Discover Forex Brokers with 100% Deposit Bonus

Best Forex Brokers with 100% Deposit Bonus Forex trading is a popular and potentially profitable investment opportunity, but it can also be a risky …

Read Article

When it comes to options trading, understanding the delta of an option is essential. The delta measures how much the price of an option will change for every one-point move in the underlying asset. It is a crucial component of option pricing and risk management strategies.

The delta of an option can range from 0 to 1 for calls and -1 to 0 for puts. A delta of 0 indicates that the option’s price will not change with a one-point move in the underlying asset, while a delta of 1 or -1 indicates that the option’s price will move in lockstep with the underlying asset.

Calculating the delta of an option involves several factors, including the price of the underlying asset, the strike price of the option, the time to expiration, and the volatility of the underlying asset. The Black-Scholes model is often used to estimate the delta of an option, taking into account these variables.

Delta is a dynamic measure, meaning it can change as the underlying asset price, time to expiration, or volatility changes. Traders and investors use delta as a tool to manage their risk exposure and adjust their options positions accordingly.

Understanding the delta of an option is crucial for options traders and investors. By knowing how much the price of an option is expected to change with a one-point move in the underlying asset, traders can make informed decisions about their options strategies. Whether you are buying or selling options, delta can help you assess potential profits and losses and fine-tune your trading approach.

In options trading, delta is a vital concept that measures how the value of an option changes in relation to changes in the underlying asset’s price. It represents the sensitivity of an option’s price to changes in the underlying asset.

Delta is often expressed as a number between -1 and 1 for call options, and between -1 and 0 for put options. A positive delta means that the option price will increase as the underlying asset’s price rises, while a negative delta means that the option price will decrease as the underlying asset’s price rises.

For example, if a call option has a delta of 0.5 and the underlying asset’s price increases by $1, the option price is expected to increase by $0.50. On the other hand, if a put option has a delta of -0.5 and the underlying asset’s price increases by $1, the option price is expected to decrease by $0.50.

Delta can also be used to determine the probability of an option expiring in-the-money. An option with a delta close to 1 has a high likelihood of expiring in-the-money, while an option with a delta close to 0 has a low likelihood of expiring in-the-money.

Moreover, delta is not constant and can change due to various factors, including changes in the underlying asset’s price, time until expiration, and changes in implied volatility. The rate at which delta changes is known as gamma.

| Delta | Interpretation |

|---|---|

| 0.5 | The option price will increase by half of the underlying asset’s price increase. |

| -0.5 | The option price will decrease by half of the underlying asset’s price increase. |

| 0.9 | The option has a high likelihood of expiring in-the-money. |

| 0.1 | The option has a low likelihood of expiring in-the-money. |

Read Also: Master the art of intraday options trading: Tips, strategies, and basics

It is important for options traders to understand delta and how it can affect their trading strategies. By analyzing the delta of an option, traders can make more informed decisions and manage their risk effectively.

When it comes to managing risk in options trading, delta is an essential tool for traders. Delta measures the sensitivity of an option’s price to changes in the price of the underlying asset. It tells us how much the option’s price will change for a given change in the underlying asset’s price. This makes delta a crucial metric for understanding and controlling risk.

Read Also: Best Phones for Forex Trading in [current year]: Top Smartphones Reviewed

The value of an option’s delta ranges from -1 to 1. A delta value of -1 means the option’s price will move in the opposite direction of the underlying asset’s price. On the other hand, a delta value of 1 means the option’s price will move in lockstep with the underlying asset’s price. It’s important to note that the delta of an option can change over time as the price of the underlying asset fluctuates.

By understanding the delta of an option, traders can assess the risk associated with their positions. A high delta option, such as one with a value close to 1, means that the option’s price will closely track the underlying asset, exposing the trader to significant gains or losses. On the other hand, a low delta option, such as one with a value close to 0, means that the option’s price will be less affected by changes in the underlying asset, resulting in smaller potential gains or losses.

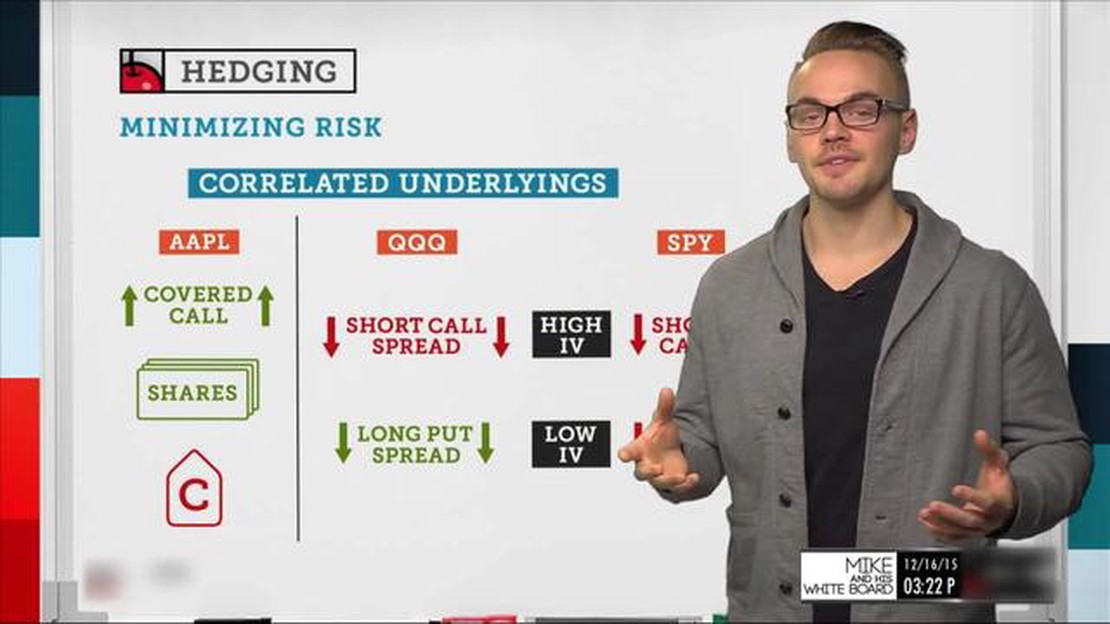

Delta also plays a crucial role in constructing hedging strategies. Traders can use options with a negative delta to hedge against potential losses in their positions. By taking a position in an option with a negative delta, traders can offset some of the risk associated with their existing positions. This allows traders to protect their portfolios from adverse market moves and manage their risk more effectively.

Overall, delta is a powerful tool for risk management in options trading. By understanding and utilizing delta, traders can assess risk, manage positions, and implement hedging strategies to protect their portfolios. It’s important for traders to regularly monitor and adjust their delta exposure as market conditions change to ensure they are effectively managing their risk.

Delta is a measure of the sensitivity of the price of an option to changes in the underlying asset price. It is often used to determine the hedge ratio, which refers to the number of options required to offset the price movements in the underlying asset.

Delta can be calculated by taking the partial derivative of the option price with respect to the underlying asset price. It can also be estimated by using options pricing models, such as the Black-Scholes model. The delta value can range from -1 to 1.

A positive delta value indicates that the option price is expected to increase when the underlying asset price rises. It means that the option is likely to gain value as the underlying asset becomes more valuable.

A negative delta value indicates that the option price is expected to decrease when the underlying asset price rises. It means that the option is likely to lose value as the underlying asset becomes more valuable. Options with negative delta values are considered bearish.

Delta is dynamic and can change over time. It is influenced by various factors, including the time remaining until expiration, the strike price of the option, and the volatility of the underlying asset. As time passes, the delta of an option can approach 1 for in-the-money options and 0 for out-of-the-money options.

Best Forex Brokers with 100% Deposit Bonus Forex trading is a popular and potentially profitable investment opportunity, but it can also be a risky …

Read Article

Understanding the Time Indicator in MT4 In the world of trading, time is a critical factor that can significantly impact decision-making and the …

Read Article

What is Trading Clearing and Settlement? Trading in financial markets involves numerous processes and procedures, and one of the most vital aspects is …

Read Article

Can I use MT4 on Mac? MetaTrader 4 (MT4) is one of the most popular trading platforms used by forex traders around the world. However, MT4 was …

Read Article

Who owns Zorro? Since his creation in 1919 by pulp writer Johnston McCulley, Zorro has captured the imaginations of millions around the world. The …

Read Article

Hedging a Stock with Options: A Practical Example When it comes to the world of investing, risk is inevitable. Whether you are a seasoned trader or a …

Read Article