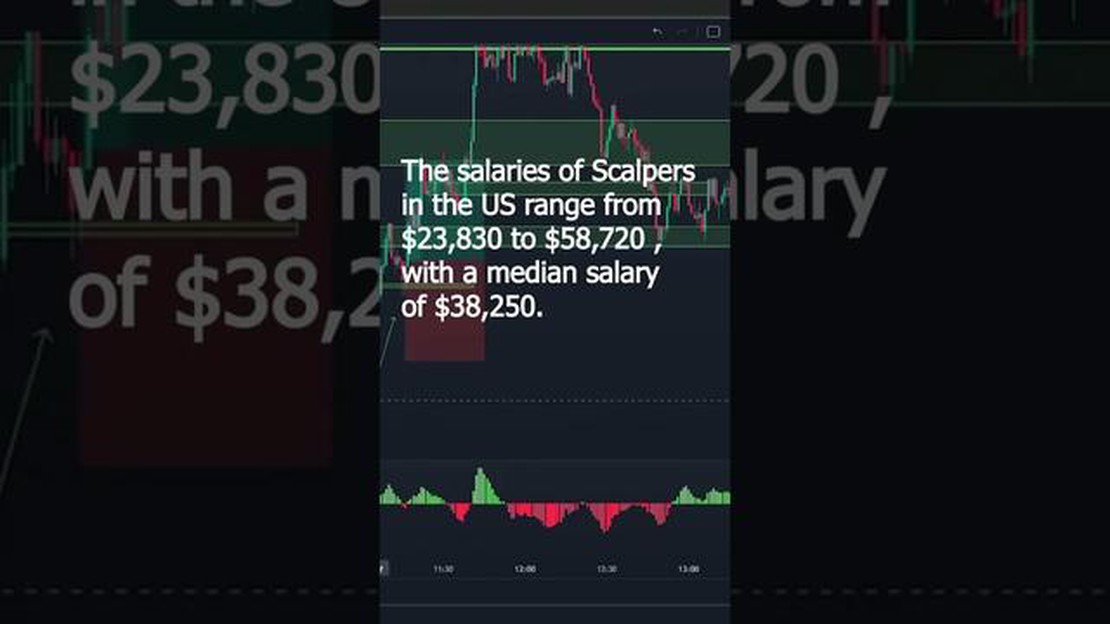

What is the average income of scalpers?

How much does the average scalper make? Scalping is a controversial practice where individuals buy tickets or merchandise at face value and then …

Read Article

Forex trading, also known as foreign exchange trading, has become increasingly popular in the Philippines. Many individuals are attracted to the potential for financial gain from trading currencies. However, it is important to understand the tax implications of forex trading in the Philippines.

One of the key questions for forex traders is whether their gains or losses are taxable. The answer is yes. The Philippines’ Bureau of Internal Revenue (BIR) considers forex trading as an ordinary business activity, and any income derived from it is subject to taxation. This includes both profits and losses incurred in forex trading.

According to the BIR, forex gains or losses should be reported as part of an individual’s annual income tax return. The gains or losses should be included in the computation of the individual’s taxable income and are subject to the corresponding tax rates. It is crucial for forex traders to keep accurate records of their trades and any related expenses to properly report their income to the BIR.

It is also important to note that forex traders in the Philippines may be subject to other taxes, such as value-added tax (VAT) or percentage tax, depending on their annual gross receipts. Forex trading falls under the BIR’s definition of a business, and as such, traders may need to register as self-employed individuals and comply with other tax obligations.

In conclusion, forex gain or loss is taxable in the Philippines. Forex traders need to be aware of their tax obligations and accurately report their income to the BIR. It is advisable to consult with a tax professional or seek guidance from the BIR to ensure compliance with tax laws and regulations.

Foreign Exchange (Forex) trading has become increasingly popular in the Philippines. Traders buy and sell different currencies in the hopes of making a profit. However, when it comes to taxation, many traders are unsure whether their Forex gains or losses are taxable.

The taxability of Forex gains or losses in the Philippines depends on various factors. The Bureau of Internal Revenue (BIR) has specific rules and regulations regarding the taxation of Forex trading. Here are some key points to keep in mind:

Ultimately, the taxability of Forex gains or losses in the Philippines depends on various factors, including the classification of income and the frequency of trading. It is crucial to keep accurate records and consult with tax professionals to ensure compliance with the BIR’s rules and regulations.

Disclaimer: This article is for informational purposes only and should not be considered as legal or tax advice. The BIR’s regulations and guidelines may change over time, so it is essential to stay updated with the latest information from the BIR or consult with tax professionals.

Read Also: What is EOD Date - Explained in Detail

Forex trading, short for foreign exchange trading, is the process of buying and selling currencies in the global foreign exchange market. In the Philippines, forex trading has become increasingly popular among individuals looking to profit from fluctuations in currency exchange rates.

Forex trading in the Philippines is regulated and supervised by the Securities and Exchange Commission (SEC). The SEC ensures that forex brokers are licensed and operate in accordance with the rules and regulations set forth by the commission.

One of the primary benefits of forex trading is its accessibility. Traders can participate in the forex market 24 hours a day, 5 days a week, allowing for flexibility in terms of when and where they trade. Additionally, forex trading requires relatively low capital compared to other investment options, making it an attractive choice for individuals with limited funds.

To start forex trading in the Philippines, individuals must open an account with a licensed forex broker. These brokers provide access to a trading platform that allows traders to execute trades and access real-time market data. Traders can choose from a variety of currency pairs to trade, depending on their preferences and market conditions.

To be successful in forex trading, individuals must have a solid understanding of fundamental and technical analysis. Fundamental analysis involves studying economic indicators and news releases to predict future currency movements. Technical analysis, on the other hand, involves analyzing charts and patterns to identify potential trading opportunities.

Risk management is a crucial aspect of forex trading. Traders should always use stop-loss orders to limit their potential losses and avoid emotional decision-making. It is also important to develop and stick to a trading plan, which includes setting realistic profit targets and risk-reward ratios.

Read Also: Understanding the MFN Trade System and its Benefits

When it comes to taxation of forex trading in the Philippines, it is important to consult a tax professional. While forex trading gains are generally considered taxable income, there may be certain exemptions or deductions that traders can take advantage of. It is essential to comply with the tax regulations in order to avoid any legal issues.

In conclusion, forex trading in the Philippines offers individuals the opportunity to profit from fluctuations in currency exchange rates. It is regulated by the SEC and requires opening an account with a licensed forex broker. Successful trading requires a strong understanding of fundamental and technical analysis, as well as risk management techniques. Traders should consult a tax professional to ensure compliance with tax regulations.

Yes, forex gains or losses are taxable in the Philippines. Any income or gain from forex trading is considered taxable. However, the specific tax laws and rates may vary depending on the type and frequency of trading activity.

Forex gains or losses are taxed as ordinary income in the Philippines. They are subject to the progressive tax rates, which range from 5% to 32%, depending on the individual’s total taxable income for the year.

Yes, you are required to report forex gains or losses in your tax return in the Philippines. It is important to keep track of all your trading activities and report any income or losses accurately to comply with the tax laws.

There are no specific exemptions or deductions for forex gains or losses in the Philippines. However, you may be able to offset your forex losses against other taxable income, subject to certain limitations and conditions. It is recommended to consult with a tax professional for more information.

If you fail to report your forex gains or losses in your tax return, you may be subject to penalties and interest charges. It is important to accurately report all your trading activities to avoid any potential legal or financial consequences.

How much does the average scalper make? Scalping is a controversial practice where individuals buy tickets or merchandise at face value and then …

Read Article

Understanding the Function of the Trading System The trading system plays a crucial role in the modern economy, serving as the backbone of global …

Read Article

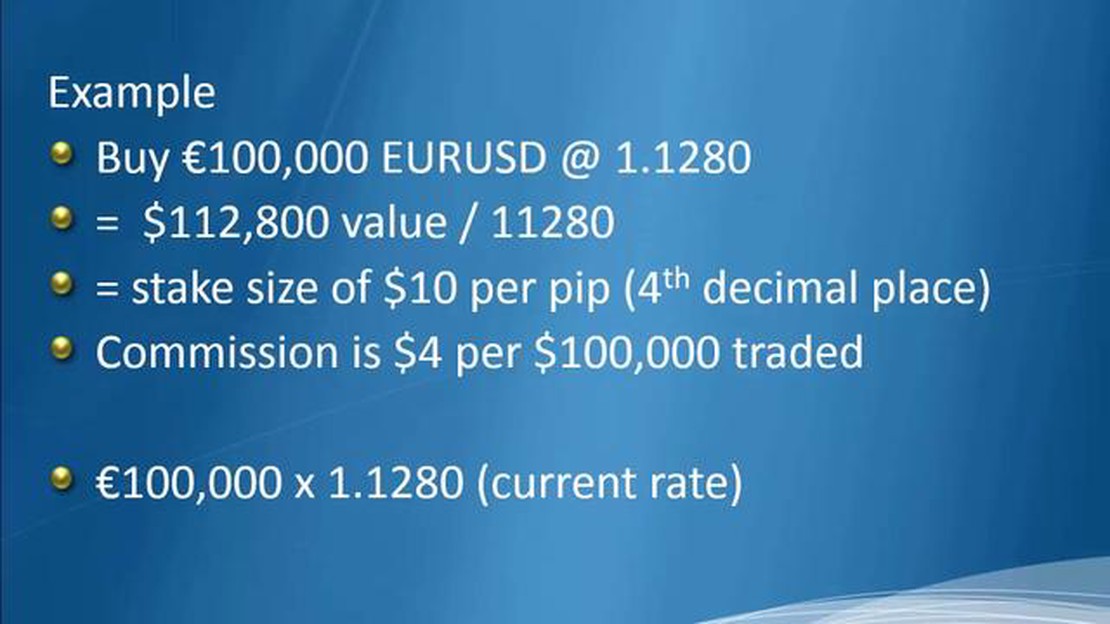

Understanding Forex Commission: What You Need to Know When it comes to trading in the forex market, one crucial aspect that every trader must …

Read Article

4 Indicators for Measuring the Sales Market Measuring the sales market and accurately assessing its performance is essential for any business. Having …

Read Article

Three Elements in a Use Case Diagram A use case diagram is a powerful tool used in software development to visualize and communicate the different …

Read Article

Release Date of Nokia C3 If you are curious to know when the Nokia C3 was released, you have come to the right place. The Nokia C3 is a …

Read Article