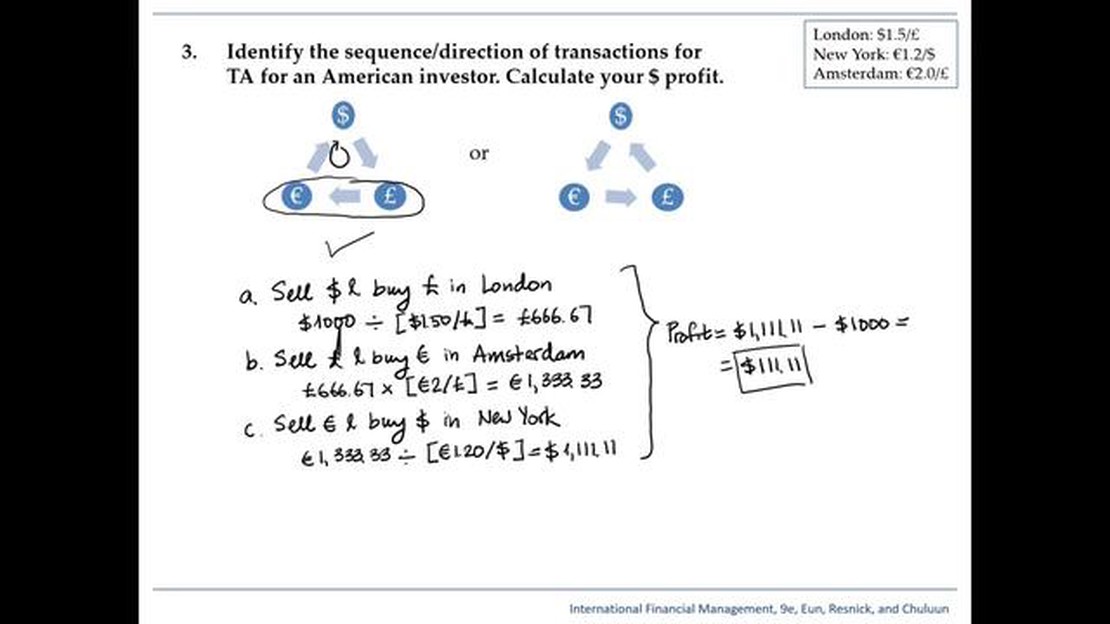

Triangular arbitrage is a popular strategy in the world of finance and investing. It involves taking advantage of pricing discrepancies in different currency pairs to make a profit. This strategy is based on the principle of exploiting the exchange rate differences between three currencies.

Table Of Contents

To understand how triangular arbitrage works, let’s consider an example. Suppose we have three currency pairs: USD/GBP, GBP/EUR, and EUR/USD. If we convert 1 USD into GBP and then into EUR, we might end up with more or less than 1 EUR. By comparing the final amount of EUR obtained by using these two routes, we can identify an opportunity for triangular arbitrage.

Let’s say we convert 1 USD into GBP, and then 1 GBP into EUR. If we end up with 1.1 EUR, but if we directly convert 1 USD into EUR, we get 1.05 EUR, then we can take advantage of this difference. We can sell our 1.05 EUR for 1 GBP and then convert that 1 GBP back into USD. By doing so, we would end up with more USD than we originally started with.

Triangular arbitrage can be a complex and time-sensitive strategy that requires quick decision-making and execution. It requires advanced knowledge of currency markets, exchange rates, and market trends. Traders and investors who engage in triangular arbitrage are constantly monitoring currency pairs and executing trades to capitalize on price discrepancies.

In conclusion, triangular arbitrage is a strategy that allows traders to exploit pricing discrepancies in currency pairs to make a profit. It involves taking advantage of exchange rate differences between three currencies. However, it is important to note that triangular arbitrage requires extensive experience and understanding of the forex market to be successful.

What is Triangular Arbitrage?

Triangular arbitrage is a popular trading strategy that takes advantage of discrepancies in exchange rates among three different currencies. The concept behind triangular arbitrage is based on the idea that cross-exchange rates should reflect the real value of the currencies involved. However, due to various factors such as market inefficiencies or time delays, exchange rates may deviate from their equilibrium values, creating opportunities for profit.

In triangular arbitrage, traders exploit these temporary exchange rate imbalances by executing a series of successive trades. The process begins by converting a base currency into a second currency, then into a third currency, and finally back into the base currency. By carefully calculating the exchange rates and ensuring that the resulting profit is positive, traders can generate risk-free profits.

For example, suppose the exchange rates are as follows: 1 USD = 0.85 EUR, 1 EUR = 120 JPY, and 1 USD = 110 JPY. In this scenario, a trader could initiate a triangular arbitrage strategy by converting 1 USD to EUR, then to JPY, and finally back to USD. If done correctly, the trader would end up with more USD than initially invested, earning a profit in the process.

It is important to note that triangular arbitrage opportunities are usually short-lived and may disappear quickly as market participants take advantage of them. Additionally, executing triangular arbitrage effectively requires advanced technical analysis skills and access to fast and reliable trading platforms.

In conclusion, triangular arbitrage is a trading strategy that aims to profit from exchange rate discrepancies among three different currencies. By taking advantage of temporary imbalances, traders can generate risk-free profits using carefully calculated trades. However, it is crucial to understand the complexities and risks involved before attempting this strategy.

Definition and Explanation

Triangular arbitrage is a financial strategy that involves taking advantage of differences in exchange rates between three currencies. It is based on the premise that the exchange rates between three currencies should have a certain relationship, known as the triangular arbitrage opportunity.

The strategy works by identifying a discrepancy in the exchange rates and executing a series of trades to profit from it. To understand how it works, let’s consider an example:

Suppose we have three currencies: USD, GBP, and EUR.

Let’s assume the exchange rates are as follows: 1 USD = 0.9 EUR and 1 GBP = 1.2 USD.

Based on these exchange rates, we can calculate the cross rate between EUR and GBP: 1 EUR = 1 / (1 USD / 0.9 EUR) * (1 GBP / 1.2 USD) = 0.75 GBP.

In this example, the calculated cross rate between EUR and GBP is 0.75 GBP. However, if the actual market rate for 1 EUR is higher than 0.75 GBP, there is a potential opportunity for triangular arbitrage.

Here’s how the triangular arbitrage strategy would work:

Buy EUR with USD: Convert 1 USD to 0.9 EUR.

Sell EUR for GBP: Convert 0.9 EUR to 0.9 * 0.75 GBP = 0.675 GBP.

Sell GBP for USD: Convert 0.675 GBP to 0.675 * 1.2 USD = 0.81 USD.

In this scenario, we started with 1 USD and ended up with 0.81 USD, resulting in a profit of 0.81 - 1 = -0.19 USD. This negative profit indicates that there is no triangular arbitrage opportunity in this case.

Overall, triangular arbitrage can be a complex strategy that requires a deep understanding of exchange rates and market dynamics. It is often used by professional traders and financial institutions to exploit temporary imbalances in the currency markets and generate profits.

Example of Triangular Arbitrage

Let’s consider an example to better understand how triangular arbitrage works.

Suppose there are three currencies: the US dollar (USD), the euro (EUR), and the Japanese yen (JPY). The exchange rates are as follows:

Using these exchange rates, we can calculate the implied exchange rate between USD and JPY by going through the EUR currency.

According to the exchange rates above, we can convert 1 USD to EUR and then to JPY, or we can convert 1 JPY to EUR and then to USD.

Using path 1, we convert 1 USD to EUR and get 1.25 EUR. Then, we convert 1.25 EUR to JPY and get 137.5 JPY.

Using path 2, we convert 1 JPY to EUR and get 0.0091 EUR. Then, we convert 0.0091 EUR to USD and get 0.0073 USD.

As we can see, using these exchange rates, path 1 gives us 137.5 JPY when converting 1 USD, while path 2 gives us 0.0073 USD when converting 1 JPY. This implies that 1 USD is equal to 137.5 JPY, which contradicts the actual exchange rate of 1 USD to 108 JPY.

This discrepancy allows arbitrage opportunities. A trader can profit from triangular arbitrage by converting USD to JPY through EUR using path 1, and then converting JPY back to USD using path 2. Through this process, the trader can make a profit of 0.0027 USD per JPY.

This example demonstrates how triangular arbitrage works in the foreign exchange market, where market inefficiencies in exchange rates can be exploited for profit.

FAQ:

What is triangular arbitrage?

Triangular arbitrage is a financial strategy that involves exploiting price differences between three currencies to make a profit.

How does triangular arbitrage work?

Triangular arbitrage involves three currency pairs. The trader takes advantage of inconsistencies in exchange rates between these pairs to make a profit by executing a series of trades.

Can you give an example of triangular arbitrage?

Sure! Let’s say we have three currency pairs: USD/EUR, EUR/GBP, and GBP/USD. If there is a discrepancy in the exchange rates, such as USD/EUR = 0.8, EUR/GBP = 0.6, and GBP/USD = 1.2, the trader can execute a series of trades to exploit this discrepancy and make a profit.

What are the risks involved in triangular arbitrage?

There are several risks involved in triangular arbitrage, including execution risk, market risk, and liquidity risk. Additionally, the strategy requires fast execution and may be more difficult to implement in volatile market conditions.

Understanding the Concept of Magic Number in EA Forex Trading Electronic trading has revolutionized the foreign exchange market, making it faster and …

Current exchange rate: 1 USD to LKR Exchange rates play a crucial role in international trade and finance. They determine the value of one currency in …