When is the share sale tax not paid? Understanding the exemptions and exceptions

Exemptions from Share Sale Tax: When is it Not Paid? When selling shares, it is usually expected that a capital gains tax will be assessed on any …

Read Article

CVA (Credit Valuation Adjustment) is a measure used in financial risk management to assess the potential loss from credit exposure in derivative portfolios. It quantifies the risk of counterparty default and provides an estimate of the cost of hedging that risk. Accurate measurement of CVA is crucial for financial institutions to mitigate their credit risk and make informed trading decisions.

There are various methods and techniques employed to measure CVA, each with its strengths and limitations. One commonly used approach is the Monte Carlo simulation, which models the future value of a derivative portfolio based on different scenarios of creditworthiness. By simulating the possible outcomes, this method provides a distribution of potential future exposures and allows for a more accurate estimation of CVA.

Another popular method is the analytical method, which involves using mathematical formulas and models to calculate CVA. This approach is more computationally efficient than Monte Carlo simulation but may rely on certain assumptions and simplifications that can affect the accuracy of the results.

In addition to these methods, there are also hybrid approaches that combine elements of both Monte Carlo simulation and analytical methods. These hybrid models aim to strike a balance between accuracy and computational efficiency, taking advantage of the strengths of each approach. They may incorporate factors such as correlation, collateral, and wrong-way risk to provide a more comprehensive assessment of CVA.

Measuring CVA is a complex task that requires a deep understanding of financial markets, credit risk, and mathematical modeling. It involves making assumptions, managing data, and running complex calculations. The choice of method and technique depends on various factors, such as the type of derivative portfolio, the availability of data, and the resources and expertise of the financial institution. By employing robust and accurate measurement methods, financial institutions can effectively manage their credit risk and protect against potential losses.

CVA stands for Credit Valuation Adjustment, and it is a measure of the credit risk associated with a financial contract. It represents the potential loss a counterparty may incur due to the default of the other counterparty involved in the transaction.

CVA is an important metric in financial risk management, especially in the context of over-the-counter (OTC) derivatives. It provides a way to quantify the credit risk exposure of a portfolio of derivative contracts, taking into account factors such as counterparty credit quality, market conditions, and contractual terms.

Measuring CVA involves assessing the probability of default of the counterparty, estimating potential future exposure (PFE), and calculating the expected loss given default (LGD). These calculations can be complex and require sophisticated models, statistical techniques, and market data.

The calculation of CVA helps financial institutions to determine the amount of capital they should allocate for credit risk, as well as to price and hedge derivative contracts. It also provides insights into the overall credit risk profile of the institution and helps in making informed risk management decisions.

Read Also: Understanding the VWAP Technique: A Comprehensive Guide

CVA is an important concept in the field of risk management and plays a significant role in the valuation and risk assessment of derivative contracts. It helps institutions to better understand and manage the credit risk associated with their portfolios, as well as to comply with regulatory requirements.

Measuring the credit valuation adjustment (CVA) is essential for financial institutions to assess and manage the counterparty credit risk associated with over-the-counter (OTC) derivative transactions. CVA quantifies the potential loss that may occur due to a counterparty defaulting on their obligations.

Read Also: Advantages of Trading FX Futures - Why Should You Consider It?

There are several reasons why measuring CVA is of great importance:

In conclusion, measuring CVA is crucial for financial institutions as it enables effective risk management, regulatory compliance, accurate pricing and valuation, stress testing, and informed decision-making regarding risk transfer. By quantifying counterparty credit risk, institutions can make well-informed decisions that drive their overall risk management strategy.

CVA stands for Credit Valuation Adjustment. It is the difference between the risk-free portfolio value and the value of the portfolio taking into account the credit risk. CVA can be used to measure counterparty credit risk in derivative transactions.

There are several methods to measure CVA, including the simulation-based approach, Black-Scholes approximation, and the analytical approach. Each method has its own advantages and limitations, and the choice of method depends on the specific requirements and constraints of the situation.

The simulation-based approach to measuring CVA involves running multiple simulations of the future scenarios to estimate the distribution of the future portfolio value. These scenarios take into account the credit risk of the counterparty. By aggregating the results of these simulations, it is possible to calculate the expected CVA.

The Black-Scholes approximation method is a simplified approach to measure CVA. It assumes a constant credit spread and uses the Black-Scholes model to calculate the expected loss due to counterparty credit risk. While this method is computationally less intensive than the simulation-based approach, it may not capture all the complexities of the credit risk.

The analytical approach to measuring CVA involves using mathematical models and formulas to calculate the expected loss due to counterparty credit risk. This approach can be more efficient than simulation-based methods and provide more accurate results for certain types of portfolios. However, it may require certain assumptions and simplifications.

Exemptions from Share Sale Tax: When is it Not Paid? When selling shares, it is usually expected that a capital gains tax will be assessed on any …

Read Article

How to Identify a Fractal Pattern Welcome to a comprehensive guide on identifying fractal patterns. Fractals are fascinating geometric shapes that …

Read Article

The Profitable Trade During WW1: Exploring Economic Opportunities and Success The outbreak of World War 1 in 1914 brought about a global conflict that …

Read Article

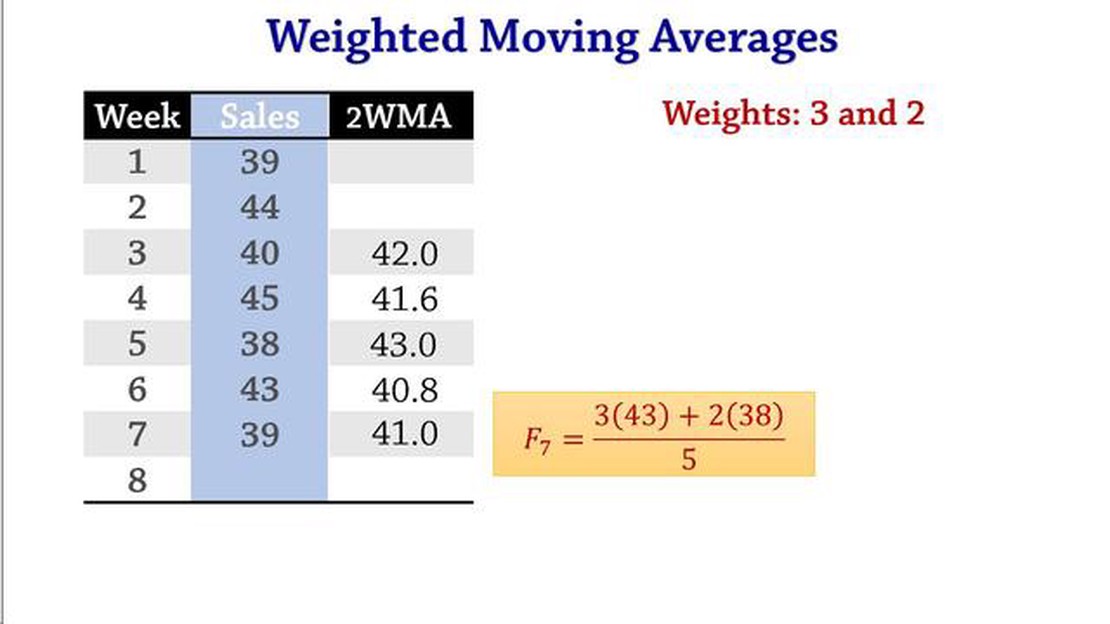

What is a Weighted Moving Average in Demand Forecasting? In demand forecasting, weighted moving averages are a commonly used technique to analyze and …

Read Article

Is it Possible to Buy Dollars on the Forex Market? Forex, which stands for foreign exchange, is the largest financial market in the world. It allows …

Read Article

Is TMGM broker legit? When it comes to choosing a broker, one of the most important factors to consider is legitimacy. With the increasing number of …

Read Article