How to Start Trading with 100 Rupees: A Comprehensive Guide

Beginners’ Guide: Trading with 100 Rupees Trading in the stock market can be an exciting and potentially lucrative endeavor. While many people assume …

Read Article

Forex trading, also known as foreign exchange trading, is a popular investment option for individuals looking to profit from the fluctuation of currency exchange rates. In the United Kingdom, forex traders are subject to specific tax regulations that determine how their trading activities are taxed.

One important aspect of forex trading taxation in the UK is the classification of traders as either investors or traders. Investors are individuals who trade forex as a form of investment, while traders are individuals who trade forex as a business or profession. The classification determines how the profits and losses from forex trading are taxed.

For investors, the profits from forex trading are generally taxed as capital gains, which are subject to capital gains tax. Capital gains tax is currently applicable to individuals who earn over a certain threshold per year. The tax rate varies depending on the individual’s income and other factors, but it is generally lower than the tax rate for regular income.

On the other hand, traders who are classified as such are subject to income tax on their profits from forex trading. Income tax rates vary depending on the individual’s total income and other factors. It’s important for traders to keep track of their trading activities and maintain proper records for tax purposes.

In conclusion, understanding the taxation of forex trading in the UK is crucial for individuals engaging in this investment activity. Whether as an investor or a trader, knowing the specific tax regulations and obligations can help ensure compliance and optimize tax planning strategies. Seeking advice from a tax professional is recommended to navigate the complexities of forex trading taxation.

When it comes to taxation of forex trading in the UK, it is important to understand the basic principles that govern the process. Here are some key concepts to keep in mind:

| 1. Taxable Income | In the UK, income from forex trading is treated as taxable income. This means that any profit you make from trading forex will be subject to taxation. |

| 2. Capital Gains Tax | Forex trading falls under the capital gains tax regime in the UK. This means that any profit made from trading forex will be subject to capital gains tax, which is calculated based on the difference between the purchase price and the sale price of the currency. |

| 3. Income Tax | Income from forex trading may also be subject to income tax in the UK. If you are trading forex as your primary source of income, you may need to pay income tax on your profits. |

| 4. Allowable Deductions | When calculating your taxable income from forex trading, you are allowed to deduct certain expenses and losses incurred during the trading process. These deductions can reduce your overall tax liability. |

| 5. Tax Evasion | It is important to note that attempting to evade taxes on your forex trading profits is illegal in the UK. Failure to comply with tax laws can result in penalties, fines, and even criminal charges. |

Understanding these basic principles of taxation can help you navigate the tax obligations associated with forex trading in the UK. It is advisable to consult with a tax professional or an accountant to ensure that you are fulfilling your tax obligations and properly reporting your forex trading income.

Forex trading has become increasingly popular in the UK, and as a forex trader, it’s important to be aware of the tax implications that come with this type of trading. Understanding these tax obligations can help you avoid any potential legal issues and ensure that you are compliant with the law.

Capital gains tax: In the UK, forex trading is generally considered to be a form of investment rather than a business activity. This means that for most individuals, any profits made from forex trading will be subject to capital gains tax (CGT). CGT is calculated based on the difference between the buying and selling price of an asset, and it applies to the annual gains that exceed the tax-free allowance.

Tax-free allowance: As of the tax year 2021/2022, the annual tax-free allowance for CGT is £12,300. If your total gains for the year are below this threshold, you will not have to pay any CGT. However, if your gains exceed this limit, you will be required to report and pay tax on the excess amount.

Income tax: In some cases, forex trading may be considered a full-time profession or business activity. If you are actively trading forex as your main source of income, your profits may be subject to income tax rather than CGT. Income tax rates can vary depending on your overall income and tax bracket, so it’s important to consult with a tax professional to determine the specific rates that apply to you.

Expense deductions: As a forex trader, you may be able to deduct certain expenses related to your trading activities. These expenses can include internet and software costs, trading platform fees, and educational materials. However, it’s important to keep detailed records and receipts to justify these deductions in case of an audit.

Read Also: Understanding the Formula for Quanto Options: A Comprehensive Guide

Trading losses: If you experience losses in your forex trading activities, you may be able to offset these losses against any capital gains or other taxable income. This can help to reduce your overall tax liability. Again, it’s important to keep accurate records of these losses to support your tax calculations.

Disclaimer: The information provided in this article is for general informational purposes only and should not be considered as professional tax advice. Tax laws are subject to change, and it’s important to consult with a qualified tax professional to understand your individual tax obligations.

When it comes to forex trading income, it is essential to understand the importance of reporting and documenting your earnings to ensure compliance with the UK tax laws. The proper reporting and documentation of your forex trading income will not only help you meet your legal obligations but also provide transparency and support in case of any tax audits or inquiries.

First and foremost, it is crucial to keep accurate and detailed records of all your forex trading activities. This includes maintaining a record of all trades, including the date, time, currency pairs traded, the price at which you entered and exited the trade, and any profits or losses incurred. These records can be maintained electronically or in hard copy format, as long as they are easily accessible and can be readily provided upon request.

Read Also: How to Identify if a Forex Factory Reports High Impact News

In addition to trade records, it is also important to keep track of any fees, commissions, or other transaction costs associated with your forex trading. These expenses can be used to offset your taxable income, so it is essential to report them accurately.

When it comes to reporting your forex trading income for tax purposes, it is recommended to consult with a qualified tax professional or accountant who specializes in forex trading. They can help you navigate the complexities of tax laws and ensure that you are reporting your income correctly.

Typically, forex trading income is subject to income tax in the UK. The rate of tax you pay will depend on your total income and tax bracket. If you are trading forex as a full-time business and not just as a hobby, your forex trading income may also be subject to National Insurance contributions.

When filing your tax return, you will usually report your forex trading income as part of your self-employment income. If you are trading forex as a hobby, the income may be reported as miscellaneous income or capital gains. Again, consulting with a tax professional is advisable to ensure accurate reporting.

In conclusion, reporting and documenting your forex trading income is essential to meet your legal obligations and ensure compliance with UK tax laws. Keeping accurate records and consulting with a qualified tax professional will help you navigate the complexities of taxation and avoid any penalties or legal issues. Remember, transparency and accuracy are key when it comes to reporting your forex trading income.

In the UK, forex trading is treated as speculation, and any profits made through forex trading are subject to capital gains tax.

Forex trading is considered an investment activity in the UK. However, if trading is done on a regular and substantial basis, it may be considered a business and subject to different tax rules.

No, if you make a loss on your forex trades, you will not owe any taxes. However, you can use your losses to offset any capital gains you may have made in other investments.

Yes, forex traders in the UK can benefit from the capital gains tax allowance, which allows individuals to earn a certain amount of capital gains tax-free each year. This can help reduce the tax burden on forex trading profits.

Yes, it is important to keep accurate and detailed records of all your forex trades for tax purposes. This includes information such as the date of the trade, the amount of the trade, the currency pair traded, and the profit or loss made. These records will help you calculate and report your taxable income correctly.

Yes, forex trading profits are subject to taxation in the UK. However, the tax treatment depends on whether you are trading as a hobby or as a business.

Beginners’ Guide: Trading with 100 Rupees Trading in the stock market can be an exciting and potentially lucrative endeavor. While many people assume …

Read Article

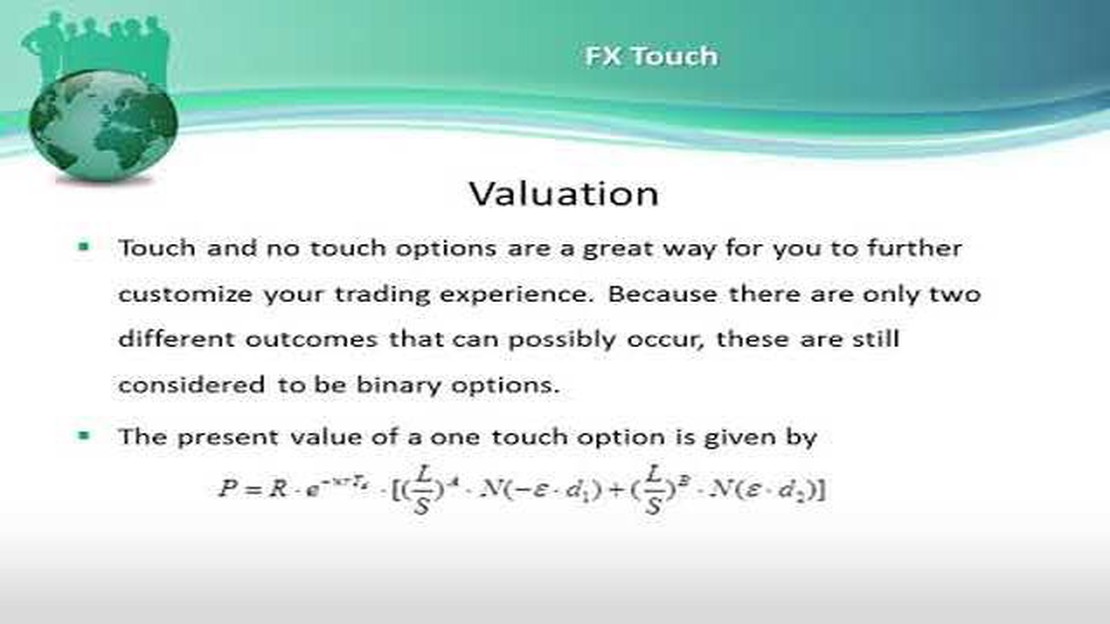

Understanding Touch Options: A Complete Guide Touch options are a type of financial instrument that offers a unique way of trading. They provide …

Read Article

Stocks and Divorce: Can They Be Included in a Settlement? Divorce can be a complex and contentious process, especially when it comes to dividing …

Read Article

What Are Some Examples of Delta Hedging Options? Options are financial derivatives that give their holder the right, but not the obligation, to buy or …

Read Article

What is forex application? Forex, also known as foreign exchange, is the global decentralized market for trading various currencies. It is the largest …

Read Article

Reasons Behind the Depreciation of the AUD The Australian dollar (AUD) has experienced a significant drop in value over recent months, leading many to …

Read Article