Learn how to successfully trade in Nifty options

Beginner’s Guide to Trading Nifty Options Trading in Nifty options can be a great way to generate income and increase your portfolio returns. However, …

Read Article

Inventory management is a crucial aspect of any business, and one key metric that helps businesses track their inventory value is the moving average cost. The moving average cost is a method used to determine the cost of inventory items by averaging the costs of each item over time. This guide will provide a step-by-step explanation of how to calculate the moving average cost of inventory, helping businesses make informed decisions about their inventory management.

Firstly, it is important to understand that the moving average cost is calculated based on the average cost of the inventory items. This average cost includes the purchase price of the items, as well as any additional costs such as shipping or handling fees. By taking into account these additional costs, the moving average cost provides a more accurate representation of the overall cost of the inventory items.

To calculate the moving average cost, one must start with the initial purchase of the inventory items. This initial cost is recorded as the starting inventory value. As new inventory items are purchased, their cost is added to the total inventory value, while the oldest item’s cost is removed. This process continues as new inventory items are purchased and older items are sold or used.

By continuously recalculating the average cost over time, the moving average cost provides a more accurate reflection of the current value of the inventory. This allows businesses to make more informed decisions about pricing, product profitability, and overall inventory management. With the help of this step-by-step guide, businesses can successfully calculate the moving average cost of their inventory and optimize their inventory management strategies.

The moving average cost of inventory is a method used to calculate the average cost of inventory items over a specific period of time. This method takes into account the changes in cost that may occur over time, allowing businesses to more accurately track and value their inventory.

When using the moving average cost method, the cost of each inventory item is recalculated with each new purchase or sale. This ensures that the cost of inventory is updated to reflect the most recent prices and quantities.

Here is a step-by-step guide on how to calculate the moving average cost of inventory:

The moving average cost method can be especially useful for businesses that experience fluctuations in the cost of inventory. By constantly updating the cost of inventory based on recent purchases and sales, businesses can ensure that the value of their inventory accurately reflects market prices.

Read Also: Is GBP JPY a Major Forex Pair?

Implementing the moving average cost method can also help businesses make more informed decisions about pricing, purchasing, and inventory management. By understanding the average cost of their inventory over time, businesses can better assess profitability and overall financial health.

In conclusion, the moving average cost of inventory is an important calculation for businesses to understand. By accurately tracking the cost of inventory over time, businesses can make more informed decisions and better manage their resources.

Calculating the moving average cost of inventory is a crucial step in effectively managing and controlling inventory costs for businesses. The moving average cost is used to determine the value of inventory on hand, track the cost of goods sold, and make informed pricing decisions.

One of the main reasons why calculating the moving average cost of inventory is important is because it provides more accuracy and clarity in understanding the true cost of inventory. It takes into account the fluctuating prices of goods, ensuring that the cost reflects the current market conditions. This allows businesses to accurately assess the profitability and performance of their inventory.

By calculating the moving average cost, businesses can also make more informed pricing decisions. They can determine whether they need to adjust the pricing of their products to maintain desired profit margins. Additionally, it helps in evaluating the impact of changing suppliers or purchasing larger quantities of inventory at different prices.

Another significant benefit of calculating the moving average cost of inventory is its role in cost control. By continuously tracking the average cost, businesses can identify any significant variations and take appropriate actions to manage and control their costs. This allows for better financial planning, budgeting, and forecasting.

In addition to cost control, calculating the moving average cost also assists in inventory management. It provides valuable insights into inventory turnover and helps businesses optimize their stock levels. By analyzing the fluctuations in average cost over time, businesses can identify trends and adjust their procurement strategies accordingly.

Overall, calculating the moving average cost of inventory is essential for businesses to accurately determine the value of their inventory, make informed pricing decisions, manage costs, and effectively optimize their inventory management processes. It provides a comprehensive view of the cost of inventory and allows businesses to stay competitive in the market.

Read Also: Does Hong Kong have a floating exchange rate? - Exploring the currency policy in Hong Kong

The moving average cost of inventory is a method used to calculate the average cost of goods in inventory.

The moving average cost of inventory is calculated by dividing the total cost of goods available for sale by the total number of units available for sale.

The moving average cost of inventory is important because it helps businesses determine the value of their inventory, as well as the cost of goods sold.

The advantages of using the moving average cost method include: it smoothens out the cost of inventory, it is simple to calculate, and it reflects the current market conditions.

Yes, the moving average cost of inventory can be used for tax purposes, as it provides an accurate representation of the cost of goods sold.

The moving average cost is the average cost of all units in inventory, which is recalculated every time a new unit is purchased or sold.

Beginner’s Guide to Trading Nifty Options Trading in Nifty options can be a great way to generate income and increase your portfolio returns. However, …

Read Article

Derivative of the MACD Indicator The MACD (Moving Average Convergence Divergence) is a popular technical indicator used in trading to identify …

Read Article

Philippine Peso Forecast: Will it Rise or Fall? The Philippine Peso, the official currency of the Philippines, has been the subject of intense …

Read Article

How to Track the Status of Your Cargo Shipment If you are waiting for an important cargo shipment, tracking its status is crucial to ensuring its …

Read Article

Why is Polish Zloty getting stronger? The Polish Zloty has been experiencing a steady rise in value against other major currencies, and this trend has …

Read Article

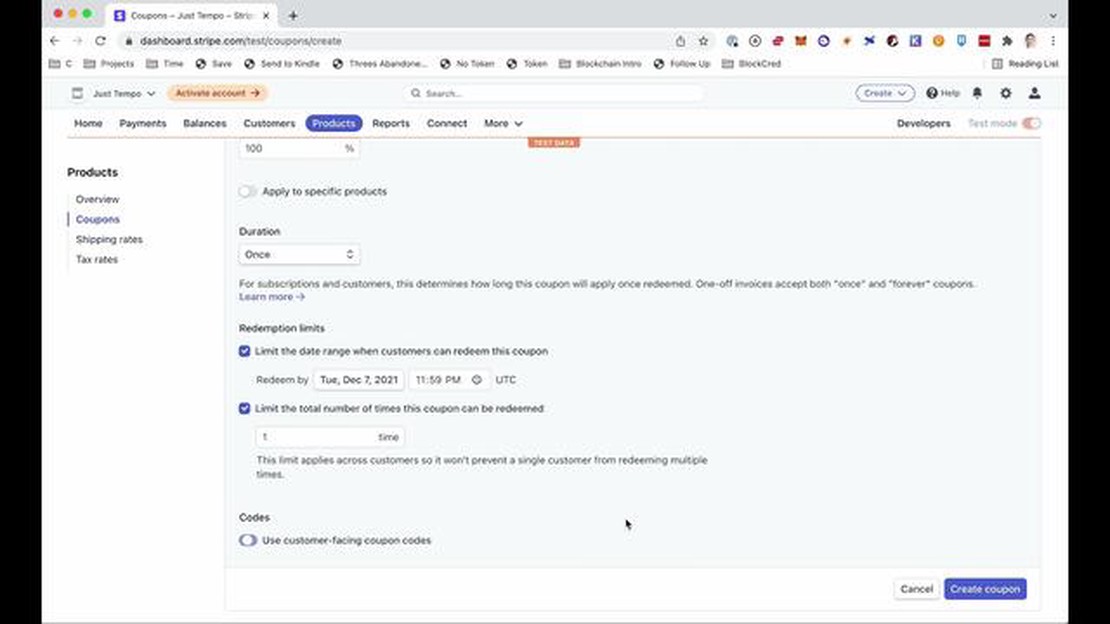

Can Stripe offer a 100% discount? When it comes to running an online business, offering discounts and promotional deals can be a great way to attract …

Read Article