Understanding Futures and Options in HDFC Securities: A Comprehensive Guide

Futures and Options in HDFC Securities: A Comprehensive Guide When it comes to investing in the stock market, it’s essential to have a good …

Read Article

Employee stock options (ESOs) are a popular form of compensation that companies use to attract and retain talented employees. ESOs offer employees the right to purchase company stock at a predetermined price, known as the strike price, within a specified time frame. When employees exercise their stock options, it has a significant impact on the accounting equation of both the company and the employee.

When an employee exercises their stock options, the company’s equity increases while its liabilities decrease. This is because the company is effectively transferring ownership of its stock to the employee, which increases the company’s equity. At the same time, the company’s liabilities decrease because it no longer owes the employee the right to purchase the stock at a future date.

From the employee’s perspective, exercising stock options impacts their personal wealth and financial position. When employees exercise their stock options, they are essentially purchasing company stock at the strike price. If the current market price of the stock is higher than the strike price, the employee can sell the stock and make a profit. However, if the market price is lower than the strike price, the employee may choose not to exercise the options as it would result in a financial loss.

Overall, the exercise of employee stock options has a direct impact on the accounting equation for both the company and the employee. It represents a transfer of ownership and affects the equity and liabilities of the company, while also impacting the personal wealth and financial position of the employee. Understanding these effects is crucial for companies and employees alike in managing their financial resources and making informed decisions regarding stock option exercise.

The exercise of employee stock options has a significant impact on the accounting equation of a company. When employees exercise their stock options, it affects both the assets and equity of the company. The accounting equation, which states that assets equals liabilities plus equity, must be adjusted to reflect this change.

Firstly, the exercise of stock options increases the company’s assets. The value of the exercised stock options is recorded as an asset on the balance sheet. This increase in assets represents the value that the employee has received from exercising their options.

On the other side of the equation, the exercise of stock options affects the equity of the company. Equity represents the ownership interest in the company and is equal to the difference between assets and liabilities. When employees exercise their stock options, they are essentially purchasing shares of the company, which increases the equity of the company. This increase in equity reflects the additional ownership interest that the employees now hold in the company.

Additionally, the exercise of stock options may also have an impact on the company’s liabilities. If the stock options are settled in cash, the company may need to increase its liabilities to reflect the cash payment that is required. However, if the stock options are settled through the issuance of shares, there may not be any impact on the liabilities of the company.

In conclusion, the exercise of employee stock options has a significant impact on the accounting equation of a company. It increases the assets and equity of the company, and may also affect its liabilities. Proper accounting and record-keeping are essential to accurately reflect these changes in the company’s financial statements.

| Impact of Employee Stock Option Exercise |

|---|

| Assets |

| Equity |

| Liabilities |

Read Also: What Time Do Futures Options Settle? A Comprehensive Guide

When employees exercise their stock options, it has specific effects on the accounting equation of a company. The accounting equation is a fundamental principle of accounting that states that assets equal liabilities plus equity.

3. Effect on Equity: Exercising stock options affects equity in two ways. First, it increases the company’s common stock account, which is part of equity. This is because the employee receives shares of the company’s stock when exercising their options, and these shares are recorded as an increase in common stock. Second, exercising stock options can also have an impact on retained earnings. If the exercise price is higher than the market price of the stock, the company may record a charge to its income statement, which reduces retained earnings.

Overall, the exercise of employee stock options affects the accounting equation by increasing assets and equity. It has no direct effect on liabilities, but it can indirectly impact retained earnings through charges or gains recorded on the income statement.

Employee stock option exercises can have significant financial implications for companies. When employees exercise their stock options, it affects the company’s financial statements in several ways:

Read Also: Understanding the Key Concept of Indicators: A Comprehensive Guide

In summary, the financial implications of employee stock option exercises can impact a company’s profitability, ownership structure, equity, and cash flow. Companies need to carefully consider these implications when designing and administering employee stock option plans.

The impact of employee stock option exercise on the accounting equation is that it reduces the company’s liabilities and increases its equity. When an employee exercises their stock options, the company is obligated to issue new shares of stock, which reduces the outstanding stock option liability and increases the shareholders’ equity.

Employee stock option exercise affects a company’s balance sheet by reducing the liabilities and increasing the shareholders’ equity. When an employee exercises their stock options, the company is obligated to issue new shares, which reduces the outstanding stock option liability and increases the equity section of the balance sheet. This increases the company’s net assets and reflects the value received by the employees.

The accounting treatment of employee stock option exercise involves recording the fair value of the stock options granted as an expense over the vesting period. When the options are exercised, the company debits the stock option liability and credits the stockholder’s equity for the fair value of the shares issued. This reduces the liabilities and increases the shareholders’ equity on the balance sheet.

The impact on the income statement when an employee exercises their stock options is the recognition of stock-based compensation expense. This expense is recorded over the vesting period of the options and is included in the income statement as a separate line item. The recognition of this expense reduces the company’s net income and therefore affects its profitability.

Employee stock option exercise affects the financial position of a company by increasing the shareholders’ equity and decreasing the liabilities. When an employee exercises their stock options, the company issues new shares, which increases the equity and reflects the value received by the employees. Additionally, the liabilities are reduced as the outstanding stock option liability decreases.

The accounting equation, also known as the balance sheet equation, is a fundamental principle in accounting that represents the relationship between a company’s assets, liabilities, and shareholders’ equity. It is expressed as: Assets = Liabilities + Shareholders’ Equity.

Employee stock options can impact the accounting equation in several ways. When an employee exercises their stock options, it increases the company’s liabilities by the value of the stock options exercised. At the same time, it increases shareholders’ equity by the same amount. This is because the employee now owns stock in the company, which represents an ownership interest and contributes to shareholders’ equity. The impact on assets depends on the method of payment for the exercise, such as cash or shares, and any associated taxes or fees.

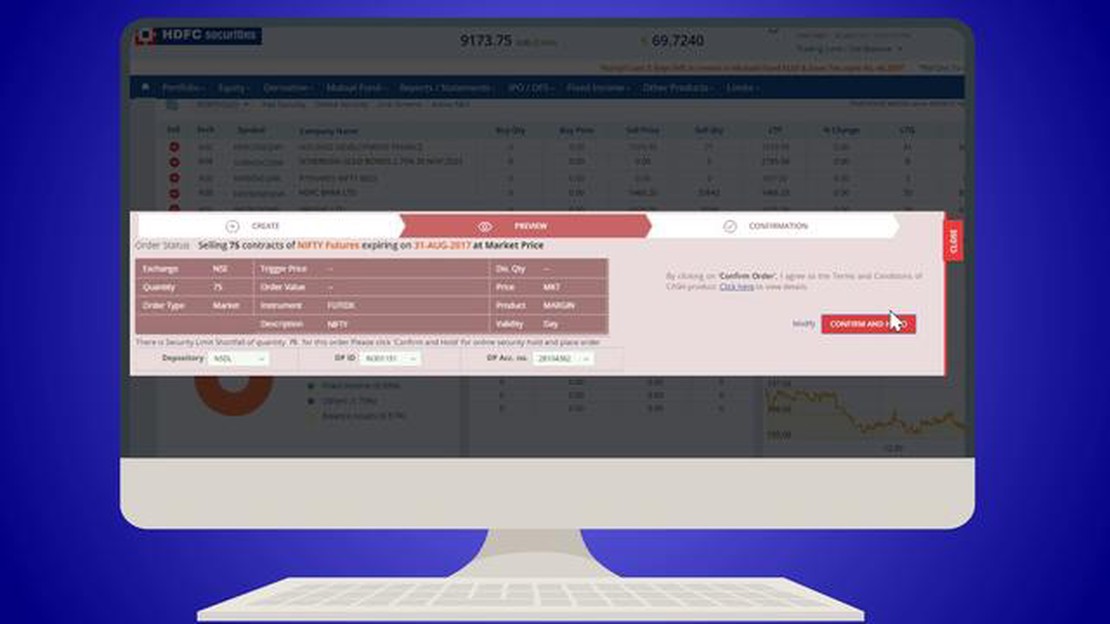

Futures and Options in HDFC Securities: A Comprehensive Guide When it comes to investing in the stock market, it’s essential to have a good …

Read Article

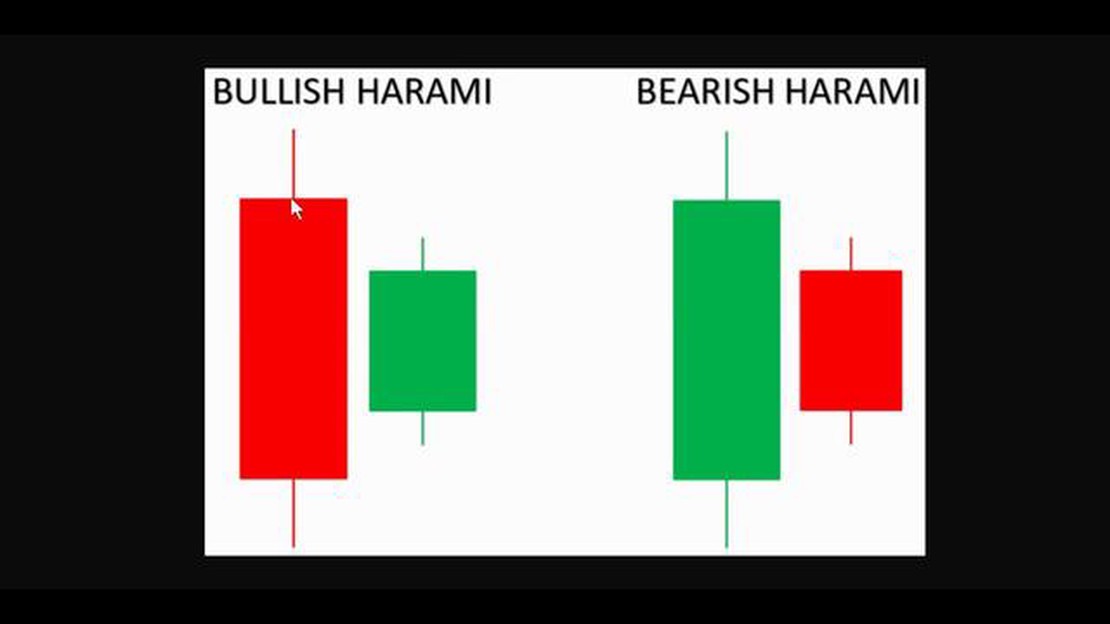

Is Bullish Harami a Reliable Candlestick Pattern? Bullish Harami is a popular candlestick pattern used by traders to identify possible trend reversals …

Read Article

Choosing the Best Timeframe for Scalping Forex Markets Scalping is a popular trading strategy that involves making small, quick trades in order to …

Read Article

What are the forex market hours today in the UK? Are you interested in trading on the foreign exchange market? One important factor to consider when …

Read Article

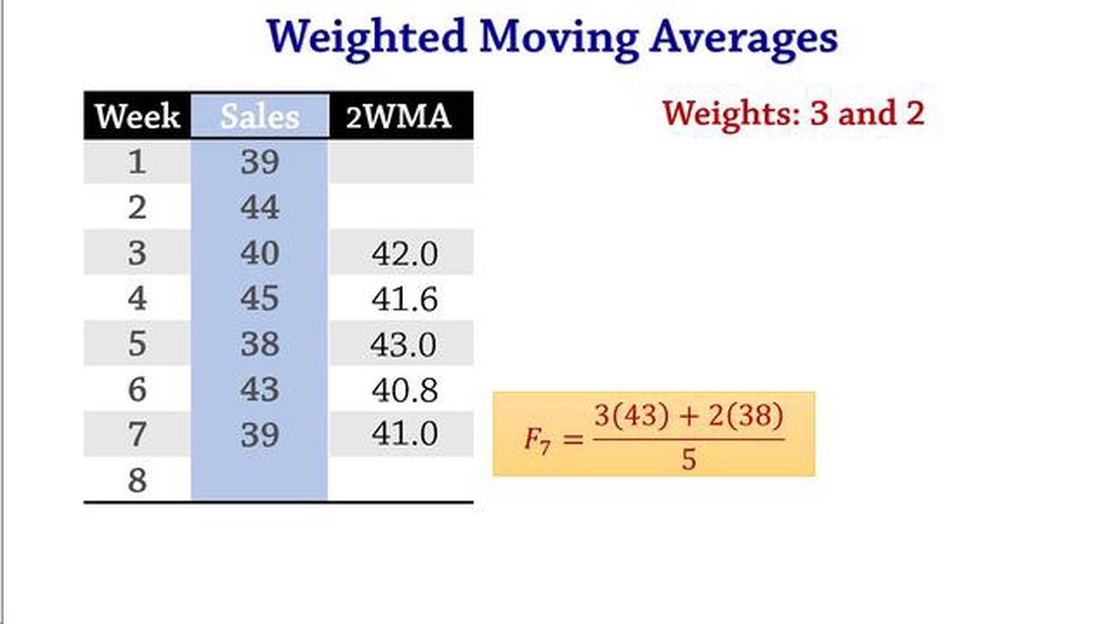

Understanding the distinction between weighted moving average and exponential smoothing Forecasting and analyzing data play crucial roles in …

Read Article

The Benefits of M Stock Discover the Advantages of Investing in M Stock M Stock Benefits Investing in M Stock can provide numerous benefits and …

Read Article