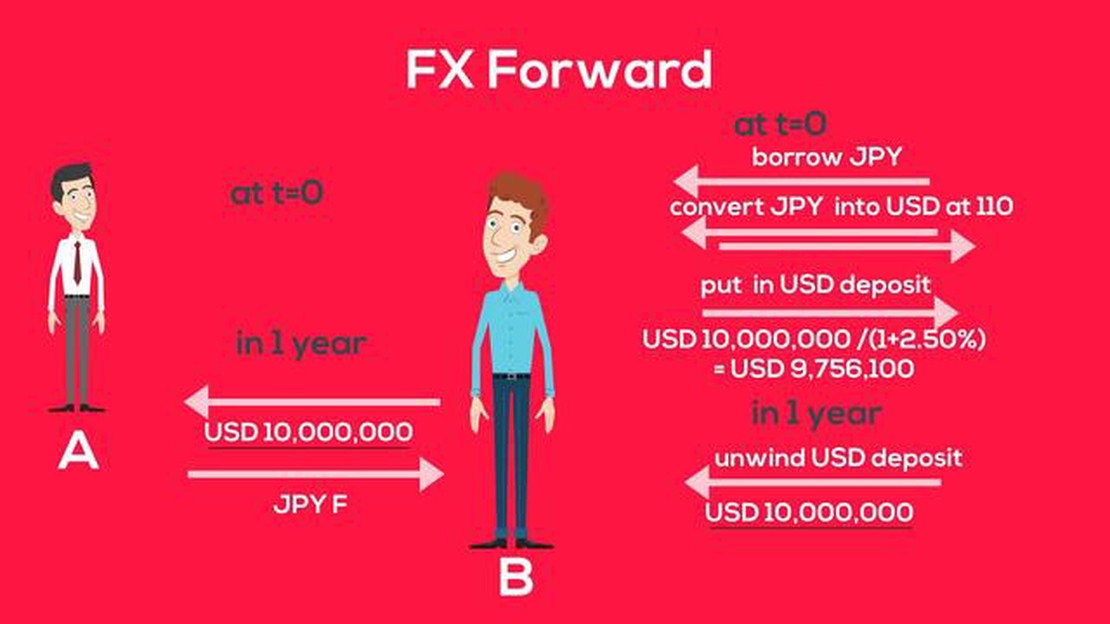

Is an FX forward an OTC derivative?

Understanding whether an FX forward is an OTC derivative An FX forward, also known as a foreign exchange forward or simply a forward contract, is a …

Read Article

Exponentially Weighted Moving Average (EWMA) is a statistical method used to analyze time series data and to forecast future values. It is widely used in finance, economics, and engineering to identify trends and patterns in the data. EWMA puts more weight on recent data points and assigns exponentially decreasing weights to older data points.

The concept of EWMA is derived from the Moving Average (MA) model, which calculates the average of a set of data points over a specific period of time. However, unlike the MA model, which gives equal weight to all data points, the EWMA model assigns weights that decrease geometrically with each successive data point.

This comprehensive guide aims to provide a detailed understanding of how EWMA works, its advantages, and its applications. We will explore the mathematical formula behind EWMA, discuss the importance of choosing the appropriate smoothing factor, and demonstrate how to calculate EWMA values using Python or Excel.

“EWMA is a powerful tool for analyzing time series data because it allows us to put more emphasis on recent data, which is often more relevant in forecasting future values. By assigning exponentially decreasing weights to older data, we can capture changing trends and adapt our forecasts accordingly.”

Whether you are a beginner or an experienced analyst, this guide will equip you with the knowledge and practical skills to effectively use EWMA for analyzing time series data. With its intuitive approach and comprehensive coverage, this guide will serve as a valuable resource for anyone seeking to gain a deeper understanding of this powerful statistical method.

An exponentially weighted moving average (EWMA) is a popular statistical tool used to analyze time series data. It is used to estimate the underlying trend and predict future values based on historical data. The method employs a weighting scheme that assigns more weight to recent observations and less weight to older observations.

The concept of EWMA is based on the assumption that recent data is more relevant in predicting future values compared to older data. This makes it particularly useful in situations where the time series exhibits a trend or pattern that changes over time.

EWMA is often used in finance and economics to analyze stock prices, exchange rates, and other financial variables. It is also commonly used in quality control and process improvement to analyze data from manufacturing processes.

The calculation of EWMA involves assigning weights to each observation in the time series based on a smoothing factor. The smoothing factor determines the rate at which the weights decrease as the observations get older. A higher smoothing factor places more weight on recent observations, while a lower smoothing factor places more weight on older observations.

Read Also: Is MetaTrader available in the USA? Find out now!

To calculate the EWMA, the following formula is applied:

| EMAt = (1 - α) * EMAt-1 + α * Yt |

Where:

The smoothing factor α determines the speed at which the weights decrease. A smaller α gives more weight to older observations and results in a smoother average, while a larger α gives more weight to recent observations and results in a more responsive average.

Overall, the exponentially weighted moving average is a versatile tool that allows analysts to analyze time series data more effectively. By assigning more importance to recent observations, it captures the most relevant information and helps in making accurate predictions.

In the field of finance, the use of mathematical models and statistical analysis is of utmost importance. These tools help professionals make informed decisions and predict future trends in the market. One such tool is the Exponentially Weighted Moving Average (EWMA), which plays a crucial role in analyzing financial data.

EWMA is a type of moving average that assigns weights to current and past observations in a time series. It gives more importance to recent data points while gradually decreasing the weights of older data points. This weighted approach allows for the detection of trends and patterns in the data, making it a valuable tool for financial analysis.

One key application of EWMA in finance is in risk management. Financial institutions, such as banks and investment firms, use EWMA to calculate and monitor risk measures, such as value at risk (VaR). VaR is a statistical measure that quantifies the potential losses that can occur in an investment portfolio. By incorporating EWMA into VaR calculations, institutions can better assess and manage their exposure to various market risks.

Read Also: Can You Make Money on Forex? Unveiling the Earning Potential

Another significant use of EWMA is in forecasting. By analyzing historical financial data using EWMA, analysts can identify trends, patterns, and volatility in the market. This information is then used to make predictions and forecasts about future market movements. Whether it is predicting stock prices, currency exchange rates, or interest rates, EWMA provides a reliable method for forecasting and risk assessment.

In addition to risk management and forecasting, EWMA is also instrumental in technical analysis. Technical analysts use a variety of tools and indicators to study price charts and patterns. EWMA is often used to smooth out price data and filter out short-term fluctuations, allowing analysts to focus on the long-term trends and signals in the market. This helps them make informed decisions about buying or selling assets.

| Benefits of EWMA in Finance: |

|---|

| 1. Improved risk management |

| 2. Accurate financial forecasting |

| 3. Enhanced technical analysis |

| 4. Better decision-making |

In conclusion, the Exponentially Weighted Moving Average is a powerful tool in the field of finance. Its ability to capture trends, patterns, and volatility in financial data makes it invaluable in risk management, forecasting, and technical analysis. By incorporating EWMA into their analytical processes, finance professionals can gain a deeper understanding of the market and make more informed decisions.

An Exponentially Weighted Moving Average (EWMA) is a statistical tool used to calculate the average of a data series with greater emphasis on more recent data points. It assigns weights to each data point, with the weights decreasing exponentially as the data points move further away from the present.

The decay factor in Exponentially Weighted Moving Average (EWMA) is calculated by using a smoothing factor, often denoted as “alpha.” The value of alpha determines how fast the weights decrease as the data points move further away from the present. The formula for calculating the decay factor is: decay factor = 1 - alpha.

There are several advantages of using Exponentially Weighted Moving Average (EWMA) over other averaging methods. Firstly, EWMA gives more weight to recent data points, allowing for better capturing of trends and changes in the data. Secondly, EWMA is computationally efficient and does not require storing all past data points, making it suitable for large datasets. Lastly, EWMA allows for easy adjustment of the level of smoothing by adjusting the value of the decay factor.

Exponentially Weighted Moving Average (EWMA) is widely used in finance for various purposes. It is commonly used to calculate volatility in financial markets, where recent price data points are given more weight in the calculation. Additionally, EWMA is used in risk management to estimate the probability of extreme events based on historical data. It is also employed in portfolio optimization and asset allocation strategies.

Understanding whether an FX forward is an OTC derivative An FX forward, also known as a foreign exchange forward or simply a forward contract, is a …

Read Article

Is Sirius XM stock a good buy? Sirius XM Holdings Inc. (NASDAQ: SIRI) is a leading satellite radio company that offers a wide range of entertainment …

Read Article

Will Twitter Stock Holders Get Paid? Twitter has become one of the most popular social media platforms, with millions of active users worldwide. …

Read Article

How many branches of SBI are there in India? The State Bank of India, also known as SBI, is one of the largest banks in India and has a vast network …

Read Article

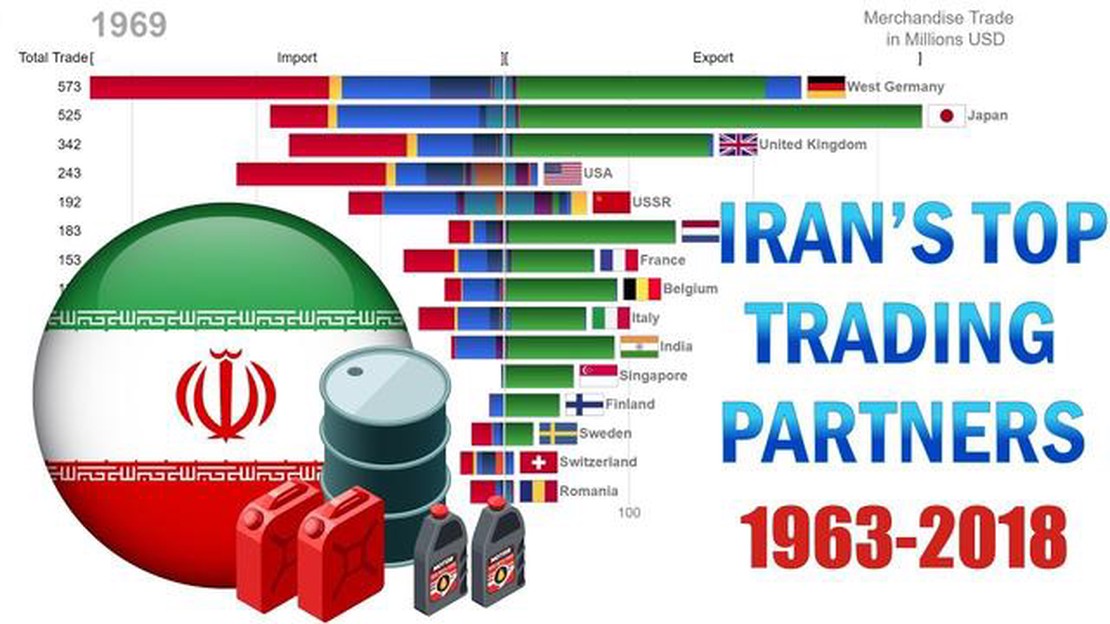

Trading Partners of Iran Iran, a country in the Middle East, has a rich history and culture. It is also known for its thriving trade partnerships with …

Read Article

Is binary options a gamble? Binary options trading has gained significant popularity in recent years, attracting both experienced traders and …

Read Article