What is the Official Exchange Rate for AUD EUR?

Official Exchange Rate for AUD to EUR If you are planning a trip to Australia or Europe, it’s crucial to know the official exchange rate for AUD …

Read Article

FX options are financial instruments that give traders the right, but not the obligation, to buy or sell a currency at a predetermined exchange rate on or before a specific date. These options are commonly used by businesses and investors to hedge against currency risk and speculate on future currency movements.

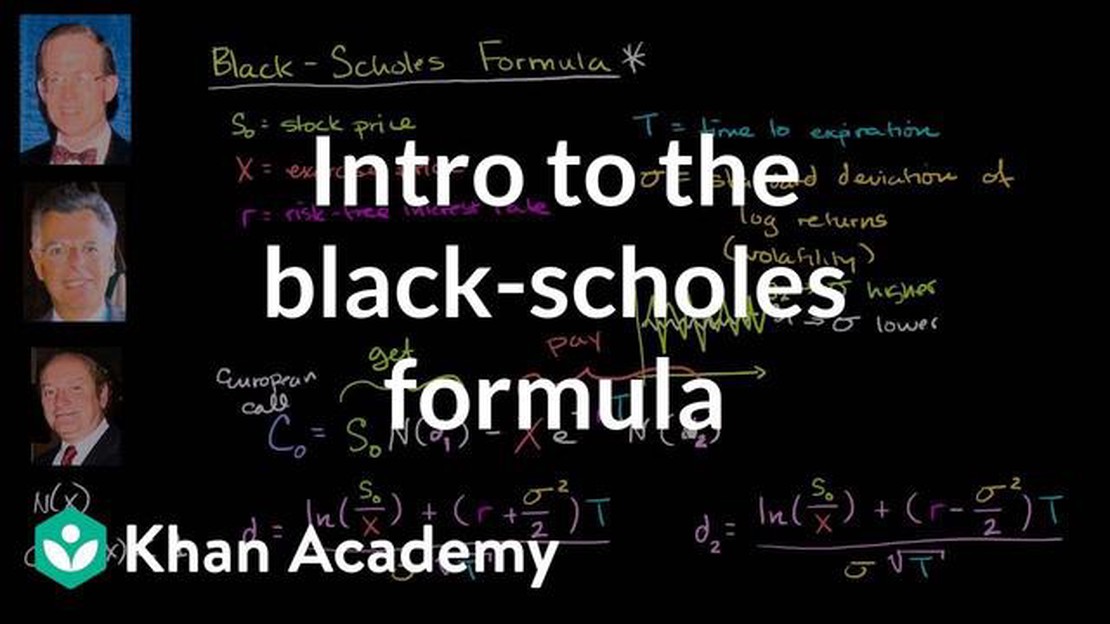

The Black Scholes formula, also known as the Black-Scholes-Merton model, is a mathematical model used to calculate the theoretical price of options. It was developed by economists Fischer Black, Myron Scholes, and Robert Merton in the early 1970s. This formula revolutionized the options market and provided a way to determine the fair value of options, including FX options.

The Black Scholes formula takes into account several variables, such as the current price of the underlying currency, the strike price of the option, the time to expiration, the risk-free interest rate, and the volatility of the underlying currency. By inputting these variables into the formula, traders can determine the theoretical price of the option.

Understanding the Black Scholes formula is crucial for traders and investors who are involved in the FX options market. It allows them to make informed decisions about buying or selling options, as well as to evaluate the fair value of their positions. By knowing the fair value of an option, traders can identify opportunities for arbitrage, where they can buy an option for less than its theoretical price and sell it for a profit.

Disclaimer: The Black Scholes formula is a theoretical model that assumes certain market conditions and may not always accurately reflect the actual price of options. Traders should exercise caution and consider other factors when making trading decisions.

In conclusion, the Black Scholes formula is a powerful tool for understanding the fair value of FX options. It provides traders and investors with a mathematical framework for pricing options and making informed decisions. While it has its limitations, the Black Scholes formula has significantly contributed to the development of the options market and continues to be widely used in financial institutions around the world.

The Black Scholes formula, also known as the Black Scholes model, is a mathematical equation used to calculate the theoretical price of options. It was developed by economists Fischer Black and Myron Scholes in 1973 and is widely used in finance to value various financial instruments, including foreign exchange (FX) options.

The formula takes into account several input variables, including the current price of the underlying currency pair, the strike price of the option, the time to expiration, the risk-free interest rate, and the volatility of the currency pair’s price. By using these variables, the Black Scholes formula provides an estimate of the fair value of an FX option.

The formula is based on several assumptions, including that the underlying currency pair follows a log-normal distribution, that there are no transaction costs or taxes, and that the risk-free interest rate is constant over the life of the option. These assumptions allow for a simplified mathematical model to be used in valuing options.

The Black Scholes formula for FX options can be summarized as:

Read Also: Understanding Graded Vesting for Stock Options: A Comprehensive Guide

C = Se(r - d)TN(d1) - Xe-rTN(d2)

Where:

The Black Scholes formula allows traders and investors to estimate the fair value of FX options and make more informed trading decisions. It is an important tool in the field of financial derivatives and has significantly contributed to the development of options markets.

Black-Scholes formula for FX options is a mathematical equation that is widely used to price options and calculate implied volatility. It was developed by economists Fischer Black and Myron Scholes in 1973 and revolutionized the finance industry by providing a framework for valuing derivative products.

Read Also: George Soros Forex Strategy Uncovered: Learn the Secrets Behind His Success

The main concept behind the Black-Scholes formula is that the price of an option can be determined by considering various factors such as the strike price, time to expiration, interest rates, and the volatility of the underlying asset. By inputting these variables into the formula, traders and investors can calculate the fair value of an option and make informed trading decisions.

The Black-Scholes formula has numerous applications in the financial markets, particularly in the field of FX options. It is used by traders, investors, and risk managers to price and hedge options positions, as well as to assess the level of risk associated with these positions. The formula also provides insights into market expectations of future volatility, which can be valuable for making investment decisions.

Furthermore, the Black-Scholes formula is an important tool for market makers, who use it to determine bid and ask prices for options. By calculating the fair value of an option, market makers can ensure that they are providing competitive prices and capturing profits from the bid-ask spread.

Overall, a deep understanding of the Black-Scholes formula is essential for anyone involved in options trading or risk management. By grasping the concept and its applications, market participants can make more informed decisions and navigate the complex world of options trading with greater confidence.

The Black Scholes formula is a mathematical equation used to calculate the theoretical pricing of options. It takes into account various factors such as the current price of the underlying asset, the strike price, the time to expiration, the risk-free interest rate, and the volatility of the underlying asset.

The Black Scholes formula can be applied to FX options by substituting the underlying asset with the exchange rate between the two currencies involved. The other factors such as the strike price, time to expiration, interest rate, and volatility still need to be considered. By plugging these values into the formula, the theoretical price of the FX option can be calculated.

The Black Scholes formula makes several assumptions, including a constant volatility of the underlying asset, continuous trading, no transaction costs, instant execution of options, no dividends paid on the underlying asset, and a risk-free interest rate that remains constant throughout the life of the option.

The Black Scholes formula provides a model for estimating the theoretical price of FX options. However, it is important to note that the actual market price of options may deviate from the calculated price due to various factors such as market conditions, liquidity, and supply and demand dynamics. Traders and investors should use the Black Scholes formula as a guide, but also consider other factors and market conditions when determining the price of FX options.

Official Exchange Rate for AUD to EUR If you are planning a trip to Australia or Europe, it’s crucial to know the official exchange rate for AUD …

Read Article

Understanding Sentiment Trades: Analysis and Strategies Investing in the stock market can be a challenging and unpredictable endeavor. Traders are …

Read Article

Charges for Foreign Remittance: Everything You Need to Know When it comes to sending money internationally, understanding the associated charges and …

Read Article

Where and How to Purchase Iraqi Dinar: A Comprehensive Guide If you’re interested in expanding your investment portfolio, you may have come across the …

Read Article

Exchange Rate Policy in Azerbaijan: Is it Fixed? Azerbaijan, a country located at the crossroads of Eastern Europe and Western Asia, has a currency …

Read Article

Limitations of the Moving Average Method: Explained The moving average method is a popular statistical technique used to analyze data over a certain …

Read Article