The Downside of Heiken Ashi: Understanding the Disadvantages

What are the disadvantages of Heiken Ashi? Heiken Ashi is a popular charting technique used by traders to predict market trends and make informed …

Read Article

An S corporation, also known as an S corp, is a type of business structure that provides certain tax advantages to its shareholders. Unlike a C corporation, which is subject to double taxation, an S corporation allows its income to be passed through to its shareholders, who then report it on their personal tax returns. However, not everyone is eligible to hold shares in an S corporation.

In order to be eligible to hold shares in an S corporation, an individual must be a legal resident or citizen of the United States. Non-resident aliens, foreign corporations, partnerships, and certain other types of entities are generally not allowed to be shareholders in an S corporation. However, there are a few exceptions to this rule.

One exception is for certain types of trusts, such as qualified subchapter S trusts (QSSTs) and electing small business trusts (ESBTs), which may be eligible to hold shares in an S corporation. Additionally, an S corporation can have certain types of estates as shareholders, such as the estate of a deceased shareholder.

It’s worth noting that there are also certain restrictions on the number and type of shareholders that an S corporation can have. For example, an S corporation cannot have more than 100 shareholders, and all shareholders must be individuals, estates, certain types of trusts, or tax-exempt organizations.

Not everyone is eligible to hold shares in an S corporation. In order to be eligible, a person or entity must meet certain requirements:

3. Residency status: Shareholders must be U.S. citizens or resident aliens. Non-resident aliens are not eligible to hold shares in an S corporation.

4. Shareholder consent: Shareholders must consent to being treated as an S corporation and must sign a consent form, which is typically included in the company’s articles of incorporation.

5. One class of stock: An S corporation can only have one class of stock. This means that all shareholders must have the same rights and privileges regarding voting, dividends, and liquidation proceeds.

3. Residency status: Shareholders must be U.S. citizens or resident aliens. Non-resident aliens are not eligible to hold shares in an S corporation.

4. Shareholder consent: Shareholders must consent to being treated as an S corporation and must sign a consent form, which is typically included in the company’s articles of incorporation.

5. One class of stock: An S corporation can only have one class of stock. This means that all shareholders must have the same rights and privileges regarding voting, dividends, and liquidation proceeds.

Read Also: Understanding OpenTable's Additional Seating Options: A Comprehensive Guide

It is important to note that these eligibility requirements may vary depending on the jurisdiction and specific circumstances. Additionally, additional requirements may apply for certain types of shareholders or entities. It is recommended to consult with a legal or tax advisor for specific guidance.

In order to hold shares in an S corporation, there are certain citizenship and residency requirements that must be met. The shareholders of an S corporation must be individuals who are either citizens or legal residents of the United States. This means that foreign individuals who do not hold U.S. citizenship or residency status are generally not eligible to hold shares in an S corporation.

It is important for shareholders to provide proof of their citizenship or residency status in order to comply with the eligibility requirements. This may include providing documentation such as a valid U.S. passport or green card.

Additionally, non-U.S. citizens who have been granted an individual taxpayer identification number (ITIN) by the Internal Revenue Service (IRS) may also be eligible to hold shares in an S corporation. However, it is recommended that individuals consult with a qualified tax professional to ensure compliance with any additional requirements or restrictions that may apply.

Overall, the citizenship and residency requirements for holding shares in an S corporation are in place to ensure that only individuals who have a legal presence in the United States can benefit from the tax advantages and limited liability offered by this type of business structure.

While an S corporation offers numerous advantages to shareholders, there are certain ownership restrictions that must be adhered to. Understanding these restrictions is crucial for both the corporation and its shareholders.

Here are the key ownership restrictions for an S corporation:

Violating these ownership restrictions can result in the termination of the S corporation’s status, subjecting it to different tax treatment and potentially losing the associated benefits.

Read Also: Discovering the Masterminds Behind EF - Everything You Need to Know

It is important for individuals or entities considering ownership in an S corporation to consult with legal and tax professionals to ensure compliance with these ownership restrictions.

An S corporation is limited in the number and type of shareholders it can have. In general, an S corporation can have no more than 100 shareholders.

Individuals, certain estates, and certain trusts can be shareholders in an S corporation. However, partnerships, corporations, and non-resident alien shareholders are not eligible to hold shares in an S corporation.

It is important for the S corporation to maintain accurate records of its shareholders and ensure that the number and type of shareholders remain in compliance with the eligibility requirements for an S corporation.

Any individual or certain qualifying trusts and estates can hold shares in an S corporation. However, there are restrictions on the types of eligible shareholders, such as non-resident aliens, certain types of trusts, and certain types of corporations.

No, non-resident aliens are not eligible to hold shares in an S corporation. Only U.S. citizens, resident aliens, and certain qualifying trusts and estates can be shareholders in an S corporation. This requirement is in place to maintain the S corporation’s status as a domestic entity for tax purposes.

No, most corporations cannot hold shares in an S corporation. The only exception is a wholly-owned subsidiary of an S corporation, which can be a shareholder. However, other types of corporations, such as C corporations or non-profit organizations, are not eligible to hold shares in an S corporation.

Yes, certain types of trusts are eligible to hold shares in an S corporation. These include electing small business trusts (ESBTs), qualified subchapter S trusts (QSSTs), and testamentary trusts. However, grantor trusts and certain other types of trusts are not eligible to hold shares in an S corporation.

What are the disadvantages of Heiken Ashi? Heiken Ashi is a popular charting technique used by traders to predict market trends and make informed …

Read Article

Should I sell my stocks at a loss for tax purposes? When it comes to investing in stocks, many investors experience gains and losses. While it’s …

Read Article

Understanding a stock option statement Stock option statements are an essential part of understanding your investments and making informed decisions. …

Read Article

Best Candlestick Chart for Trading When it comes to trading the financial markets, having access to accurate and reliable data is essential. …

Read Article

Is Pocket Option Trading Halal or Haram? Islamic principles play a significant role in the daily lives of many Muslims, guiding their decisions and …

Read Article

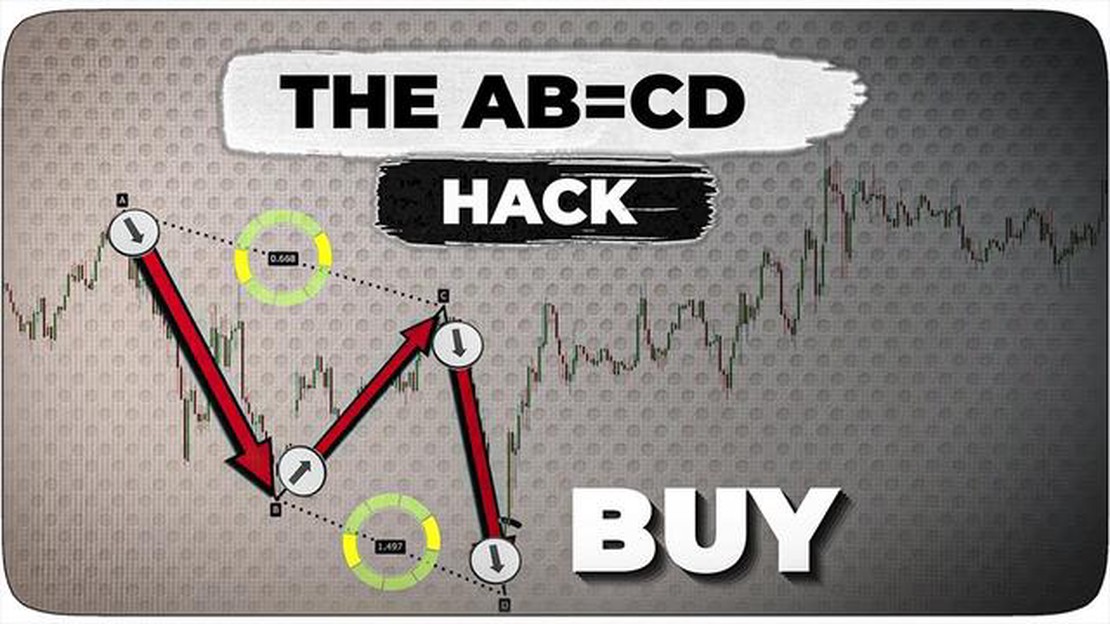

Understanding the ABCD Pattern in Tradingview The ABCD pattern is a popular trading pattern used by technical analysts to identify potential trend …

Read Article