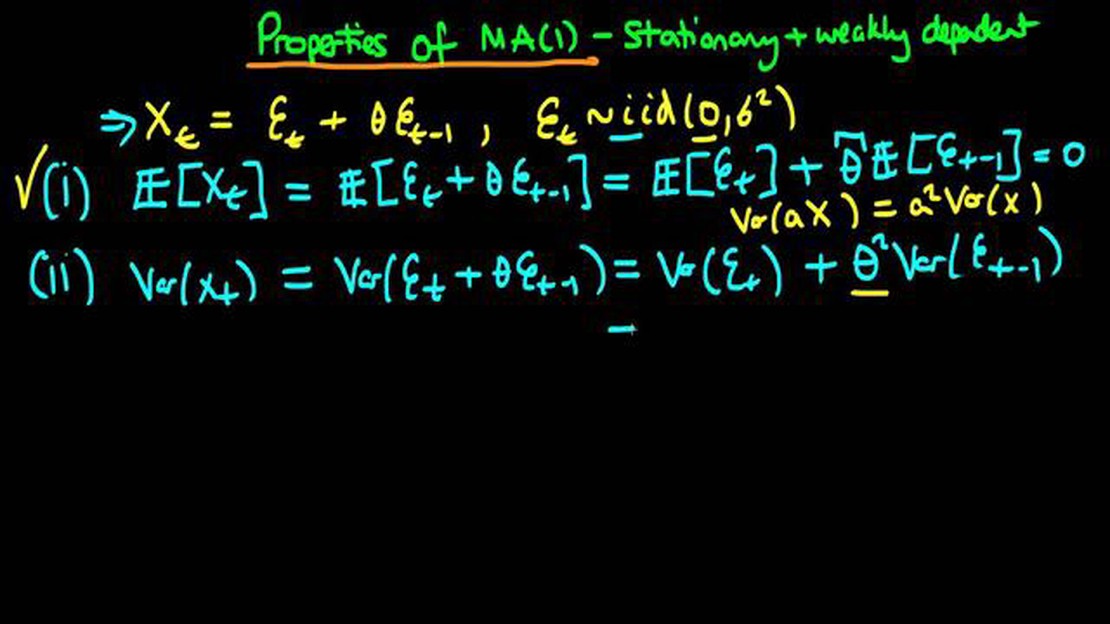

Exploring the Stationarity of Moving Averages: Are They Always Stationary?

Are moving averages always stationary? In the field of time series analysis, moving averages are widely used for smoothing data and identifying …

Read Article

Stock options are a popular method of compensating employees, especially in the technology and startup industries. However, understanding how to properly identify and account for the compensation expense from stock options can be a complex task for both employees and employers.

Compensation expense from stock options is the cost that a company incurs when it grants stock options to its employees. This cost is then recognized over a period of time, typically the vesting period of the options. It is important to accurately identify and account for this expense in order to properly reflect the financial position and performance of the company.

There are several factors that need to be considered when identifying compensation expense from stock options. One such factor is the fair value of the options at the grant date. The fair value is typically determined using a mathematical model, such as the Black-Scholes model, which takes into account factors such as the stock price, exercise price, expected volatility, and expected term of the options.

Another factor to consider is the vesting period of the options. The vesting period is the length of time that an employee must wait before they can exercise their options and receive the underlying stock. During this period, the compensation expense is recognized and accrued on the company’s financial statements. Once the options have vested, the expense is no longer accrued, and any further changes in the fair value of the options are recognized as a gain or loss in the company’s income statement.

Understanding how to properly identify compensation expense from stock options is crucial for both employees and employers. Employees need to be aware of the potential financial impact of stock options on their personal finances, while employers need to accurately account for and disclose the compensation expense in their financial statements. By having a clear understanding of these concepts, both parties can make informed decisions regarding stock options.

A stock option is a financial instrument that gives an individual or employee the right to buy shares of company stock at a specified price, known as the strike price, within a certain period of time. Stock options are often used as an incentive for employees, as they provide the potential for financial gain if the company’s stock price rises.

There are two main types of stock options: incentive stock options (ISOs) and non-qualified stock options (NSOs). ISOs are typically offered to key employees and have certain tax advantages, while NSOs are more commonly issued to all employees and do not have the same tax benefits.

When an employee is granted stock options, the company must determine the fair value of the options and record this as compensation expense on its income statement. This expense is typically spread out over the vesting period, which is the time it takes for the employee to fully own the options.

It is important to properly account for stock option expenses, as they can have a significant impact on a company’s financial statements. In addition to the income statement, stock option expenses are also recorded on the company’s balance sheet and statement of cash flows.

| Advantages of Stock Options | Disadvantages of Stock Options |

|---|---|

| Employees have the potential for financial gain if the company’s stock price rises. | Stock options can become worthless if the company’s stock price decreases. |

| Stock options can be used as a recruiting and retention tool for employees. | There may be restrictions on when and how the stock options can be exercised. |

| Stock options align the interests of employees with those of shareholders. | Stock options can dilute the ownership percentage of existing shareholders. |

Read Also: Should You Let Options Expire? Understanding the Pros and Cons

Overall, stock options can be a valuable tool for companies to incentivize and reward employees. However, it is important for both employees and employers to understand the potential risks and benefits associated with stock options.

When employees receive stock options as part of their compensation package, a company must account for the value of these options as an expense in its financial statements. This expense, known as compensation expense, represents the cost to the company of granting the stock options to its employees.

Compensation expense is recognized over the vesting period of the options, which is the period of time over which employees earn the right to exercise their options. The expense is typically recognized straight-line over the vesting period, although there are alternative methods of recognition that can be used, such as accelerated recognition or proportional recognition based on performance targets.

The value of the options is usually determined using an option pricing model, such as the Black-Scholes model, which takes into account factors such as the current stock price, the exercise price of the options, the expected volatility of the stock, and the time remaining until the options expire. This valuation is then used to calculate the total compensation expense associated with the options.

Once the compensation expense is determined, it is recorded on the income statement as an operating expense. It is also recorded as an increase in the equity of the company, specifically in a separate account called “stock-based compensation expense” or “stock compensation expense.” This allows investors and other stakeholders to see the impact of the stock options on the company’s financial performance and position.

It is important for companies to carefully account for compensation expense from stock options, as it can have a significant impact on their financial statements. Failing to properly recognize and measure this expense can result in inaccurate financial reporting and potential noncompliance with accounting standards.

Read Also: How to calculate a moving average in time series analysis

There are several methods that companies can use to identify compensation expense from stock options. These methods help companies accurately record the cost of providing stock options to their employees.

Regardless of the method used, it is important for companies to consistently apply the chosen method and regularly reassess the assumptions and inputs used in the calculation to ensure the accuracy of the compensation expense recognized. By using an appropriate method, companies can properly identify and record the cost of providing stock options to their employees.

Stock option compensation is a form of payment that companies offer to employees in the form of stock options. These options give employees the right to purchase a certain number of shares at a predetermined price within a specified period of time.

Companies offer stock option compensation as a way to attract and retain talented employees. By offering employees the opportunity to own a stake in the company, companies can align the interests of employees with those of shareholders and incentivize employees to work towards the company’s success.

Compensation expense from stock options is calculated using a fair value method. The fair value is determined at the grant date and is based on factors such as the current market price of the stock, the exercise price of the options, the expected term of the options, and any expected dividends. The expense is then recognized over the vesting period of the options.

Accounting regulations, such as ASC 718 in the United States, require companies to record compensation expense from stock options in their financial statements. The expense is typically recorded in the income statement as a separate line item, and it is also disclosed in the footnotes of the financial statements.

The recognition of compensation expense from stock options impacts a company’s financial statements by increasing its expenses and reducing its net income. This can have an impact on key financial ratios, such as earnings per share, and can also affect the company’s overall financial performance and profitability.

Stock options are a type of benefit that companies offer to their employees, allowing them to purchase company stock at a specific price within a certain time frame. The purpose of stock options is to provide employees with an incentive to contribute to the company’s success and align their interests with those of the shareholders.

When a company grants stock options to its employees, they are treated as an expense on the company’s income statement. The value of the stock options is determined using a recognized accounting model, such as the Black-Scholes model, and is recognized as an expense over the vesting period of the options. This is done to reflect the cost to the company of providing this benefit to its employees.

Are moving averages always stationary? In the field of time series analysis, moving averages are widely used for smoothing data and identifying …

Read Article

How to Determine if a Trade Company is Legitimate When it comes to engaging in business transactions, it is crucial to ensure that the trade company …

Read Article

Get a 50% Bonus on OctaFX Today! Are you looking for a way to increase your trading potential? Look no further! OctaFX is offering a fantastic …

Read Article

Which Bank Offers the Best Currency Exchange Rates? When it comes to exchanging currencies, finding the best rates can save you a significant amount …

Read Article

Is Blackbox stocks free? If you’re interested in trading stocks and are considering using Blackbox Stocks, one of the questions you may have is …

Read Article

What is the formula for the price action indicator? The price action indicator is a popular tool used by traders and investors to analyze market …

Read Article