Understanding Overbought and Oversold Indicators: Should You Buy or Sell?

Is Overbought Oversold a Signal to Buy or Sell? When it comes to investing in the financial markets, one of the key factors to consider is the concept …

Read Article

If you’re interested in time series analysis and forecasting, you’ve likely come across the term “autoregressive moving average” or ARMA model. Understanding ARMA processes is crucial for successfully modeling and predicting time series data. In this comprehensive guide, we’ll explore the fundamentals of ARMA processes, their components, and how they can be applied to real-world scenarios.

An ARMA process is a mathematical model used to describe the behavior of a time series. It combines autoregressive (AR) components, which account for the linear dependence between current and past observations, and moving average (MA) components, which capture the influence of past error terms on the current value. By incorporating both of these components, ARMA models are able to capture complex patterns and dynamics in time series data.

ARMA processes are widely used in various fields, including economics, finance, and engineering. They can be applied to analyze and forecast a wide range of time-dependent phenomena, such as stock prices, weather patterns, and sales figures. By understanding the underlying principles of ARMA processes, you can gain valuable insights and make informed decisions based on historical data.

In this guide, we’ll delve into the mathematics behind ARMA processes, including the formulas and calculations involved. We’ll also explore different techniques for estimating the parameters of an ARMA model, such as maximum likelihood estimation and Bayesian methods. Additionally, we’ll discuss the limitations and assumptions of ARMA processes, as well as their extensions and variations, such as autoregressive integrated moving average (ARIMA) models.

Whether you’re a beginner or an experienced practitioner in time series analysis, this comprehensive guide will equip you with the knowledge and tools to confidently understand, implement, and interpret ARMA processes. So let’s dive in and explore the fascinating world of autoregressive moving average models!

An Autoregressive Moving Average (ARMA) process is a mathematical model used for time series analysis, forecasting, and modeling. It combines two components: the autoregressive (AR) component and the moving average (MA) component. ARMA processes are widely used in various fields, such as economics, finance, signal processing, and meteorology.

The AR component represents the dependent relationship of the current value of a time series with its past values. It assumes that the current value is a linear combination of the previous values, weighted by coefficients. The order of the AR component, denoted by p, determines the number of past values used in the model.

The MA component, on the other hand, models the dependency of the current value on the past error terms. It assumes that the current value is a linear combination of the past error terms, weighted by coefficients. The order of the MA component, denoted by q, determines the number of error terms used in the model.

The ARMA process can be represented by the equation:

Yt = c + α1Yt-1 + α2Yt-2 + … + αpYt-p + εt + β1εt-1 + β2εt-2 + … + βqεt-q

Read Also: Understanding the Concept of Target in Forex Trading

where Yt is the value of the time series at time t, c is a constant term, αi and βi are the autoregressive and moving average coefficients, εt is the random error term at time t, and p and q are the orders of the AR and MA components, respectively.

ARMA processes are useful for analyzing and forecasting time series data, as they can capture both the trends and the random fluctuations in the data. The parameters of the ARMA model can be estimated using various statistical techniques, such as maximum likelihood estimation or least squares estimation.

By understanding ARMA processes and their components, analysts and researchers can gain valuable insights into the underlying patterns and dynamics of time series data, leading to better predictions and decision-making.

Autoregressive Moving Average (ARMA) processes are widely used in various fields due to their numerous advantages and applications. Let’s explore some of the key advantages and applications of ARMA processes.

| Advantages |

|---|

| 1. Flexibility: |

| 2. Simple Representation: |

| 3. Stationarity: |

| 4. Versatility: |

| 5. Forecasting: |

Now that we have explored the advantages of ARMA processes, let’s take a look at some of the common applications:

Read Also: Understanding the Relationship Between Share Quantity and Option Prices

| Applications |

|---|

| 1. Financial Modeling: |

| 2. Econometrics: |

| 3. Environmental Studies: |

| 4. Time Series Analysis: |

In conclusion, ARMA processes offer several advantages and have a wide range of applications across different disciplines. Their flexibility, simple representation, and ability to capture complex relationships make them a valuable tool for modeling and analyzing time series data.

An ARMA process is a combination of two components: an autoregressive (AR) component and a moving average (MA) component. It is a commonly used time series model that is used to analyze and forecast stationary time series data.

The main difference between an ARMA process and an AR process is that an ARMA process includes both autoregressive (AR) and moving average (MA) components, while an AR process only includes the AR component. The MA component in an ARMA process allows for the modeling of the random shocks or noise in the data, which can improve the model’s ability to capture the dynamics of the time series.

The order of an ARMA process is denoted as ARMA(p, q), where p represents the order of the autoregressive (AR) component and q represents the order of the moving average (MA) component. The order of an ARMA process determines the number of past observations that are used to model the current observation.

An ARMA process can be estimated using various methods, such as the maximum likelihood estimation (MLE) or the least squares (LS) estimation. These methods involve finding the parameter values that maximize the likelihood function or minimize the sum of squared errors between the observed and predicted values. Software packages like R, Python, and MATLAB provide functions for estimating ARMA models.

Yes, there are limitations to using ARMA processes. ARMA models assume that the time series data is stationary, meaning that the mean, variance, and autocovariance remain constant over time. If the data is non-stationary, it may need to be transformed or differenced before fitting an ARMA model. Additionally, ARMA models may not perform well if the data has complex or nonlinear patterns, in which case more advanced models like ARIMA or GARCH may be more appropriate.

Autoregressive Moving Average (ARMA) processes are commonly used in time series analysis to model and forecast data. They combine both autoregressive (AR) and moving average (MA) components to capture the dynamics of the data. The AR component captures the linear dependence of the current value on past values, while the MA component captures the linear dependence of the current value on past error terms. By combining these two components, ARMA processes provide a flexible framework for modeling a wide range of time series data.

The parameters of an ARMA process can be estimated using various methods, including maximum likelihood estimation, least squares estimation, and the Yule-Walker equations. Maximum likelihood estimation involves finding the parameter values that maximize the likelihood of observing the given data. Least squares estimation minimizes the sum of squared differences between the observed data and the corresponding ARMA predictions. The Yule-Walker equations are a set of equations that can be used to estimate the AR parameters of an ARMA process based on the autocovariance function of the data. The choice of estimation method depends on the specific characteristics of the data and the assumptions made about the error terms.

Is Overbought Oversold a Signal to Buy or Sell? When it comes to investing in the financial markets, one of the key factors to consider is the concept …

Read Article

Ways to Avoid Bank Transfer Fees When it comes to sending money, bank transfer fees can really add up. These fees can eat into the amount you are …

Read Article

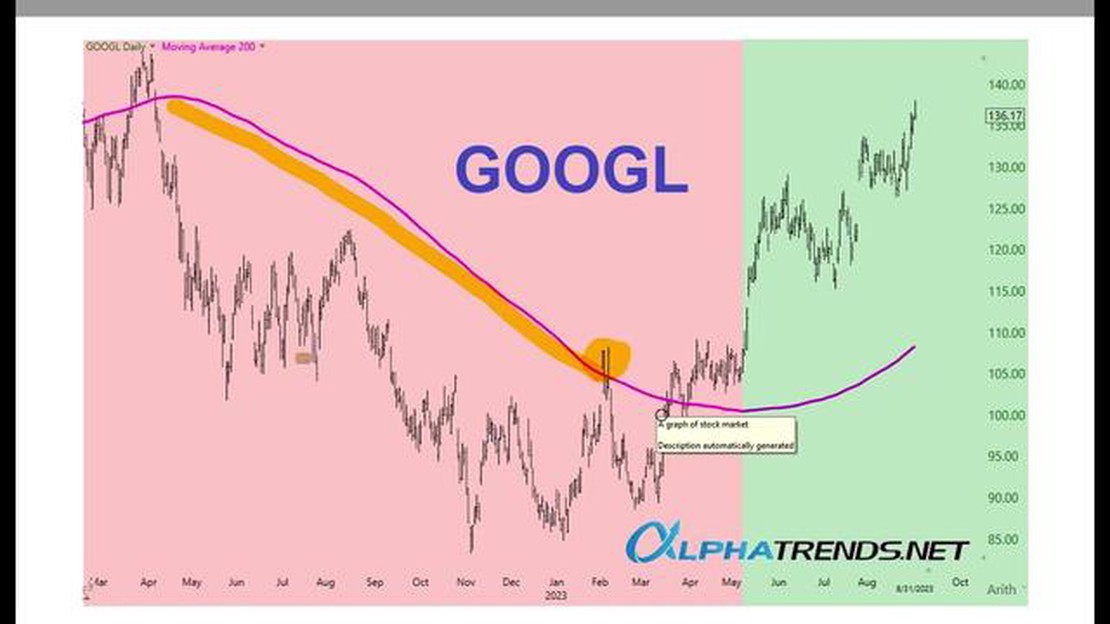

Understanding the Significance of the 200-day Moving Average Investors and traders have long used various technical indicators to help them make …

Read Article

Understanding M1 M2 M3 M4 in Forex Trading Foreign exchange, or forex, trading involves the buying and selling of currencies in order to make a …

Read Article

200-day Moving Average vs Buy and Hold: Which is Better? Investors are always on the lookout for strategies that can help them achieve better returns …

Read Article

Download Historical Forex Data: Step-by-Step Guide Obtaining historical forex data can be a crucial step for analyzing market trends, testing trading …

Read Article