Is IronFX FCA Regulated? Find Out Here!

Is IronFX FCA regulated? If you are considering trading with IronFX, one of the first things you should know is whether they are regulated by the …

Read Article

When it comes to analyzing data and making predictions, it is essential to understand the terms AR and MA. Both of these terms are widely used in statistical analysis and forecasting, and they play a significant role in various fields, including economics, finance, and engineering.

AR stands for AutoRegressive, which refers to a type of model that predicts a future value based on its past values. In other words, an AR model takes into account the previous observations and uses them to forecast the future. The idea behind AR is that the future values depend on the past values, and by identifying patterns and trends in the data, we can make accurate predictions.

MA, on the other hand, stands for Moving Average. Unlike the AR model, which focuses on the past values, the MA model primarily looks at the error term or the difference between the actual and predicted values. By analyzing these errors and creating a moving average of them, the MA model provides insights into the random fluctuations and noise present in the data.

These two concepts, AR and MA, are often combined to create a more powerful forecasting model known as ARIMA (AutoRegressive Integrated Moving Average). By incorporating the AR and MA components along with the integration term, ARIMA model can capture both the autocorrelation and the random noise in the data, allowing for more accurate predictions.

Understanding the terms AR and MA is crucial for anyone working with time series data or involved in forecasting. Whether you are an economist analyzing economic indicators, a finance professional predicting stock prices, or an engineer designing a control system, having a solid understanding of AR and MA models will help you make better predictions and decisions based on historical data.

Autoregressive (AR) and Moving Average (MA) models are commonly used in time series analysis to understand and forecast data patterns. These models are fundamental concepts in econometrics, finance, and other fields that deal with time-dependent data.

The AR model represents a time series as a linear combination of its past values. It assumes that the current value of the series is related to its previous values, with the relationship becoming weaker as we move further back in time. The AR model is defined by two parameters: the order of the model, denoted as p, which represents the number of past values used in the linear combination, and the coefficients associated with each lagged value.

The MA model, on the other hand, describes a time series as a linear combination of random shocks or errors from previous time points. It assumes that the current value of the series depends on the current and previous errors. Like the AR model, the MA model is also defined by an order parameter, denoted as q, which represents the number of previous errors used in the linear combination, and the coefficients associated with each error term.

Both AR and MA models have their own advantages and drawbacks. The AR model is useful for capturing autocorrelation, trend, and seasonality in the data, which can help in forecasting. However, it assumes that the series is stationary, which means that its statistical properties remain constant over time. On the other hand, the MA model can handle non-stationary series but may not capture long-term dependencies as effectively as the AR model. Understanding the characteristics of the data and the assumptions of the models is crucial in selecting the appropriate model for analysis.

Autoregressive (AR) and Moving Average (MA) models are both widely used in time series analysis. While they are similar in some respects, there are key differences between the two:

Definition: AR models predict future values based on linear regression of past values, while MA models predict future values based on linear regression of past errors.

Number of Parameters: AR models have a fixed number of parameters determined by the order of the model, while MA models have a variable number of parameters determined by the number of lagged errors included.

Dependency on Past Values: AR models rely on past values to predict future values, while MA models rely on past errors to predict future values.

Stationarity: AR models require the time series to be stationary, meaning it has a constant mean and variance over time. MA models do not have this requirement and can be used with non-stationary time series.

Read Also: Foreign Transaction Fees in Axis Bank: All You Need to Know

Interpretation: AR models allow for the interpretation of coefficients as the impact of past values on the future values. MA models do not allow for direct interpretation of coefficients.

Forecasting: AR models are better suited for short-term forecasting, while MA models are better suited for smoothing and long-term trend estimation.

In summary, AR and MA models differ in terms of their definition, number of parameters, dependency on past values, stationarity requirement, interpretation of coefficients, and suitability for forecasting. Understanding these differences is crucial for selecting the appropriate model for a given time series analysis.

Autoregressive (AR) and Moving Average (MA) models are widely used in various fields for analyzing and predicting time series data. These models have numerous practical applications that can benefit different industries and domains.

Read Also: Beginner's Guide: How to Trade in Gold Options - Step-by-Step Tutorial

Stock Market Analysis: AR and MA models are commonly used in the financial sector for analyzing stock market data and predicting price movements. By understanding the historical data and identifying the patterns and trends, these models can provide insight into the future performance of stocks.

Forecasting Sales: AR and MA models are essential tools in sales forecasting. These models can help businesses anticipate future sales trends, enabling them to make informed decisions about production, inventory management, and marketing strategies.

Economic Analysis: AR and MA models are extensively used in economic analysis to study economic indicators and forecast economic variables such as GDP, inflation rates, and exchange rates. These models can provide valuable insights into the overall performance and stability of national economies.

Weather Forecasting: AR and MA models are also employed in weather forecasting. These models analyze past weather patterns to predict future weather conditions. By identifying weather trends, these models can assist meteorologists in making accurate and timely forecasts.

Quality Control: AR and MA models find application in quality control processes. They can be used to identify and analyze patterns in production and manufacturing data, aiding businesses in improving product quality and ensuring consistency in production processes.

Healthcare: AR and MA models have been applied in healthcare for analyzing patient data, predicting disease outbreaks, and identifying health trends. By analyzing large amounts of data, these models can assist healthcare professionals in making accurate diagnoses and developing effective treatment plans.

Energy Industry: AR and MA models play a crucial role in the energy industry for optimizing resource allocation, predicting energy demand, and managing costs. These models help energy companies make strategic decisions related to production, distribution, and pricing.

Overall, AR and MA models have a wide range of practical applications across different industries. Their ability to analyze and predict time series data makes them valuable tools for decision-making, planning, and forecasting.

The terms AR and MA stand for autoregressive and moving average, respectively, in statistics. Autoregressive refers to a model that uses past values of a variable to predict future values. Moving average, on the other hand, refers to a model that uses the weighted sum of past forecast errors to predict future values.

Autoregressive models, or AR models, use the past values of a variable to predict future values, whereas moving average models, or MA models, use the weighted sum of past forecast errors to predict future values. While AR models focus on the relationship between the variable and its own past values, MA models focus on the relationship between the variable and past forecast errors.

Autoregressive order, denoted as p, refers to the number of past values of a variable used in an autoregressive model to predict future values. The value of p determines how far back in time the model looks to make predictions.

The difference between AR(1) and AR(2) models lies in the number of past values used to make predictions. In an AR(1) model, only the immediate past value of the variable is considered, whereas in an AR(2) model, the two most recent past values are considered. In general, an AR(p) model considers the ‘p’ most recent past values.

In a model that combines autoregressive and moving average terms, denoted as ARMA(p,q), both the autoregressive order (p) and the moving average order (q) are considered. The autoregressive terms capture the relationship between the variable and its own past values, while the moving average terms capture the relationship between the variable and past forecast errors.

Is IronFX FCA regulated? If you are considering trading with IronFX, one of the first things you should know is whether they are regulated by the …

Read Article

Trading Bitcoin Options: An In-Depth Guide Bitcoin, the world’s first decentralized cryptocurrency, has gained significant popularity in recent years. …

Read Article

How long should I hold onto stock options? Stock options can be a valuable part of an employee’s compensation package, providing an opportunity to …

Read Article

How to Get Verified on Forex If you are a forex trader, getting verified is an essential step to ensure the credibility and security of your trading …

Read Article

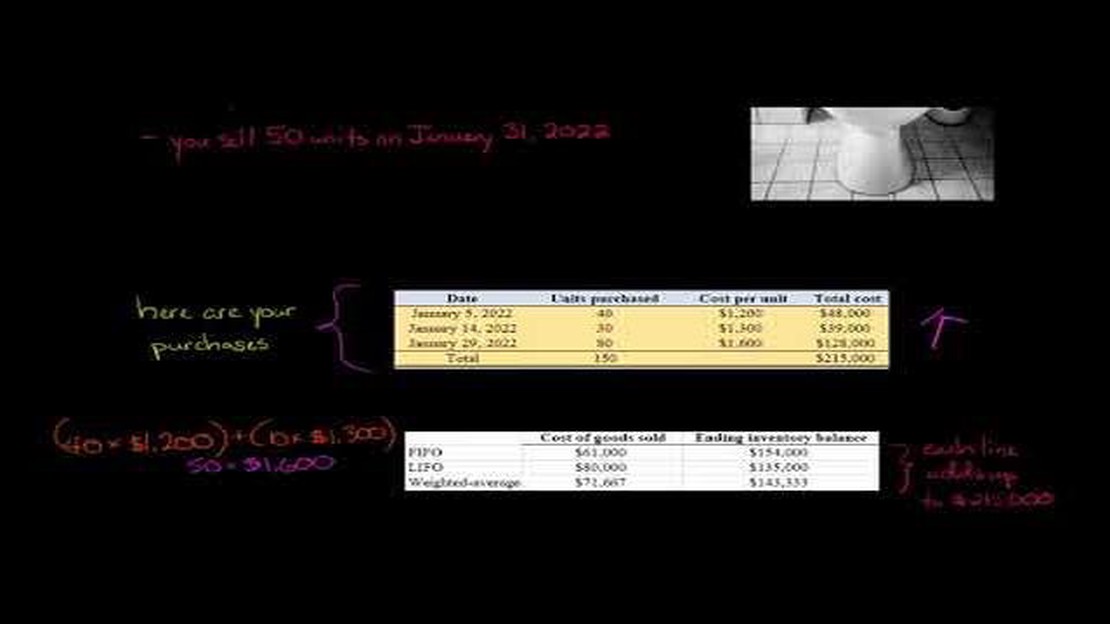

Comparing FIFO and Weighted Average: Which Method is Better? Inventory valuation is an important aspect of accounting for businesses. It involves …

Read Article

What is Hedging in Forex Trading with Examples Forex trading, also known as foreign exchange trading, is the largest and most liquid financial market …

Read Article