Best Forex Trading Platform in China: Which One to Choose?

Best trading platform for Forex trading in China If you’re looking to get started with forex trading in China, it’s crucial to find a reliable and …

Read Article

Value at Risk (VaR) is a statistical measure used to quantify the potential loss an investment or portfolio may experience over a given period of time, with a certain level of confidence. VaR is an important tool for risk management and portfolio construction in finance.

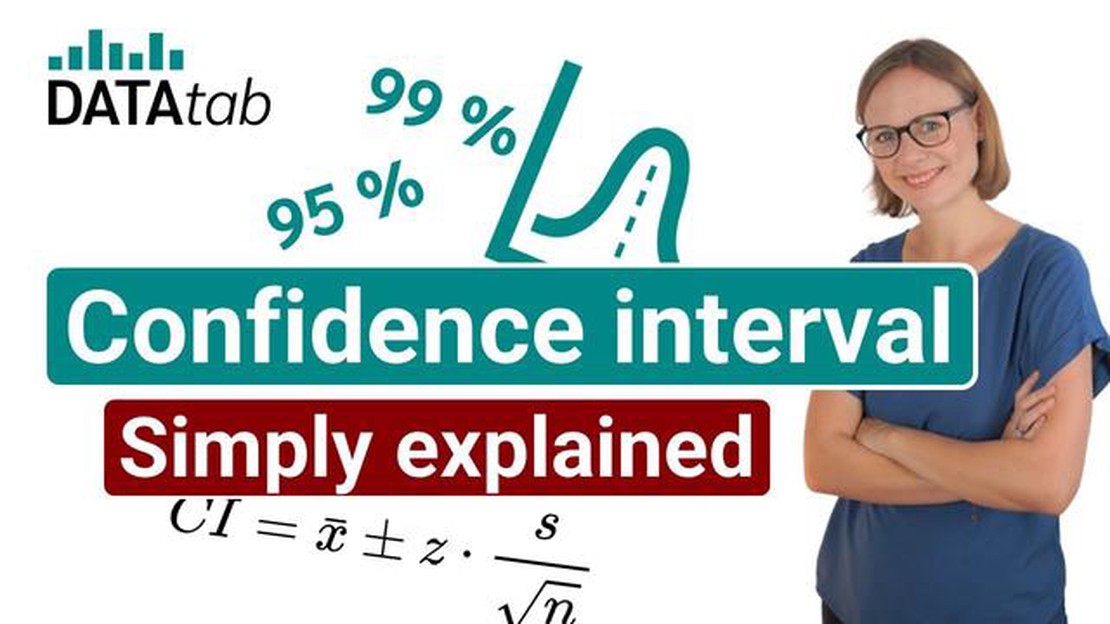

At its core, VaR represents the maximum potential loss that an investment or portfolio could face over a defined time period, under normal market conditions, and with a specified level of confidence. This confidence level is expressed as a percentage, and a commonly used level is 95%.

When we say “VaR at 95% confidence level,” we are referring to the estimated amount of loss that an investment or portfolio could experience, with a 95% probability of not being exceeded over a given time period. In other words, there is a 5% chance that the actual losses could exceed the estimated VaR.

To calculate the VaR at a 95% confidence level, various statistical methods can be used. These methods take into account the volatility of the investment or portfolio, as well as the correlation between different assets within the portfolio. By using historical data and probability distributions, VaR models estimate the potential downside risk.

In summary, the VaR at a 95% confidence level provides investors and portfolio managers with an estimate of the potential maximum loss they could face within a given time frame, while maintaining a high level of confidence. It is an essential tool in risk management and decision-making, allowing investors to assess and mitigate potential risks in their portfolios.

Value at Risk (VaR) is a statistical measure used in financial risk management to estimate the potential loss on an investment or portfolio of investments. It provides an estimate of the maximum loss a certain investment or portfolio could experience over a specified time period, with a specified level of confidence.

VaR is typically used by financial institutions, such as banks and investment firms, to assess and manage risk. It is an important tool for decision-making and risk management, as it helps to determine the amount of capital that should be set aside to cover potential losses and to ensure financial stability.

VaR is calculated using statistical methods, taking into account historical data, volatility, and the desired confidence level. The calculation involves estimating the potential losses based on the historical data and then determining the level of confidence at which the VaR is calculated.

For example, if an investor wants to calculate the VaR at 95% confidence level, it means that there is a 5% (or 1 in 20) chance that the actual loss could be greater than the estimated VaR. This level of confidence is often chosen by investors and financial institutions to ensure they are adequately prepared for potential losses.

VaR can be calculated for different time horizons, such as daily, weekly, or monthly, depending on the needs and preferences of the investor. It can also be calculated for individual securities or portfolios, considering the correlation and diversification effects.

Read Also: Best Candlestick Pattern App: Discover Top Apps for Analyzing Candlestick Patterns

Once the VaR is calculated, it can be used to assess the risk-return trade-off of different investment strategies or portfolios. Investors can compare the VaRs of different investments or portfolios to determine the level of risk they are comfortable with and make informed investment decisions.

However, it is important to note that VaR has limitations and should not be the sole measure of risk. It assumes that the future will follow a similar pattern as the past and does not account for extreme events or changes in market conditions. Therefore, it should be used in conjunction with other risk measures and risk management techniques to make sound financial decisions.

In conclusion, VaR is a valuable tool for risk management and decision-making in the financial industry. It helps investors and financial institutions to estimate potential losses and set aside adequate capital to cover those losses. By understanding VaR and its limitations, investors can make more informed investment decisions and manage risk effectively.

When calculating the Value at Risk (VaR), the confidence level is an essential parameter. The 95 confidence level is the most commonly used level in financial risk management, indicating a 95% probability or confidence that the actual loss will not exceed the calculated VaR.

Read Also: Exploring the Risks of High-Frequency Trading: Impact on the Financial Markets

The importance of the 95 confidence level lies in its balance between accuracy and conservatism. A higher confidence level, such as 99%, would provide a more conservative estimate of potential losses but may not reflect the true risk appetite of the organization. On the other hand, a lower confidence level, such as 90%, would provide a more optimistic estimate of potential losses but may not adequately account for extreme events.

By using the 95% confidence level, financial institutions and investors can strike a balance between effectively managing risk and ensuring reasonable returns. This level allows for a margin of error while still providing a meaningful measure of potential losses. It also aligns with industry standards and regulatory requirements, making it easier to compare and evaluate risks across different organizations or investment portfolios.

In addition, the 95 confidence level allows decision-makers to assess the impact of potential scenarios and make informed judgments. It provides a clear threshold for evaluating the acceptability of risk and determining appropriate risk management strategies.

| Benefits of using the 95 confidence level: |

|---|

| 1. Balance between accuracy and conservatism |

| 2. Reflects the true risk appetite |

| 3. Adequately accounts for extreme events |

| 4. Allows for a margin of error |

| 5. Aligns with industry standards and regulations |

| 6. Provides a clear threshold for evaluating risk |

In conclusion, the 95% confidence level is an important parameter in calculating the VaR as it strikes a balance between accuracy and conservatism. Using this level allows financial institutions and investors to effectively manage risk while still providing a meaningful measure of potential losses.

VaR stands for Value at Risk and is a statistical measure that estimates the maximum potential loss an investment portfolio or position may face over a specified period of time at a certain confidence level. It provides investors with an understanding of the risk associated with their investments and helps them make informed decisions.

VaR can be calculated using various methods, including the parametric method, historical method, and Monte Carlo simulation. In the parametric method, VaR is calculated based on assumptions about the distribution of asset returns. The historical method calculates VaR based on historical data, while the Monte Carlo simulation generates random scenarios to estimate potential losses. The choice of method depends on the characteristics of the investment portfolio and the level of accuracy desired.

The confidence level in VaR represents the likelihood of a loss exceeding the estimated VaR. For example, a VaR at a 95% confidence level means that there is a 5% chance of experiencing a loss greater than the estimated VaR. Higher confidence levels, such as 99%, provide a greater level of certainty but may also result in a higher estimated VaR.

Calculating VaR at different confidence levels allows investors to understand the potential risk of their investments under different scenarios. Higher confidence levels, such as 99%, provide a greater level of certainty but may also result in a higher estimated VaR. Lower confidence levels, such as 90%, provide a lower level of certainty but may result in a lower estimated VaR. The choice of confidence level depends on the investor’s risk tolerance and investment objectives.

Best trading platform for Forex trading in China If you’re looking to get started with forex trading in China, it’s crucial to find a reliable and …

Read Article

Choosing the Best Indicator for Bollinger Bands Bollinger Bands are a popular technical analysis tool used by traders to identify potential breakout …

Read Article

Understanding the Significance of High Open Interest Compared to Volume on Options Options trading is a complex financial instrument that involves …

Read Article

Three Momentum Indicators: Understanding the Key Tools for Traders Whether you are a seasoned trader or just starting out in the stock market, …

Read Article

Choosing the Right Delta for Your Option Strategy When it comes to options trading, delta is a crucial concept to understand. Delta measures the rate …

Read Article

Using a Forex Card in Any Country: Is it Possible? Forex cards are a popular choice for travelers when it comes to managing their finances abroad. …

Read Article