Choosing the Best Forex Indicator: A Comprehensive Guide

Choosing the Best Indicator for Forex Trading When it comes to trading on the foreign exchange market, having the right tools and strategies is …

Read Article

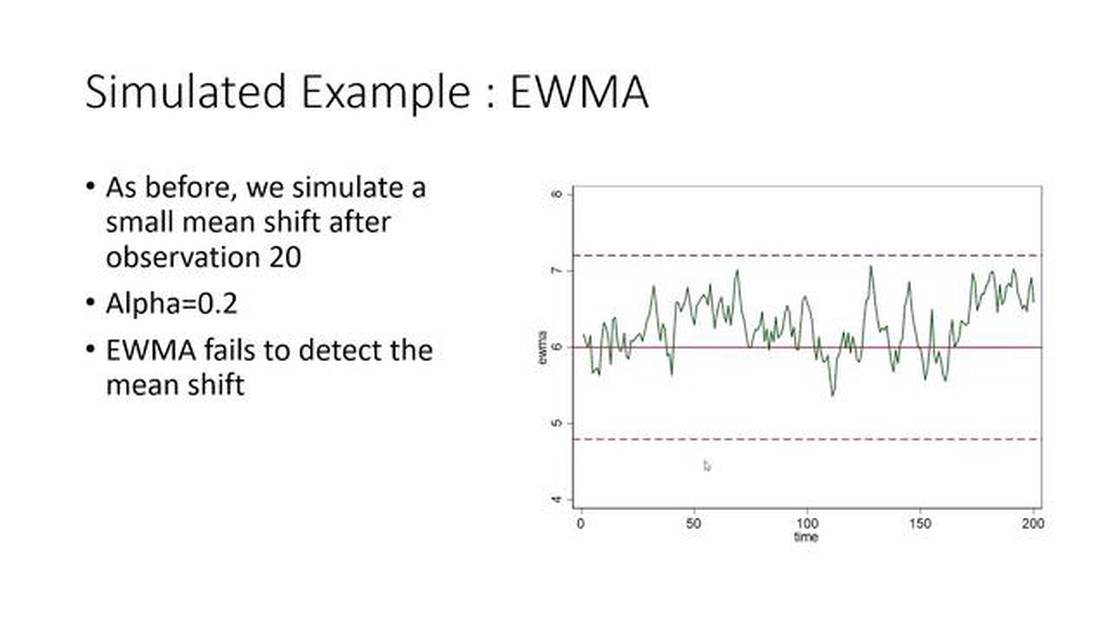

The Exponentially Weighted Moving Average (EWMA) is a statistical method used in data analysis to better understand trends and patterns in a dataset. It is particularly useful in finance and economics, where it can be applied to analyze stock prices, market trends, and economic indicators.

Unlike a simple moving average, which assigns equal weight to all data points, the EWMA assigns greater weight to more recent data points. This means that the EWMA places more emphasis on recent trends and is better able to capture short-term changes in the data. As a result, the EWMA is more responsive to recent events and can provide a more accurate representation of the underlying trend.

The functionality of the EWMA lies in its ability to reduce the impact of outliers and noise in the data. By assigning greater weight to recent data points, the EWMA effectively “smoothes” the data and filters out random fluctuations. This makes it easier to identify underlying patterns and trends and facilitates better decision-making.

Another key feature of the EWMA is its flexibility. The level of smoothing can be adjusted by changing the decay factor, which determines the weight given to each data point. A higher decay factor places more weight on recent data points, resulting in a more responsive and volatile trend. On the other hand, a lower decay factor places more weight on past data points, smoothing out short-term fluctuations and providing a more stable trend.

The Exponentially Weighted Moving Average (EWMA) is a statistical method that calculates the weighted average of a time series data, giving more importance to recent values and less to old values. It is a popular tool used in various fields, such as finance, engineering, and data analysis, for smoothing and forecasting purposes.

The EWMA assigns exponentially decreasing weights to past observations, with the most recent observations having higher weights. This allows the average to adapt quickly to changes in the data, making it more responsive to recent trends. The weighting factor is determined by the smoothing parameter, which controls how quickly the weights decay as the data ages.

The formula used to calculate EWMA is as follows:

where:

By adjusting the value of α, one can control the emphasis placed on recent observations. A smaller α will give more importance to past observations, resulting in a smoother average, while a larger α will give more weight to recent observations, making the average more responsive to changes.

The EWMA is often used in time series analysis to estimate the current value or forecast future values based on historical data. It is especially useful for handling data with trends, seasonality, or other patterns, as it can help identify underlying patterns and remove noise.

In conclusion, the Exponentially Weighted Moving Average is a flexible and powerful tool for analyzing and smoothing time series data. Its ability to adapt to changing trends and patterns makes it a valuable tool in various fields.

The Exponentially Weighted Moving Average (EWMA) is a statistical method used to analyze and forecast time series data. It is commonly used in various fields such as finance, economics, and statistics. EWMA assigns exponentially decreasing weights to older observations and gives more importance to recent observations. This allows it to capture short-term trends and react quickly to changes in the data.

To calculate EWMA, you first need to assign an initial value to the weighted moving average. This is typically the first observation in the data series. Then, you need to choose a smoothing factor, often denoted as λ (lambda). The value of λ determines the rate of decay of the weights. A smaller λ gives more weight to recent observations, while a larger λ puts more weight on older observations.

Read Also: How Long Does It Take to Withdraw from LiteFinance? - Find Out the Process and Timing

Once the initial value and the smoothing factor are defined, you can calculate the EWMA for each subsequent observation using the following formula:

where EWMA(t) represents the EWMA value at time t, observation(t) is the current observation, and EWMA(t-1) is the EWMA value calculated for the previous period.

Read Also: Limitations of the Method of Moving Average: Understanding Its Two Key Drawbacks

By iterating this calculation for each subsequent observation, you can create a time series of EWMA values that reflect the behavior of the underlying data. This allows you to analyze the trend and volatility of the data, identify anomalies, and make predictions based on the EWMA.

The Exponentially Weighted Moving Average (EWMA) is a widely used tool in financial analysis. It is particularly valuable in managing the risk associated with financial assets and portfolios.

EWMA allows analysts and investors to identify and predict trends in financial data by giving more weight to recent observations. This is important because financial markets are dynamic and constantly changing, and it is crucial to have a method that can accurately capture and respond to these changes.

One of the main advantages of EWMA is its ability to reduce the impact of outliers or extreme observations. By giving more weight to recent data, outliers are dampened, and the resulting smoothed series provides a more realistic representation of the underlying trend.

Another key benefit of EWMA is its adaptability. Unlike other moving average techniques, EWMA allows users to adjust the level of smoothing by changing the value of the decay factor. This flexibility is crucial in financial analysis as different assets and portfolios require different levels of smoothing depending on their volatility and risk tolerance.

The ability to accurately capture and respond to changing market conditions is essential in financial analysis. By using EWMA, analysts and investors can make more informed decisions by identifying and reacting to trends in real-time. This can help mitigate risks, optimize investment strategies, and ultimately improve financial performance.

In conclusion, the Exponentially Weighted Moving Average is a powerful tool that has a significant impact on financial analysis. Its ability to capture trends, reduce the impact of outliers, and its adaptability make it an invaluable resource in managing risk and optimizing investment strategies. By understanding and utilizing EWMA, analysts and investors can gain a competitive edge and make more informed decisions in the dynamic world of finance.

An Exponentially Weighted Moving Average (EWMA) is a statistical calculation that assigns weights to historical data points, with the most recent data points being assigned higher weights. This weighted average is commonly used in finance and economics to track trends and forecast future values.

In EWMA, the weight assigned to each data point is determined by a smoothing factor. The smoothing factor is usually a value between 0 and 1, where a higher value assigns more weight to recent data points, and a lower value assigns more weight to older data points.

One of the main advantages of EWMA is that it gives more importance to recent data, making it more responsive to changes in the underlying data. This can be particularly useful when dealing with time series data that exhibits trend or seasonality. Additionally, EWMA does not require the storage of large amounts of historical data, making it more efficient for computational purposes.

Yes, EWMA can be used to forecast future values based on historical data. By assigning higher weights to recent data points, EWMA captures the underlying trend and can be used to predict future values. However, it is important to note that the accuracy of the forecast depends on the quality and representativeness of the historical data.

Choosing the Best Indicator for Forex Trading When it comes to trading on the foreign exchange market, having the right tools and strategies is …

Read Article

Fast Moving Average vs Slow Moving Average: Understanding the Difference When it comes to analyzing the stock market and making investment decisions, …

Read Article

How to Identify a Fractal Pattern Welcome to a comprehensive guide on identifying fractal patterns. Fractals are fascinating geometric shapes that …

Read Article

What is the typical bid-ask spread? The bid-ask spread is a crucial concept in the world of finance and trading. It refers to the difference between …

Read Article

Is a high margin level good? A high margin level is often seen as a positive indicator for businesses. It represents the difference between the cost …

Read Article

Step-by-Step Guide: How to Draw Supply and Demand Zones Effectively If you want to become a successful trader in the financial markets, understanding …

Read Article