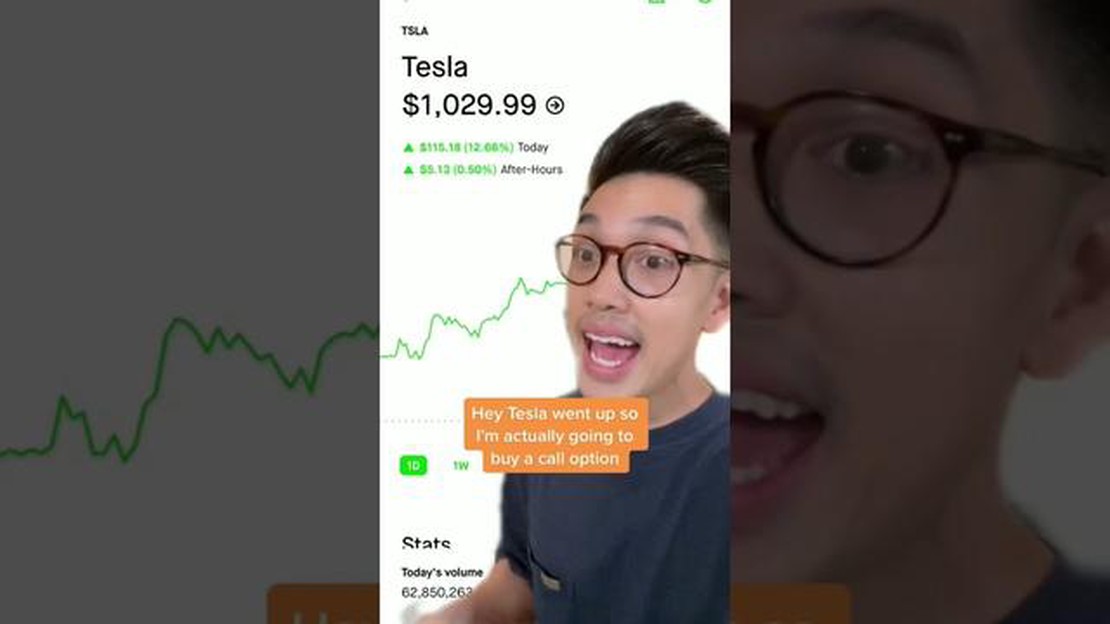

Is Tesla a stock option or RSU? Understanding Tesla's compensation plans

Understanding Tesla Options: Stock or RSU? In recent years, Tesla has become one of the most talked-about companies in the world. Known for its …

Read Article

The Reserve Bank of India (RBI) is the central banking institution of India and plays a crucial role in maintaining financial stability in the country. As part of its responsibilities, the RBI has introduced guidelines for risk management to ensure the safety and soundness of the banking system.

Risk management is a critical aspect of banking operations, as it helps banks identify, assess, and mitigate various types of risks that they are exposed to. The RBI’s guidelines provide comprehensive frameworks and principles to help banks effectively manage risks such as credit risk, market risk, operational risk, liquidity risk, and interest rate risk.

One of the key objectives of RBI’s risk management guidelines is to enhance the resilience of banks and protect them from financial shocks. By implementing effective risk management practices, banks can reduce the likelihood of losses and strengthen their ability to withstand adverse economic conditions.

The RBI’s guidelines also emphasize the importance of creating a strong risk management culture within banks. This involves establishing clear risk governance structures, defining risk tolerance thresholds, and promoting risk awareness and accountability among employees at all levels.

In conclusion, RBI’s guidelines for risk management are designed to ensure the stability and resilience of the Indian banking system. By adhering to these guidelines, banks can better protect themselves from various risks and contribute to the overall financial stability of the country.

When it comes to risk management, the Reserve Bank of India (RBI) plays a crucial role. As the central banking institution of the country, the RBI is responsible for maintaining financial stability and ensuring the overall soundness of the banking system.

One of the key roles of the RBI in risk management is to develop and enforce guidelines and regulations for banks and financial institutions. These guidelines cover various aspects of risk management, including credit risk, market risk, operational risk, and liquidity risk.

The RBI also monitors and assesses the risk management practices of banks to identify any potential vulnerabilities and ensure that they are taking appropriate measures to mitigate risks. This includes conducting regular inspections and audits of banks’ risk management frameworks and processes.

Furthermore, the RBI provides guidance and support to banks in building robust risk management systems. This includes encouraging the adoption of best practices, providing training programs for bank employees, and promoting the use of technology and data analytics to improve risk management capabilities.

In addition, the RBI acts as a lender of last resort during times of financial stress. It provides liquidity support to banks to ensure the stability of the financial system and prevent any potential contagion effects. This role of the RBI helps in managing systemic risk and maintaining overall financial stability.

Read Also: 7 Effective Ways to Promote Your Forex Affiliate Program

In summary, the RBI plays a critical role in risk management by developing and enforcing guidelines, monitoring and assessing risk management practices, providing guidance and support to banks, and acting as a lender of last resort. Its efforts are aimed at maintaining the stability and soundness of the banking system, which is essential for the overall health of the economy.

The Reserve Bank of India (RBI) has issued comprehensive guidelines on risk management for banks and financial institutions. These guidelines aim to ensure that banks have robust risk management practices in place, in order to maintain financial stability and protect the interests of depositors and other stakeholders.

Read Also: Is $25,000 needed to trade options successfully?

Key elements of RBI’s risk management guidelines include:

By adhering to these key elements of RBI’s risk management guidelines, banks can enhance their risk management capabilities and ensure a safe and resilient financial system.

Implementing and complying with RBI (Reserve Bank of India) guidelines is crucial for organizations in managing risk effectively. These guidelines provide a framework for risk management practices while ensuring financial stability and security in the banking sector. Compliance with these guidelines not only helps in instilling transparency and accountability but also in building trust among stakeholders.

Here are some key points to consider for implementation and compliance with RBI guidelines:

By implementing and complying with RBI guidelines, organizations can demonstrate their commitment to sound risk management practices and contribute to the overall stability and resilience of the banking sector.

The RBI Guidelines for Risk Management are a set of rules and regulations issued by the Reserve Bank of India (RBI) that outline how banks and financial institutions should identify, assess, and manage different types of risks they face.

The RBI Guidelines for Risk Management are important because they provide a framework for banks and financial institutions to effectively manage various risks, such as credit risk, market risk, operational risk, and liquidity risk. By following these guidelines, banks can ensure the stability and integrity of the financial system.

The key components of the RBI Guidelines for Risk Management include the establishment of a comprehensive risk management framework, the identification and assessment of various risks, the development of risk management policies and procedures, the implementation of risk mitigation strategies, and the monitoring and reporting of risk exposure.

Non-compliance with the RBI Guidelines for Risk Management can have serious consequences for banks and financial institutions. The RBI has the authority to impose penalties, fines, and other disciplinary measures on non-compliant institutions. In extreme cases, the RBI can even revoke a bank’s license to operate.

Understanding Tesla Options: Stock or RSU? In recent years, Tesla has become one of the most talked-about companies in the world. Known for its …

Read Article

CVS Stock Payout: Everything You Need to Know If you are a shareholder of CVS, you may be wondering about the payout for the stock. CVS Health is a …

Read Article

Is Golden Cross a good strategy? When it comes to trading strategies, the golden cross is one that has gained significant attention in the financial …

Read Article

The Tax Treatment of NSO: Understanding the Basics Non-Qualified Stock Options (NSOs) are a type of stock option that is more commonly offered to …

Read Article

Philippine Peso Forecast: Will it Rise or Fall? The Philippine Peso, the official currency of the Philippines, has been the subject of intense …

Read Article

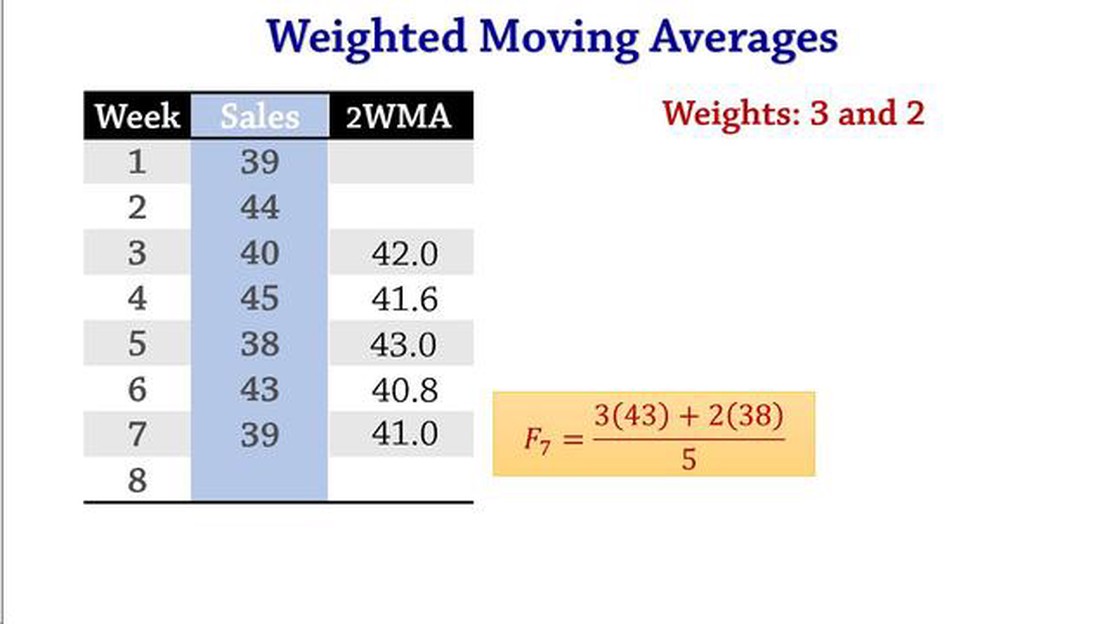

Understanding the Weighted Moving Average: What Does It Indicate? The weighted moving average is a widely used statistical technique that provides …

Read Article