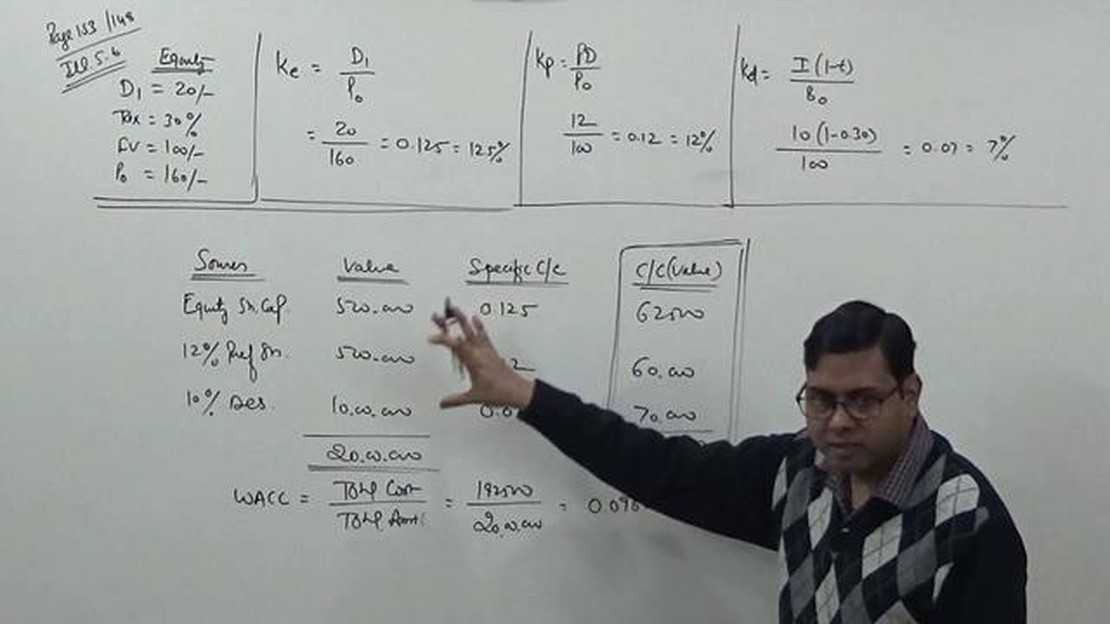

Understanding the Weighted Average Method in Financial Management | Explained in Detail

What is the Weighted Average Method in Financial Management? The weighted average method is a commonly used technique in financial management that …

Read Article

Equity compensation is a common method for companies to attract and retain talented employees. The value of these equity-based awards is often determined by their fair market value, which is subject to regulation under the Accounting Standards Codification (ASC) 409A.

ASC 409A, issued by the Financial Accounting Standards Board (FASB), provides guidelines for the valuation of equity compensation, particularly with regard to non-qualified stock options (NSOs) and stock appreciation rights (SARs). The regulations aim to prevent the improper deferral of income tax for these types of compensation.

Under ASC 409A, it is important for companies to accurately determine the fair market value of their equity awards. This fair market value must be calculated as of the grant date, taking into account various factors such as the company’s financial performance, the volatility of its stock price, and the likelihood of liquidity events.

Non-compliance with ASC 409A can have significant consequences for companies and their employees. If the fair market value of an equity award is improperly determined, the recipient may be subject to additional taxes, penalties, and interest. Additionally, companies may face reputational damage and legal liabilities if they fail to comply with the regulations.

ASC 409A, also known as Accounting Standards Codification 409A, is a regulation created by the Financial Accounting Standards Board (FASB) that governs the valuation and taxation of equity compensation. It was introduced in 2004 to address concerns about the accuracy and consistency of valuations for stock options, stock appreciation rights, and other equity-based compensation plans.

Under ASC 409A, companies are required to determine the fair value of their equity awards and report it as an expense on their financial statements. This is done to ensure that the compensation expense is accurately measured and recognized in the company’s financial statements in the periods in which it is earned.

One of the main objectives of ASC 409A is to prevent companies from manipulating the valuation of their equity awards to reduce their tax liability. It sets strict rules and guidelines for determining the fair value of equity awards, including the use of independent appraisers and specific methodologies.

Failure to comply with ASC 409A can result in severe penalties for both employers and employees. Employers may face additional taxes and interest on deferred compensation, while employees may be subject to additional income tax and penalties on the unvested portion of their equity awards.

In summary, ASC 409A is a regulation that standardizes the valuation and taxation of equity compensation to ensure accuracy, consistency, and fairness. It is important for companies and individuals who have equity-based compensation plans to fully understand and comply with the requirements of ASC 409A to avoid potential legal and financial consequences.

ASC 409A, or Accounting Standards Codification 409A, is a set of guidelines established by the Financial Accounting Standards Board (FASB) that outlines the rules and regulations for valuing and reporting equity compensation instruments, such as stock options, stock appreciation rights, and restricted stock units.

Read Also: What Is ADX Combined With? Discover the Perfect Pairings for The ADX Indicator

Equity compensation is a popular method for companies to attract and retain top talent by offering employees ownership in the form of stock or stock-based instruments. However, the fair value of these equity instruments needs to be accurately determined for financial reporting purposes.

ASC 409A is important in equity compensation because it sets forth specific criteria for valuing equity instruments, which must be followed in order to comply with accounting regulations. Under ASC 409A, the fair value of equity instruments should be determined as of the grant date using a reasonable valuation method.

Read Also: How to Get Trading Signals: A Comprehensive Guide

The importance of complying with ASC 409A in equity compensation cannot be overstated, as failure to do so may result in negative consequences for both the company and the employees. If a company does not properly value its equity instruments, it may lead to inaccurate financial statements, potential audit issues, and legal liabilities.

Furthermore, noncompliance with ASC 409A can also have significant tax implications for the employees. Certain tax penalties and additional taxes may apply if it is determined that the fair value of an equity instrument was incorrectly reported or if the instrument was granted at a discount.

It is crucial for companies to work with experienced valuation professionals who are knowledgeable about ASC 409A and can ensure compliance with its requirements. These professionals can help with the proper valuation of equity instruments, documentation of the valuation process, and the development of policies and procedures to maintain compliance.

In conclusion, ASC 409A plays a crucial role in equity compensation by providing guidelines for valuing and reporting equity instruments. Compliance with ASC 409A is important to avoid financial and legal consequences, as well as potential tax implications for employees. Working with knowledgeable professionals can help companies navigate the complexities of ASC 409A and ensure the accurate valuation and reporting of equity compensation.

ASC 409A refers to Accounting Standards Codification 409A, which sets forth the guidelines for determining the fair value of equity compensation. It is important because non-compliance with ASC 409A can result in significant tax penalties for both the company and the employee.

Some common mistakes include not properly valuing equity compensation at the time of grant, failing to update valuations as necessary, and not consulting with an independent third-party valuation expert. These mistakes can lead to incorrect reporting and non-compliance with ASC 409A.

If a company does not comply with ASC 409A, the employee may be subject to immediate income inclusion and an additional 20% excise tax on the amount of the deferred compensation. This can result in a significant tax burden for the employee.

To ensure compliance with ASC 409A, companies should engage an independent third-party valuation expert to determine the fair value of their equity compensation. Regular valuation updates should also be performed to ensure ongoing compliance. It is advisable to consult with a qualified tax advisor to fully understand the requirements of ASC 409A.

Yes, there are certain exceptions and safe harbors under ASC 409A. For example, certain equity grants made at fair market value are exempt from the requirements of ASC 409A. Additionally, there are specific rules for stock options, stock appreciation rights, and restricted stock that may provide relief from some of the strict requirements of ASC 409A.

What is the Weighted Average Method in Financial Management? The weighted average method is a commonly used technique in financial management that …

Read Article

Discover More about the Da Vinci Company Da Vinci Company is a renowned and innovative technology firm that specializes in creating cutting-edge …

Read Article

How to Download MT5 from Forex? Are you interested in trading on the Forex market using MetaTrader 5 (MT5)? This advanced trading platform offers a …

Read Article

AA Stock: Sector Classification Explained When investing in stocks, it is important to understand the sector in which a particular stock belongs. One …

Read Article

Understanding the Difference Between ATS and Dark Pools Alternative Trading Systems (ATS) and Dark Pools are two popular options for traders looking …

Read Article

Disadvantages of Binary Options: Unveiling the Risks and Downsides Binary options have gained popularity in recent years as a way for individuals to …

Read Article