Understanding W1 in trading: Key factors and implications

What does W1 mean in trading? When it comes to trading in the financial markets, there are many indicators and tools that traders use to make informed …

Read Article

Employee Stock Purchase Plans (ESPPs) are popular compensation programs offered by many companies in Canada. These plans allow employees to purchase company stock at a discounted price, usually through payroll deductions. While ESPPs provide employees with an opportunity to participate in the growth of the company and potentially earn additional income, it is important for employees to understand the potential tax implications of participating in these plans.

One of the key tax implications of ESPPs in Canada is the treatment of the discount received by employees when purchasing company stock. Typically, the discount is considered a taxable benefit and must be included in the employee’s income for the year in which the stock is purchased. This means that employees will need to pay taxes on the discount they received, just like any other form of compensation.

Another tax implication is the potential for a capital gain or loss when the employee eventually sells the purchased stock. If the stock is held for at least two years from the date of purchase and at least one year from the date of exercise (i.e., when the employee actually acquires the stock), any gain on the sale of the stock will be considered a capital gain and subject to capital gains tax. However, if the stock is sold before meeting these holding periods, any gain will be treated as ordinary income and taxed accordingly.

It is also worth noting that employees may be eligible for a deduction on their income taxes for the amount of the discount they included as income if certain conditions are met. For example, if the stock is held for at least two years from the date of purchase and at least one year from the date of exercise, employees may be able to claim a deduction equal to 50% of the discount as a capital gains deduction, effectively reducing the taxable amount.

Overall, participating in an Employee Stock Purchase Plan can have both financial and tax implications for employees in Canada. It is important for employees to understand the potential tax consequences and to consult with a tax professional to ensure compliance with tax laws and to maximize the benefits of participating in an ESPP.

Employee Stock Purchase Plans (ESPP) offer employees the opportunity to purchase company stock at a discounted price. While these plans can be a valuable benefit, it is important for Canadian employees to understand the tax implications involved.

Understanding the Taxable Benefit

When an employee participates in an ESPP, they receive a taxable benefit equal to the difference between the fair market value of the shares at the time of purchase and the price paid by the employee. This benefit is considered employment income and is subject to income tax.

Reporting the Taxable Benefit

The taxable benefit from participating in an ESPP is reported on the employee’s T4 slip in the year in which the shares are purchased. It is important to report this income accurately to ensure compliance with Canada Revenue Agency (CRA) regulations.

Withholding Taxes

Employers are required to withhold taxes on the taxable benefit provided through an ESPP. The amount of tax deducted depends on the employee’s tax bracket and is calculated based on the fair market value of the shares at the time of purchase.

Sale of ESPP Shares

Read Also: Is Thinkmarket Legit? Unbiased Review and Analysis

If an employee sells their ESPP shares, any gains from the sale are considered a capital gain and are subject to capital gains tax. The cost base for calculating the capital gain is the fair market value of the shares at the time of purchase, plus any taxable benefit already reported as employment income.

Identifying the Eligible Amount

Employees may be eligible for a deduction on the capital gains tax if they meet certain criteria. The eligible amount is calculated based on the employee’s ownership period and the type of shares held.

Seek Professional Advice

Given the complexity of ESPP tax implications, it is recommended that employees seek professional advice from a tax specialist or accountant. They can provide guidance on reporting requirements, withholding tax obligations, and any eligible deductions.

Conclusion

Employee Stock Purchase Plans (ESPP) can be a valuable benefit, but it is important for Canadian employees to understand the tax implications involved. By understanding the taxable benefit, reporting requirements, and potential deductions, employees can effectively manage their tax obligations and maximize their financial benefits from participating in an ESPP.

Employee Stock Purchase Plans (ESPPs) are a type of employee benefit program that allows eligible employees to purchase company stock at a discounted price. These plans are offered by many companies as a way to attract and retain talented employees by giving them a stake in the company’s success.

Read Also: What is the Optimal RSI Level for Forex Trading?

ESPPs typically work on a subscription period basis, where employees have the option to contribute a percentage of their salary to purchase company stock. This contribution is usually deducted from the employee’s paycheck on an after-tax basis. At the end of each subscription period, employees can use their accumulated contributions to purchase company stock.

The purchase price of the company stock in an ESPP is usually set at a discount to the market price. This discount can range from a few percent up to a maximum of 15% as specified by Canadian tax laws. The discounted purchase price allows employees to buy company stock at a lower cost compared to the market price, potentially resulting in gains if the stock value increases.

ESPPs often have a “lookback” feature, which allows employees to purchase company stock at the lower of either the market price at the beginning or end of the subscription period. This feature provides an additional advantage to employees, as it ensures they can benefit from any decrease in the stock price during the subscription period.

Once employees have purchased company stock through an ESPP, they have the option to hold onto the shares or sell them. The decision to hold or sell the shares can be based on market conditions, personal financial goals, and tax implications.

It’s important for employees to understand the tax implications of participating in an ESPP. When employees purchase company stock through an ESPP, they may be subject to income tax on the discount received. Additionally, any gains from the sale of the stock may be subject to capital gains tax.

Overall, understanding the mechanics of an ESPP is essential for employees considering participation in such a program. By understanding how ESPPs work, employees can make informed decisions about their contributions, stock purchases, and tax implications.

An employee stock purchase plan (ESPP) is a program that allows employees of a company to purchase company stock at a discounted rate.

In Canada, an ESPP typically works by allowing employees to contribute a portion of their salary to purchase company stock at a discounted rate. The contributions are usually made through payroll deductions. The purchased stock is then held in the employee’s brokerage account.

When participating in an ESPP in Canada, there are two types of tax implications to consider. Firstly, the discount received on the purchase of stock is considered employment income and is subject to the normal income tax. Secondly, any capital gains or losses realized when selling the stock may be subject to capital gains tax.

Yes, there can be tax advantages to participating in an ESPP in Canada. The employment income resulting from the discount on the stock purchase can be eligible for a stock option deduction, which can reduce the overall taxable amount. Additionally, if the stock is held for a certain length of time, any capital gains may be eligible for the 50% capital gains inclusion rate, resulting in a lower tax liability.

If you sell your ESPP shares immediately after purchasing them, you may realize a capital gain or loss depending on the market value of the stock at the time of sale. This gain or loss will be subject to capital gains tax. Additionally, any discount received on the purchase of the stock will be considered employment income and will be subject to income tax.

What does W1 mean in trading? When it comes to trading in the financial markets, there are many indicators and tools that traders use to make informed …

Read Article

Autobahn Futures and Options: Exploring the Benefits and Opportunities Autobahn futures and options are financial derivatives that allow investors to …

Read Article

Advantages of Trading Barrier Options Barrier options are a type of financial derivatives that offer unique benefits to traders. These options have a …

Read Article

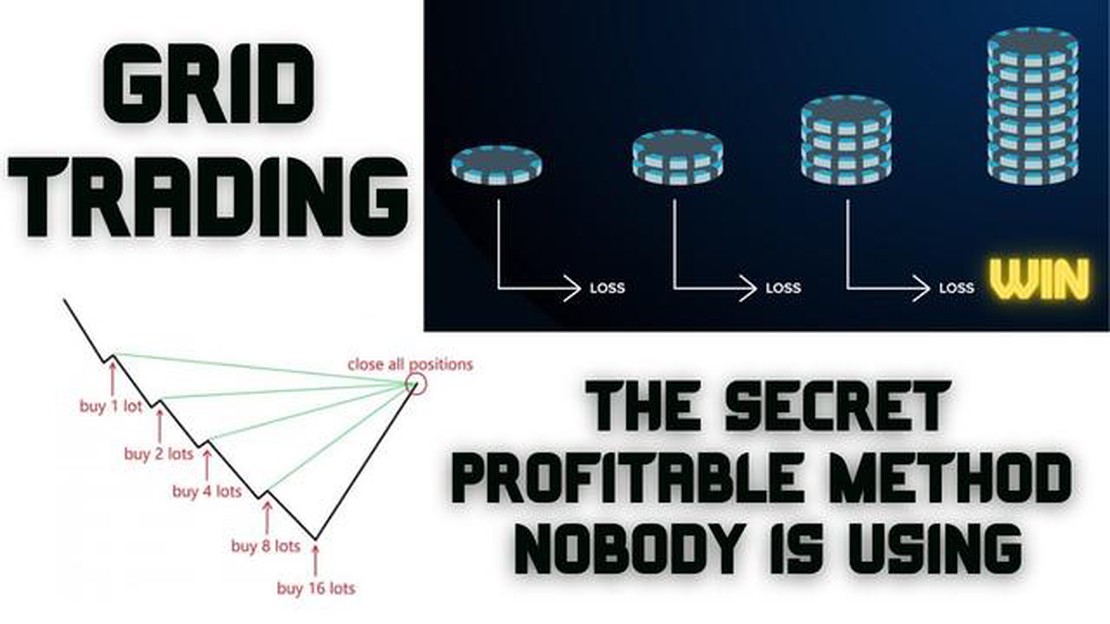

Is grid trading safe? Grid trading is a popular trading strategy that involves placing buy and sell orders at specific price points on a grid. It is …

Read Article

Is it Worth Upgrading to a Unified Trading Account? Trading in the financial markets can be a complex and challenging process. Whether you are a …

Read Article

XM Broker Review: How Good is XM Broker? XM Broker is a well-known online trading platform that has gained popularity among traders worldwide. With …

Read Article