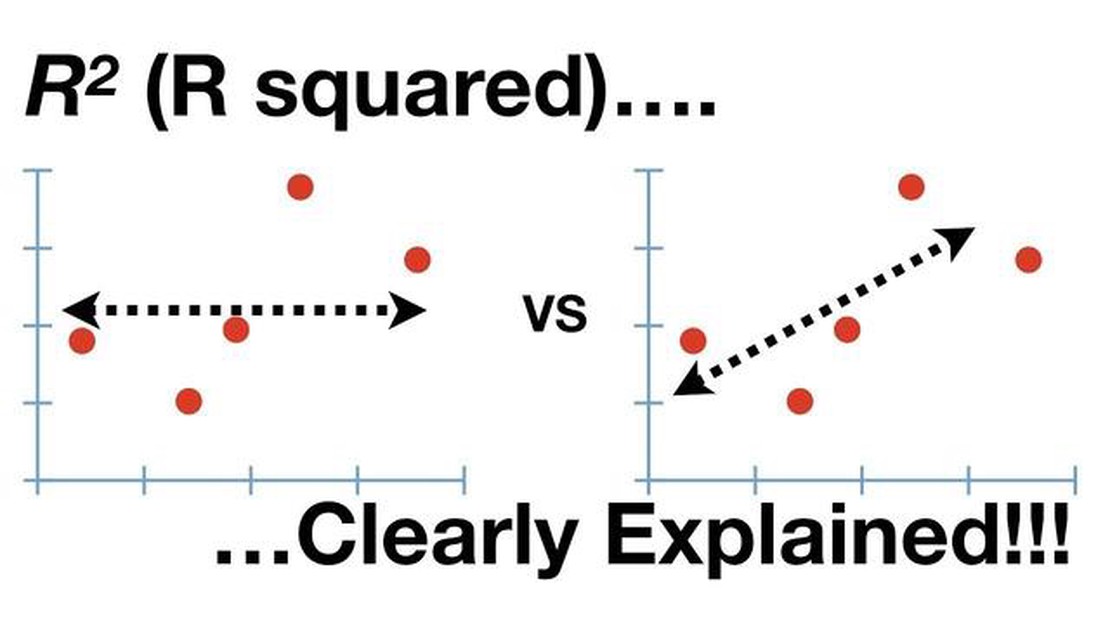

Understanding R2: A Beginner's Guide to the Coefficient of Determination

Understanding R2: A Beginner’s Guide to R2 Regression The coefficient of determination, also known as R2, is a statistical measure used to assess the …

Read Article

When it comes to assessing the worth of an asset or liability, fair value is a key concept in evaluating its true value. Fair value is defined as the price that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants at the measurement date.

Understanding fair value is crucial for various purposes, including financial reporting, investment analysis, and regulatory compliance. By determining the fair value of an asset or liability, stakeholders can make informed decisions regarding its management, valuation, and potential risks.

There are different methods used to determine fair value, such as market approaches, income approaches, and cost approaches. Market approaches involve comparing the asset or liability to similar ones in the market. Income approaches consider the cash flows generated by the asset or liability. Cost approaches focus on the cost to replace the asset or liability.

Examples of items commonly measured at fair value include financial instruments, such as stocks and bonds, as well as real estate properties and derivatives. The fair value of these items is determined by considering factors such as market conditions, risk, and liquidity. It is important to note that fair value is not a static concept, as it can change over time due to changing market conditions or other factors.

Overall, understanding fair value is vital for anyone involved in finance or investment. It provides a standardized and objective measure of an asset or liability’s worth, allowing stakeholders to make informed decisions based on reliable information. By considering various approaches and factors, individuals can determine fair value and ensure transparency and accuracy in financial reporting and analysis.

Fair value is a term used in finance and accounting to determine the worth of an asset or liability. It represents the price that would be received to sell an asset or the price that would be paid to transfer a liability in an orderly transaction between market participants at the measurement date.

Fair value is based on the concept of an arms-length transaction, where buyers and sellers are both knowledgeable and willing to engage in the transaction without duress. It is a subjective measure that relies on assumptions and estimates, rather than objective and verifiable data.

It is important to note that fair value is not always equal to the market price. It can be higher or lower, depending on various factors such as supply and demand, market conditions, and the specific circumstances of the asset or liability being valued.

There are several methods and approaches that can be used to estimate fair value, such as market approaches, income approaches, and cost approaches. Each method has its own set of assumptions and techniques, and the choice of method depends on the nature and characteristics of the asset or liability being valued.

Fair value is often used in financial reporting, particularly in the valuation of financial instruments such as stocks, bonds, derivatives, and other investment assets. It is also used in other areas of finance and accounting, such as in the valuation of businesses, real estate, and intangible assets.

Overall, fair value provides a useful framework for determining the worth of assets and liabilities, but it is important to recognize its limitations and the inherent subjectivity involved in its estimation. It is essential for investors, analysts, and stakeholders to understand the assumptions and methodologies used in determining fair value in order to make informed decisions based on accurate and reliable information.

Fair value is a concept that plays a crucial role in the financial reporting and analysis of companies. It provides a mechanism for determining the true worth of assets and liabilities, which is essential for making informed decisions and evaluating the financial health of an entity.

Read Also: Current Commercial Exchange Rate: Dollar to Real Conversion

One of the primary reasons why fair value is important is because it reflects the current market conditions. This means that the value of an asset or liability is based on what it would be worth if it were sold in an open and competitive market. By using fair value, investors, analysts, and other stakeholders can have a more accurate and reliable picture of an entity’s financial position.

Fair value also enhances transparency and comparability. When assets and liabilities are measured at their fair value, it provides users of financial statements with a clear and consistent basis for evaluating different entities. This allows for better comparisons and more meaningful analysis, which can be especially important for investors looking to allocate their resources effectively.

The use of fair value is particularly significant in complex financial instruments and assets that do not have an active market. These instruments and assets, such as derivatives or real estate, may have unique characteristics that make it challenging to determine their value. Fair value provides a standardized and objective measure that helps address these valuation challenges.

Moreover, fair value is essential for financial reporting compliance. Many accounting standards require companies to measure certain assets and liabilities at their fair value. By doing so, companies can provide accurate and reliable financial information to regulators, investors, and other stakeholders, which promotes trust and confidence in the financial markets.

In conclusion, fair value is of paramount importance in the world of finance. It facilitates accurate valuation, transparency, comparability, and compliance. By using fair value, stakeholders can improve decision-making, assess risks, and gain a better understanding of a company’s financial position.

There are several methods that can be used to determine the fair value of an asset or liability. These methods are typically based on market data and financial analysis, and aim to provide an objective estimate of an asset’s worth. Here are some commonly used methods for determining fair value:

1. Market Approach: This method relies on comparing the asset or liability to similar assets or liabilities that have recently been bought or sold in the market. It takes into consideration factors such as price, terms, and market conditions to determine the fair value.

2. Income Approach: The income approach focuses on the present value of future expected cash flows generated by the asset or liability. This method takes into account factors such as expected earnings, growth rates, and risk to determine the fair value.

Read Also: Learn all about NIFTY option trading: a comprehensive guide

3. Cost Approach: The cost approach determines the fair value by considering the current replacement cost of the asset or liability. It takes into account factors such as current market prices, depreciation, and obsolescence to estimate the fair value.

4. Market Participant Approach: This approach considers the perspective of a hypothetical market participant and takes into account their knowledge, motivations, and expectations. It aims to determine the fair value based on what a rational participant would be willing to pay or receive for the asset or liability.

5. Option Pricing Model: This method uses an option pricing model, such as Black-Scholes, to determine the fair value of an asset or liability that has option-like features, such as an embedded derivative. It takes into account factors such as volatility, time to expiration, and interest rates to estimate the fair value.

It’s important to note that the choice of method may depend on the specific circumstances and nature of the asset or liability being valued. Additionally, fair value estimates are subject to judgment and can vary based on the assumptions and inputs used in the valuation process.

Fair value is the estimated price at which an asset or liability can be sold or settled between knowledgeable, willing parties in an arm’s length transaction.

Fair value can be determined through various methods, including market prices, market comparables, third-party valuations, and financial models.

Fair value is important as it provides an objective measure of the worth of an asset or liability and is used in financial reporting to ensure transparency and comparability.

Yes, fair value can change over time due to various factors, such as market conditions, changes in supply and demand, and changes in the underlying fundamentals of the asset or liability.

An example of fair value is the price at which a share of a publicly traded company is traded on a stock exchange.

Fair value is the estimated price at which an asset or liability would be exchanged in an orderly transaction between market participants on the measurement date.

Fair value is determined based on a combination of factors, including market prices, observable inputs, and valuation techniques. It is often estimated using financial models and may require judgment and assumptions from professionals.

Understanding R2: A Beginner’s Guide to R2 Regression The coefficient of determination, also known as R2, is a statistical measure used to assess the …

Read Article

Aspen Hysys Users: Who Benefits from this Simulation Software? Aspen Hysys is a powerful process simulation software used by engineers and researchers …

Read Article

Calculate MAD: A Step-by-Step Guide When it comes to analyzing data, the Mean Absolute Deviation (MAD) is a commonly used statistic that measures the …

Read Article

Is trading options legal in Canada? Options trading is an increasingly popular investment strategy that allows individuals to speculate on the price …

Read Article

Understanding the Concept of a Call in Forex Trading In the world of forex trading, there are several key concepts that every trader should be …

Read Article

How to Cash Out from FX Royale So, you’ve had a successful run at FX Royale and now it’s time to cash out your winnings. Congratulations! Here is a …

Read Article