Understanding FX Arbitrage: A Guide to Foreign Exchange Arbitrage Strategies

Understanding FX Arbitrage: Strategies and Benefits Foreign exchange (FX) arbitrage is an investment strategy that aims to take advantage of …

Read Article

When it comes to non-qualified stock options (NQSOs), one of the most important factors to consider is the cost basis. The cost basis is the amount of money you initially paid for the options, and it is used to determine the taxable gain or loss when you exercise or sell the options.

Calculating the cost basis for NQSOs can be complex, as it involves several factors. One of the main factors is the grant price, which is the price at which you can purchase the stock when you exercise the options. Additionally, you need to take into account any costs, such as commissions or fees, associated with the purchase of the options.

Another factor to consider is any adjustments that may need to be made to the cost basis. These adjustments can include the spread, which is the difference between the grant price and the fair market value of the stock on the exercise date. It can also include any disqualifying dispositions, which occur when you sell the stock before meeting certain holding requirements.

In this comprehensive guide, we will walk you through the process of calculating the cost basis for NQSOs in detail. We will explain the different factors involved and provide examples to help you understand how it works. By the end of this guide, you will have a clear understanding of how to calculate the cost basis for your non-qualified stock options.

Non-Qualified Stock Options (NQSOs) are a type of stock option offered to employees as part of their compensation package. Unlike Incentive Stock Options (ISOs), NQSOs do not qualify for special tax treatment under the Internal Revenue Code.

When an employee is granted NQSOs, they have the right to buy a specific number of company shares at a predetermined price, known as the strike price or exercise price. This price is usually set at the current market value of the stock on the date of grant.

Employees can exercise their NQSOs at any time during a predetermined exercise period, which is typically several years after the grant date. Once the options are exercised, employees can either hold onto the shares or sell them in the open market.

One of the primary benefits of NQSOs is that they provide employees with the opportunity to participate in the company’s growth and success. If the stock price increases above the exercise price, employees can purchase the shares at a lower price and then sell them at the higher market price to make a profit.

However, it’s important to note that exercising NQSOs can also trigger tax obligations. The difference between the exercise price and the fair market value of the stock at the time of exercise is considered compensation income and is subject to ordinary income tax and potentially Medicare and Social Security taxes.

Read Also: Are taxes applicable on gifted stocks?

Overall, NQSOs can be a valuable form of compensation for employees, providing them with the potential for financial gain. Understanding the tax implications and calculating the cost basis is crucial for accurately determining the gain or loss upon the sale of the shares acquired through NQSOs.

Calculating the cost basis for non-qualified stock options can be a complex process, but by following these step-by-step instructions, you can ensure accuracy and compliance with tax regulations.

It’s important to note that if you sell the stock immediately after exercising your options, the cost basis will be equal to the exercise price plus any commissions or fees associated with the exercise. However, if you hold the stock for a period of time before selling, additional calculations may be required to account for any changes in the stock price or other factors.

Keep accurate records of your stock option transactions and consult a tax professional if you have any questions or need further assistance in calculating your cost basis for non-qualified stock options.

Read Also: Is Sensibull free or paid? A detailed comparison of pricing plans and features

Cost basis for non-qualified stock options is the price you paid to exercise the options plus any additional fees or commissions. It is used to calculate the profit or loss when you sell the stock.

If you exercised your non-qualified stock options in multiple transactions, you need to calculate the cost basis for each transaction separately. For each transaction, you take the cost of exercising the options plus any additional fees or commissions. You then sum up the cost basis for each transaction to get the total cost basis.

The cost basis of non-qualified stock options is not deductible on your taxes. However, it is used to calculate the profit or loss when you sell the stock, which may have tax implications.

If you sold the stock acquired from non-qualified stock options at a loss, you can use the loss to offset any capital gains you have and reduce your overall tax liability. If the loss exceeds your capital gains, you can use it to offset up to $3,000 of ordinary income and carry over any remaining loss to future years.

The alternative minimum tax (AMT) is a separate tax calculation that is often triggered when exercising non-qualified stock options. It can result in a higher tax liability compared to the regular tax calculation. When calculating the cost basis for non-qualified stock options, you need to consider the potential impact of the AMT and consult a tax advisor for guidance.

Calculating the cost basis for non-qualified stock options is important because it determines the amount of tax you owe when you exercise the options and sell the stock. The cost basis is used to calculate the capital gain or loss on the sale of the stock.

There are two methods to calculate the cost basis for non-qualified stock options: the multiple acquisition dates method and the single acquisition date method. The multiple acquisition dates method requires tracking each grant and exercise of the options separately, while the single acquisition date method treats all options as if they were acquired on the same date.

Understanding FX Arbitrage: Strategies and Benefits Foreign exchange (FX) arbitrage is an investment strategy that aims to take advantage of …

Read Article

Can you earn dividends on options? Options are a popular investment vehicle that allows traders to speculate on the price movement of an underlying …

Read Article

What is OHLC in mt4? When it comes to trading in financial markets, understanding OHLC is crucial. OHLC stands for Open, High, Low, and Close, and it …

Read Article

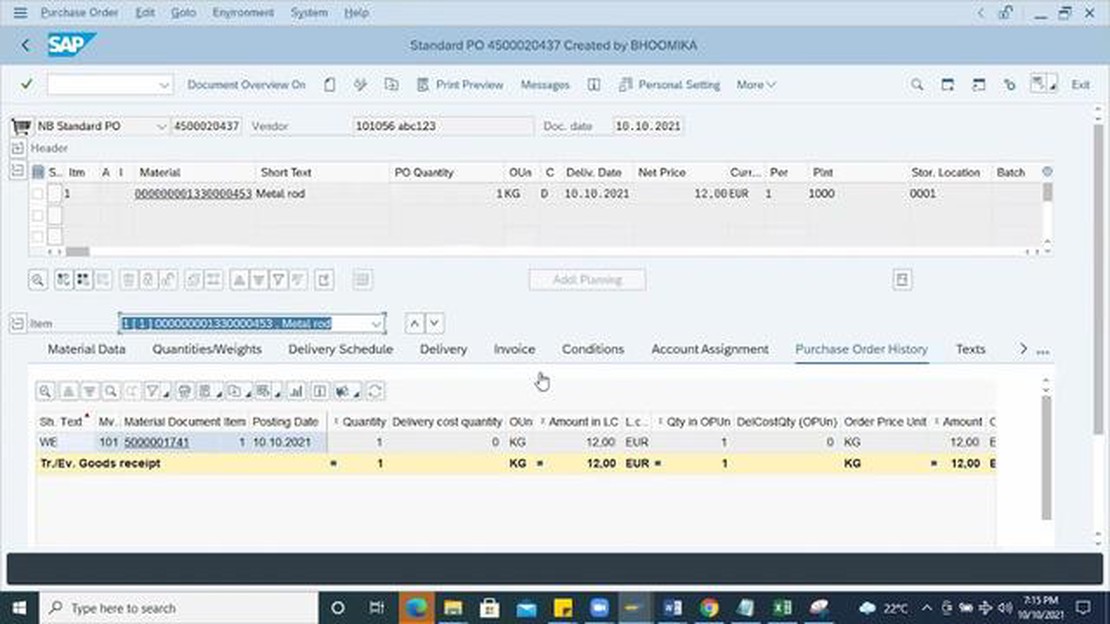

Understanding the Concept of Standard Price in SAP In SAP, the concept of standard price plays a crucial role in managing and controlling costs within …

Read Article

Profit and Loss of Option Strategy Explained Option strategies can be a powerful tool for investors to enhance their portfolio performance. However, …

Read Article

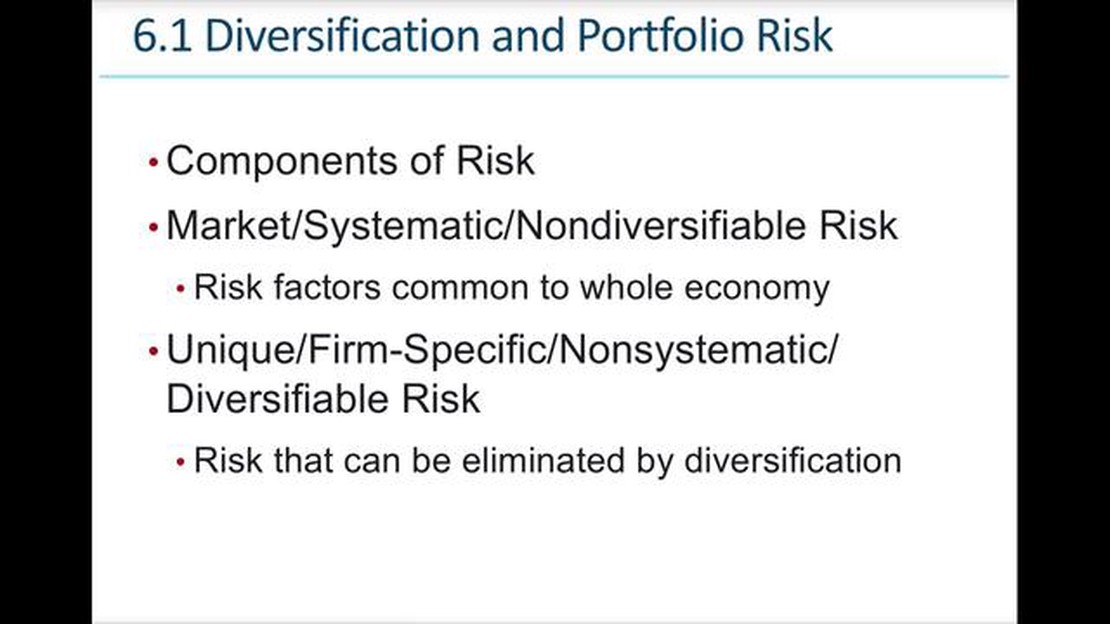

What are the 6 steps of diversification? Investing is a key activity for individuals and businesses looking to secure their financial future. However, …

Read Article