Is New Zealand a Free Trade Zone? Exploring New Zealand's Trade Policies and Agreements

Is New Zealand a Free Trade Country? New Zealand, a small island nation located in the southwestern Pacific Ocean, is often recognized for its …

Read Article

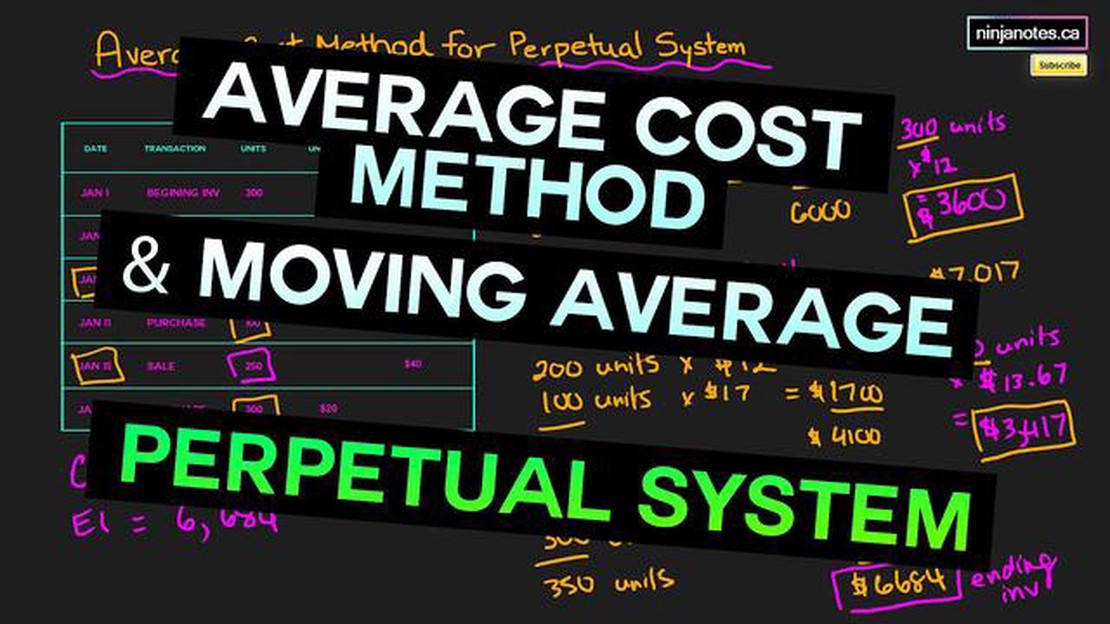

The moving average cost per unit is a financial metric used by businesses to determine the average cost of a unit of inventory over a specific period of time. It is an important tool for assessing the profitability of a company’s operations and managing inventory costs. By calculating the moving average cost per unit, businesses can get a better understanding of their cost structure and make informed decisions about pricing, production, and purchasing.

To calculate the moving average cost per unit, you need to know the total cost of the inventory and the total number of units in stock. This can include the cost of raw materials, labor, and other production expenses. By dividing the total cost by the total number of units, you can determine the average cost per unit.

For example, if a company has a total inventory cost of $10,000 and 1,000 units in stock, the moving average cost per unit would be $10,000 / 1,000 units = $10 per unit. As new inventory is purchased or sold, the moving average cost per unit will change accordingly.

The moving average cost per unit is particularly useful in industries where inventory costs can fluctuate significantly, such as retail or manufacturing. It allows businesses to adjust their pricing and production strategies to maintain profitability and stay competitive in the market. Additionally, it helps in assessing the impact of changes in the cost of raw materials or other production expenses.

In conclusion, the moving average cost per unit is a valuable financial metric that provides insights into a company’s inventory costs. By calculating this metric, businesses can make informed decisions about pricing, production, and purchasing to optimize profitability and stay competitive in their industry.

When managing inventory and calculating costs, understanding the moving average cost per unit can be essential. The moving average cost per unit refers to the average cost of each item in inventory based on the changes in the cost over time.

To calculate the moving average cost per unit, you need to track the costs associated with acquiring the items. This includes the cost of purchasing the items, any additional charges like transportation or handling fees, and any other expenses incurred in relation to the acquisition.

The calculation of the moving average cost per unit involves dividing the total cost of all the items in inventory by the total number of units. The result is the average cost per unit.

One benefit of using the moving average cost per unit method is that it smooths out the fluctuations in inventory costs. This can be particularly helpful when price changes are frequent or unpredictable. By calculating the average cost per unit, businesses can more accurately determine the cost of goods sold and the value of their inventory.

For example, let’s say a business purchases 100 items at $10 each. The total cost of the inventory is $1000. Later, the business purchases 50 more items at $12 each. To calculate the moving average cost per unit, you would add the total cost of the items purchased ($1000 + $600 = $1600) and divide it by the total number of units ($1600 ÷ 150 = $10.67). Therefore, the moving average cost per unit is $10.67.

Understanding the moving average cost per unit can help businesses make informed decisions about pricing, profitability, and managing their inventory. By accurately calculating and tracking the average cost per unit, businesses can avoid underpricing or overpricing their products and ensure that their financial records are accurate.

Read Also: Current Black Market Exchange Rate: How Much is $100 Worth?

Moving Average Cost Per Unit is a method used in accounting and finance to calculate the average cost of producing a unit of a product. It is commonly used in managing inventory costs and determining the cost of goods sold.

The moving average cost per unit is calculated by dividing the total cost of goods available for sale by the total number of units available for sale. This average cost is then used to determine the cost of each individual unit sold or produced.

Read Also: Pros and Cons of Offering Stock Options to Employees as Incentive Compensation

The moving average cost per unit is especially useful in situations where the cost of acquiring inventory fluctuates over time. By taking into account the average cost over a period of time, this method helps to smooth out the impact of price changes.

For example, let’s say a company acquires 100 units of a product at various costs over a month: 50 units at $10 each and 50 units at $12 each. The total cost of goods available would be $1,100 ($500 from the first batch and $600 from the second batch), and the total number of units available would be 100.

To determine the moving average cost per unit, divide the total cost of goods available by the total number of units available: $1,100 divided by 100 units equals $11 per unit.

This moving average cost per unit of $11 can then be used to calculate the cost of each unit sold or produced, providing a more accurate representation of cost in a dynamic pricing environment.

In conclusion, the moving average cost per unit is a valuable tool for businesses to manage inventory costs and determine accurate pricing. By taking into account fluctuating costs over a period of time, this method provides a more realistic representation of the average cost per unit.

The purpose of calculating the moving average cost per unit is to determine the average cost of each unit of production over a specific period of time. This can be useful for budgeting, pricing decisions, and inventory valuation.

The moving average cost per unit is calculated by dividing the total cost of production by the total number of units produced over a specific period of time. This gives the average cost for each unit produced during that time period.

Yes, the moving average cost per unit can change over time. As new units are produced and included in the calculation, the average cost per unit may increase or decrease depending on the cost of production for those units.

One advantage of using the moving average cost per unit method is that it smooths out fluctuations in the cost of production. This can be helpful for businesses that experience frequent changes in production costs. Additionally, it provides a more accurate representation of the average cost per unit compared to other costing methods.

While the moving average cost per unit method is useful in many situations, it may not be suitable for all businesses. It assumes that the cost of production is evenly spread across all units produced, which may not always be the case. Additionally, it may not be appropriate for businesses with significant variations in production costs over time.

Is New Zealand a Free Trade Country? New Zealand, a small island nation located in the southwestern Pacific Ocean, is often recognized for its …

Read Article

Hours of F& F& is a popular establishment that offers a wide range of services and products. From delicious meals to high-quality goods, F& has …

Read Article

Is Forex Robot Real? Forex trading has become increasingly popular in recent years, with more and more people looking to make profits in the …

Read Article

Stock-Based Compensation and Deferred Tax Assets: An Exploratory Analysis Stock-based compensation is a form of remuneration that companies offer to …

Read Article

How much does 1000Pip builder cost? If you are a forex trader looking for reliable and accurate trading signals, you may have come across 1000Pip …

Read Article

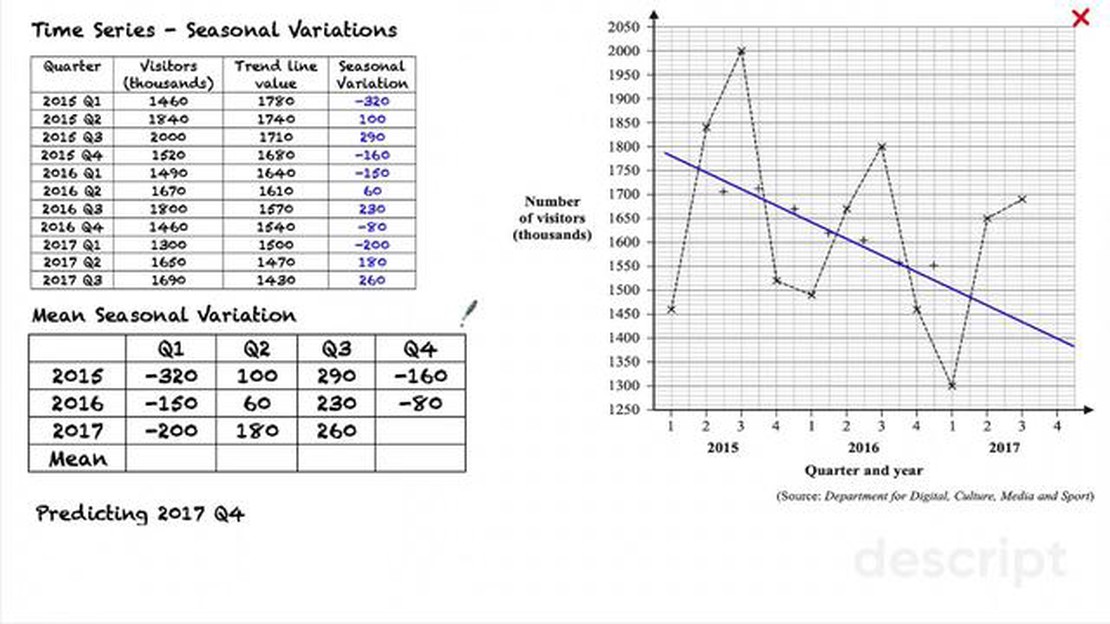

Formula for the Seasonal Component The seasonal component is an important factor to consider when analyzing time series data. It represents the …

Read Article