that there are no transaction costs or restrictions on short selling.

By inputting the relevant variables into the Black-Scholes formula, which is a complex mathematical equation, it is possible to calculate the theoretical price of an option. This theoretical price is often referred to as the “fair value” or “market price” of the option.

While the Black-Scholes Model is widely used and considered a standard tool for pricing options, it does have some limitations. It assumes that the market is efficient and that there are no frictions or taxes. It also assumes constant volatility, which may not necessarily hold true in real-world markets.

Despite these limitations, the Black-Scholes Model provides a valuable framework for pricing options and has had a significant impact on the field of financial economics.

The Black-Scholes model is a widely used mathematical model for calculating the fair value of stock options. It plays a crucial role in the world of Employee Stock Ownership Plans (ESOPs) as it provides a framework for determining the value of stock options granted to employees.

Read Also: How Many Index Options Are There? A Comprehensive Guide

ESOPs are popular compensation plans that give employees the opportunity to become partial owners of the company they work for. In order to determine the value of the stock options granted to employees, it is necessary to have a reliable and accurate valuation method. The Black-Scholes model provides such a method and has become the industry standard for valuing stock options.

By using the Black-Scholes model, companies can ensure that the stock options granted to employees are priced fairly. This is important for maintaining employee morale and motivation, as it assures employees that their stock options have a fair value. It also helps the company attract and retain talent, as the valuation method is recognized and accepted by investors and regulators.

Read Also: Is MACD a Leading Indicator? Discover the Role of MACD in Technical Analysis

Moreover, the Black-Scholes model enables companies to comply with accounting and reporting requirements. In many jurisdictions, including the United States, companies are required to expense the fair value of stock options in their financial statements. The Black-Scholes model provides a standardized way to calculate this value, ensuring compliance with accounting standards.

Additionally, the use of the Black-Scholes model allows companies to assess the cost of stock options and factor it into their overall compensation strategy. By understanding the value of stock options, companies can better manage their compensation expenses and make informed decisions about granting stock options to employees.

In summary, the Black-Scholes model is important for ESOPs as it provides a reliable and accepted method for valuing stock options. It ensures fairness in pricing, helps with compliance, and allows companies to effectively manage their compensation strategies.

When applying the Black-Scholes Model to Employee Stock Option Plans (ESOPs), there are several important factors to consider. These factors play a crucial role in determining the fair value of the options and ensuring accurate financial reporting. Below are the key considerations:

By carefully considering these factors, companies can ensure that the Black-Scholes Model accurately reflects the fair value of their Employee Stock Option Plans. This, in turn, enables them to make informed decisions regarding compensation packages and financial reporting.

The Black-Scholes Model is a mathematical model used to calculate the theoretical value of options. It is based on certain assumptions about the behavior of financial markets and provides a way to estimate the price of financial derivatives.

ESOP stands for Employee Stock Ownership Plan. It is a type of employee benefit plan that allows employees to become owners of company stock. ESOPs are designed to provide employees with a financial stake in the company’s success and can be used as a form of compensation or retirement benefit.

The Black-Scholes Model can be used to estimate the fair value of employee stock options granted under an ESOP. By inputting variables such as the current stock price, exercise price, expected volatility, time to expiration, and risk-free interest rate, the model calculates the theoretical value of the options.

The Black-Scholes Model makes several assumptions, including that the market is efficient, the price of the underlying asset follows a geometric Brownian motion, there are no dividends paid on the underlying asset, there are no transaction costs or taxes, and the risk-free interest rate is constant over the life of the option.

Yes, there are limitations to the Black-Scholes Model. It assumes that stock prices follow a random walk, which may not always be the case in real financial markets. It also assumes constant volatility, which may not hold true in practice. Additionally, the model does not take into account factors such as dividends or changes in interest rates.

ZAR to Dollar Exchange Rate: Current Conversion Rate and Factors Influencing the Value When it comes to international trade and travel, understanding …

Read Article

Understanding the Exponentially Weighted Moving Average Exponentially Weighted Moving Average (EWMA) is a statistical method used to analyze time …

Read Article

The Rule of ADX Indicator: Understanding and Utilizing Its Power The Average Directional Index (ADX) is a popular technical indicator used by traders …

Read Article

Should I Move Out at 22? Consider the Pros and Cons Leaving home and moving out on your own is a major life decision, and one that many young adults …

Read Article

Is low IV good for options? When it comes to trading options, understanding implied volatility (IV) is crucial. IV represents market expectations of …

Read Article

Are ETPs a good investment? Exchange-Traded Products (ETPs) have gained popularity among investors in recent years due to their ease of trading and …

Read Article