When Were Binary Options Introduced? The Start of Binary Options Trading

When Did Binary Options Start? Binary options, a type of financial instrument, have become increasingly popular over the years. But when were they …

Read Article

Employee Retirement Income Security Act (ERISA) is a federal law that sets minimum standards for retirement plans and other employee benefit plans offered by private employers. The main purpose of ERISA is to protect the rights and interests of employees who participate in these plans. One important aspect of ERISA regulations is its impact on stock plans.

Stock plans, such as employee stock ownership plans (ESOPs) and stock option plans, are popular tools that companies use to incentivize and reward their employees. These plans allow employees to buy or receive shares of their employer’s stock as part of their compensation package. However, ERISA regulations impose specific requirements and responsibilities on companies that offer stock plans to their employees.

Under ERISA, companies that offer stock plans must act as fiduciaries, meaning they must adhere to certain standards of responsibility and loyalty in managing these plans. They have a duty to act in the best interest of plan participants, prudently manage the plan’s assets, and provide participants with accurate and timely information about the plan. Failure to meet these fiduciary responsibilities can result in legal consequences for the company.

In addition to these fiduciary responsibilities, ERISA also requires companies to provide certain disclosures and notices to participants in stock plans. These include information about the plan’s terms and features, the risks associated with investing in company stock, and the participants’ rights and options. By providing these disclosures, ERISA aims to ensure that participants have the information they need to make informed decisions about their stock plan investments.

Overall, understanding ERISA regulations is crucial for companies that offer stock plans to their employees. By complying with these regulations, companies can protect the rights and interests of their employees and avoid potential legal issues. Conversely, failure to comply with ERISA requirements can lead to significant financial and reputational consequences for companies.

ERISA, or the Employee Retirement Income Security Act, is a federal law that sets standards for pension plans and other employee benefit plans offered by private employers. The purpose of ERISA is to protect employees’ rights and ensure the financial stability of their retirement and welfare plans.

ERISA regulates various aspects of employee benefit plans, including eligibility, participation, vesting, funding, fiduciary responsibilities, disclosure requirements, and plan termination. It applies to both retirement plans, such as pensions and 401(k) plans, and welfare benefit plans, including health insurance and disability plans.

One of the key provisions of ERISA is the requirement for plan sponsors to provide participants with comprehensive information regarding their benefits. This includes details about plan features, funding, investment options, and the rights and responsibilities of participants. ERISA also establishes fiduciary standards that require plan sponsors and other parties involved in the administration of benefit plans to act in the best interests of the participants.

ERISA also outlines the rules and regulations for vesting, which determines when employees have a non-forfeitable right to their accrued benefits. The law sets minimum vesting requirements that employers must meet, ensuring that employees have a vested interest in their retirement benefits after a certain period of service.

Read Also: Will the Iraqi Dinar Revalue? Exploring the Possibility of a Currency Revaluation

In addition to these requirements, ERISA imposes reporting and disclosure obligations on plan sponsors. They are required to file an annual report, known as the Form 5500, which provides detailed information about the plan’s financial condition, operations, and investments. This information is made available to participants and the public, promoting transparency and accountability in the administration of employee benefit plans.

Overall, ERISA regulations play a vital role in safeguarding the interests of employees and ensuring the positive management of retirement and welfare benefit plans. Compliance with these regulations is essential for employers to avoid legal liabilities and provide their employees with adequate retirement security and welfare benefits.

The Employee Retirement Income Security Act (ERISA) is a federal law that sets standards for employer-sponsored retirement and employee benefit plans. It was enacted in 1974 to protect the interests of employees participating in these plans. ERISA regulations aim to ensure that employees receive the benefits promised to them and that the plans are managed in a responsible and transparent manner.

Here are some key points to understand about ERISA regulations:

Read Also: Understanding the Meaning and Significance of a Tweezer Bottom Pattern

Compliance with ERISA regulations is important for employers and plan sponsors to avoid legal and financial consequences. Understanding the basics of ERISA regulations can help employers navigate the complexities of offering retirement and employee benefit plans while ensuring the protection of their employees’ interests.

ERISA stands for the Employee Retirement Income Security Act, which is a federal law that sets minimum standards for pension and health plans offered by private employers. ERISA regulations can impact stock plans because they require certain disclosures, fiduciary responsibilities, and reporting requirements for companies offering employee stock purchase plans, stock option plans, and other equity compensation plans.

The key requirements of ERISA regulations for stock plans include the provision of plan documents to participants, fiduciary responsibilities, reporting and disclosure requirements, and prohibited transactions.

Some examples of fiduciary responsibilities under ERISA for stock plans include prudently selecting and monitoring plan investments, diversifying plan investments to minimize risk, ensuring the payment of plan expenses is reasonable, and providing appropriate disclosures to participants.

ERISA regulations can impact the design of stock plans by requiring certain features or restrictions. For example, ERISA may require a vesting schedule for stock options or employee stock purchase plans, limitations on employer contributions to stock plans, or restrictions on withdrawal or transfer of stock plan assets.

If a company fails to comply with ERISA regulations for their stock plans, they may face penalties, fines, or legal action. The company may be required to make corrective actions, such as providing additional disclosures to participants, amending plan documents, or reimbursing losses suffered by participants as a result of non-compliance.

ERISA stands for the Employee Retirement Income Security Act. It is a federal law that establishes standards for employee benefit plans, including retirement and health plans, to protect the interests of plan participants and beneficiaries.

When Did Binary Options Start? Binary options, a type of financial instrument, have become increasingly popular over the years. But when were they …

Read Article

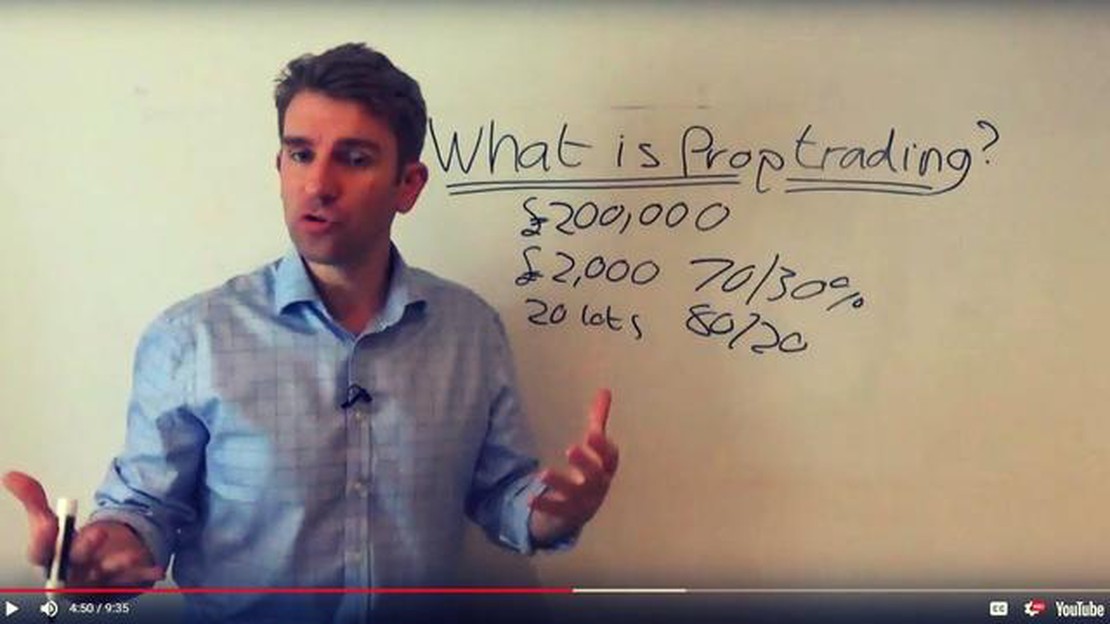

Understanding the Profit Model of Proprietary Trading Firms Proprietary trading firms, also known as prop shops, are financial institutions that …

Read Article

Understanding 0.1 Lot Size in Octafx: A Detailed Explanation In the world of forex trading, lot size is a crucial concept that every trader needs to …

Read Article

Forex Trading during the London Open hour The London open is a crucial time for forex traders around the world. As one of the major financial centers, …

Read Article

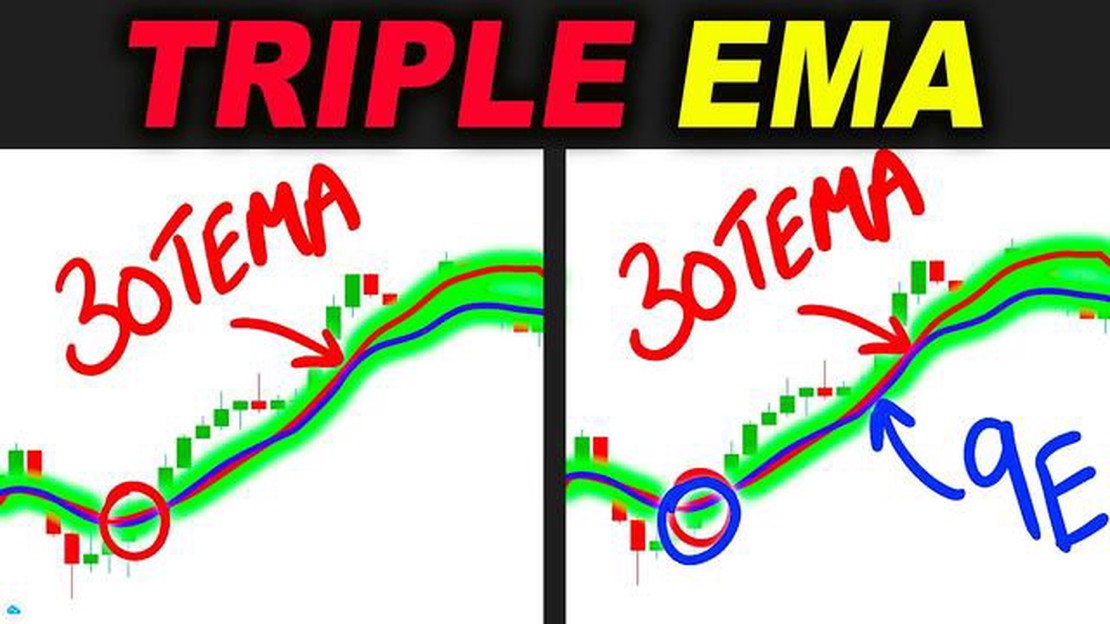

What is the triple moving average? The triple moving average is a technical analysis tool that can greatly improve your trading strategy. It involves …

Read Article

What is the daily chart strategy in forex? Forex trading is a complex and highly volatile market, with numerous strategies available to traders. One …

Read Article