Discover the most effective engulfing candle strategy for successful trading

Discover the Best Engulfing Candle Strategy for Success Engulfing candlestick patterns are widely used by traders to identify potential reversals in …

Read Article

When it comes to managing money while traveling abroad, there are several options available, with forex cards and debit cards being two of the most popular choices. Both these types of cards offer convenience and security, but they also have some key differences. In this article, we will compare forex cards and debit cards to help you make an informed decision about which one is the better choice for your international travels.

Forex cards, also known as prepaid travel cards, are specifically designed for use while traveling internationally. These cards can be preloaded with multiple currencies, allowing you to conveniently make payments and withdraw cash in the local currency of the country you are visiting. Forex cards offer competitive exchange rates and are widely accepted at merchant establishments and ATMs around the world.

On the other hand, debit cards are traditional bank cards that are linked to your bank account. They are primarily designed for domestic use, but many banks offer debit cards with international usage capability. When using a debit card abroad, you will typically be charged foreign transaction fees and conversion fees for making purchases or cash withdrawals in a foreign currency. However, debit cards offer the advantage of being easily accessible and linked to your bank account, allowing you to monitor your expenses and manage your finances on the go.

Forex cards offer several advantages over debit cards when it comes to international travel and currency exchange. Here are some of the benefits of using a forex card:

1. Convenience: Forex cards are convenient and hassle-free to use. They can be easily loaded with multiple currencies and can be used for cash withdrawal at ATMs or for making payments at POS terminals worldwide.

2. Currency Conversion: Forex cards allow you to load multiple currencies onto a single card, which eliminates the need to carry multiple debit or credit cards. This makes it easier to manage your expenses while traveling and avoids any confusion with currency conversion.

3. Exchange Rates: Forex cards offer competitive exchange rates compared to debit or credit cards. They are generally cheaper than withdrawing cash from ATMs abroad or using your debit/credit card for transactions in foreign currency.

4. Security: Forex cards come with an embedded chip and PIN, which provides an added layer of security. In case of loss or theft, forex cards can be easily blocked and replaced, ensuring the safety of your funds. Moreover, they are not linked to your bank account, reducing the risk of any fraudulent activities.

5. Trackable Transactions: Forex card transactions can be easily tracked online through mobile apps or internet banking. This allows you to keep a record of your expenses and monitor your spending while traveling.

6. Global Acceptance: Forex cards are widely accepted at millions of merchant establishments and ATMs worldwide. They can be used for making purchases, paying bills, and withdrawing cash in the local currency, making it a convenient option for travelers.

Read Also: Trading vs Investing: Clearing the Confusion

7. No Cross-Currency Charges: Forex cards do not attract any cross-currency conversion charges. This means that you can transact in any currency without incurring additional fees.

8. Emergency Assistance: In case of any emergency, most forex card issuers provide 24/7 customer support and assistance. This can be helpful in situations like lost cards, card blocking, or obtaining emergency cash.

Overall, forex cards offer a convenient and cost-effective way to manage your international expenses and currency exchange. They provide better control, security, and flexibility compared to debit cards, making them a preferred choice for frequent travelers.

Debit cards offer several advantages over forex cards:

Read Also: Does IG Forex Use MT4? The Ultimate Guide

Overall, debit cards can be a more cost-effective and convenient option for everyday expenses and travel, especially if you already have a bank account and want easy access to your funds.

There are several advantages of using a forex card compared to a debit card. Firstly, forex cards offer better exchange rates as compared to debit cards. Secondly, forex cards are accepted worldwide, whereas debit cards may have limited acceptance. Additionally, forex cards offer features such as the ability to load multiple currencies, easy reloading options, and better security.

Yes, you can use your forex card for online shopping. Forex cards come with a unique card number, CVV, and PIN, just like a debit card. You can use these details to make online purchases on websites that accept international cards. However, it’s always recommended to check with the forex card issuer about their specific online usage policies.

Yes, forex cards are generally considered safer than debit cards. Forex cards are not linked to your bank account, which means that even if your card is lost or stolen, your bank account remains unaffected. Additionally, forex cards offer features like PIN protection, fraud protection, and the ability to lock or block the card in case of any suspicious activity. This provides an added layer of security compared to debit cards.

When choosing between a forex card and a debit card, you should consider various fees. With a forex card, you may be charged fees such as issuance fees, reloading fees, ATM withdrawal fees, and currency conversion fees. On the other hand, with a debit card, you may have to pay fees like ATM withdrawal fees, transaction fees for international usage, and currency conversion fees. It’s important to compare these fees and choose the option that suits your financial needs.

Forex cards can be used to withdraw cash from ATMs, but there may be certain limitations depending on the card issuer. Some forex cards restrict cash withdrawals to specific ATMs or networks, while others may have a daily or monthly withdrawal limit. It’s advisable to check with the forex card issuer regarding the specific ATM usage policies and any associated fees or restrictions.

A Forex card is a prepaid travel card that allows you to load multiple currencies onto a single card. A debit card, on the other hand, is linked to your bank account and can be used to make purchases or withdraw cash.

Forex cards often offer better exchange rates compared to debit cards. This is because Forex cards are specifically designed for international travel and typically have lower conversion fees. Debit cards, on the other hand, may have higher fees and less favorable exchange rates.

Discover the Best Engulfing Candle Strategy for Success Engulfing candlestick patterns are widely used by traders to identify potential reversals in …

Read Article

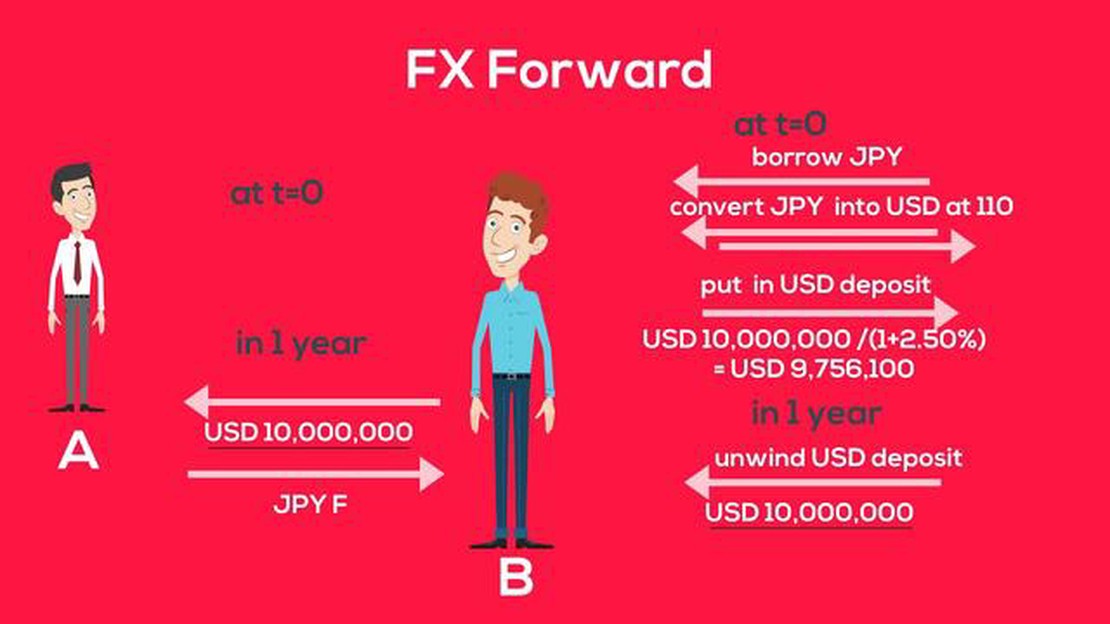

Understanding FX FWD Markets A foreign exchange forward contract, also known as FX FWD, is a financial instrument used in the global currency market. …

Read Article

Two Types of Foreign Trade: Explained Foreign trade plays a crucial role in the global economy, facilitating the exchange of goods and services …

Read Article

Is auto trading profitable? In today’s fast-paced and technology-driven world, auto trading has become an increasingly popular option for investors …

Read Article

What does $() shorthand stand for in jQuery? In the world of web development, jQuery has become an essential tool for creating interactive and dynamic …

Read Article

Understanding the Role of a Trading Turret A trading turret is a specialized communication system used by financial professionals and traders for …

Read Article