What is a Forex expert: Understanding the role and skills of a financial trading pro

What is a Forex expert? Foreign exchange, or Forex, trading is a fast-paced and highly volatile market where individuals can trade currencies from …

Read Article

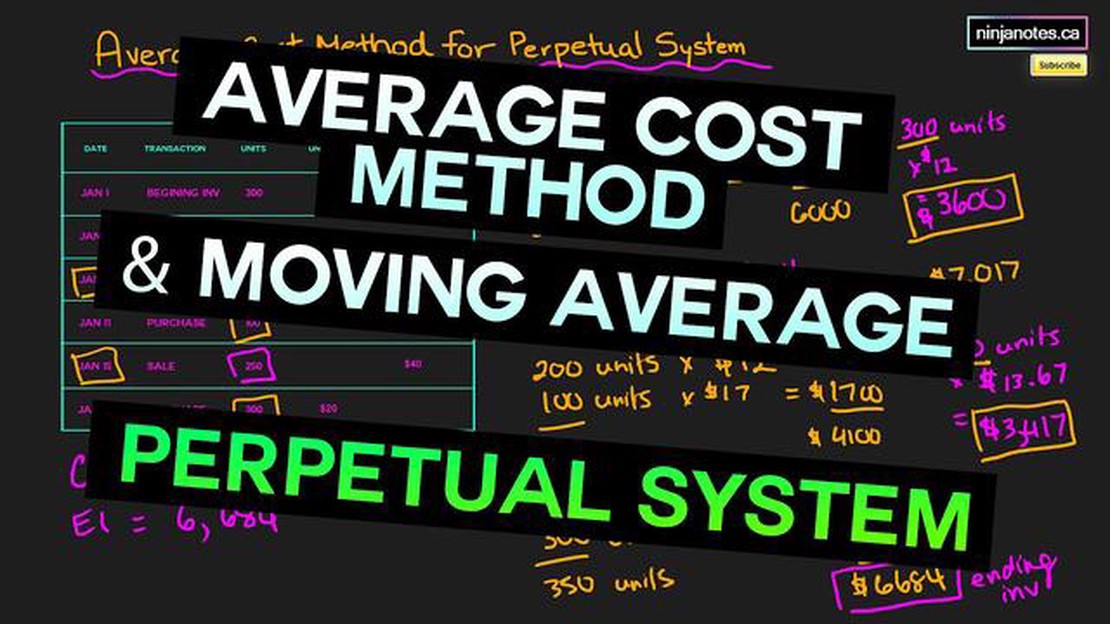

The moving average method is a widely used technique in material management that helps to forecast and manage inventory levels. It is based on the principle of determining the average cost of goods over a specific period of time, which is then used to calculate the value of inventory.

In material management, the moving average method is particularly useful in industries where the cost of raw materials fluctuates frequently. By taking into account the most recent prices paid for materials, this method provides a more accurate and up-to-date estimate of the value of inventory.

One of the key advantages of the moving average method is its simplicity and ease of use. It does not require complex calculations or extensive data analysis, making it accessible to businesses of all sizes. Additionally, this method can be easily incorporated into existing inventory management systems, allowing for seamless integration and efficient tracking of inventory levels.

Using the moving average method in material management can significantly improve inventory accuracy and enable businesses to make more informed and strategic decisions regarding procurement and production.

In conclusion, the moving average method is a valuable tool in material management that helps businesses effectively manage their inventory levels and forecast future demand. By accounting for fluctuations in material costs, this method allows for more accurate valuation of inventory and enhances overall operational efficiency.

The moving average method is a technique used in material management to calculate the average cost of a product over a specified period of time. It is based on the principle of averaging the unit cost of the product by taking into account the cost of both older and newer inventory.

The moving average method is particularly useful in industries where the cost of raw materials or finished products fluctuates frequently. By averaging the cost over time, it allows businesses to manage their inventory and pricing strategies more effectively.

To calculate the moving average cost, you need to have data on the quantity and cost of products purchased at different times. The average cost is calculated by dividing the total cost of the inventory by the total quantity of products in stock.

Here’s an example to illustrate how the moving average method works:

| Date | Quantity | Cost | Total Cost | Total Quantity | Moving Average Cost |

|---|---|---|---|---|---|

| Jan 1 | 100 | $10 | $1000 | 100 | $10 |

| Feb 1 | 50 | $12 | $600 | 150 | $10.50 |

| Mar 1 | 200 | $8 | $1600 | 350 | $9.14 |

In this example, the inventory cost for January is $1000 (100 units x $10 per unit). In February, 50 units are purchased at a cost of $12 per unit, resulting in a total cost of $600. The moving average cost for February is calculated as the total cost ($1600) divided by the total quantity (150 units), which equals $10.50 per unit. Similarly, the moving average cost for March is calculated as $9.14 per unit.

By using the moving average method, businesses can make more informed decisions regarding pricing, inventory management, and profitability. It provides a more accurate reflection of the true cost of products, which can help in setting competitive prices and optimizing profit margins.

The moving average method is a commonly used technique in material management for forecasting future demand. It is based on the principle that past demand can be used to predict future demand.

The method calculates an average of the demand over a certain period of time and uses this average to forecast future demand. It is called “moving” average because as new data becomes available, the average is updated by removing the oldest data point and adding the newest data point.

This method is particularly useful for smoothing out fluctuations in demand that may occur due to seasonality, promotions, or other factors. By taking into account the historical data, the moving average method can provide a more accurate forecast than simply using the most recent demand data.

Read Also: How Accurate is an SKS at 100 Yards? Discover the Rifle's Precision.

There are different variations of the moving average method, such as the simple moving average and the weighted moving average. The simple moving average gives equal weight to all data points, while the weighted moving average assigns different weights to each data point based on their significance.

In conclusion, understanding the principle of the moving average method is essential for effective material management. By utilizing this technique, businesses can make more informed decisions about inventory levels, production planning, and overall supply chain management.

Read Also: What is the value of a 1000 Chilean peso bill?

The moving average method is a commonly used method in material management that has both advantages and disadvantages. Understanding these can help companies determine if this method is appropriate for their inventory control needs.

One of the main advantages of the moving average method is its simplicity. This method calculates the average cost of inventory by considering the prices of goods over a certain period of time. This makes it easy to understand and implement, especially for companies that do not have sophisticated inventory management systems.

Another advantage of the moving average method is its ability to smooth out price fluctuations. By using an average cost that is based on multiple periods, this method can help companies avoid sudden spikes or drops in inventory costs. This can be particularly useful in industries where price fluctuations are common and can impact profitability.

However, there are also some disadvantages to using the moving average method. One significant disadvantage is that it may not accurately reflect the current market value of inventory. As this method considers historical costs, it may not capture changes in prices that have occurred since the inventory was purchased. This can result in overvalued or undervalued inventory, leading to inaccurate financial statements.

Furthermore, the moving average method can be time-consuming to calculate and update. With each new purchase or sale of inventory, the average cost needs to be recalculated. This can be burdensome for companies with high transaction volumes or complex inventory systems, requiring significant time and resources.

In conclusion, the moving average method has both advantages and disadvantages. It offers simplicity and helps smooth out price fluctuations, but it may not accurately reflect market values and can be time-consuming to maintain. Therefore, companies should carefully consider their specific inventory management needs and evaluate if the moving average method is the most suitable approach for their business.

The moving average method is a way to calculate the average cost of inventory items by taking into account the cost of the items purchased over a certain period of time.

The moving average cost is calculated by dividing the total cost of the inventory items by the total number of items in stock.

The moving average method is important in material management as it helps in determining the cost of inventory items, which is crucial for budgeting, pricing decisions, and evaluating the profitability of products.

The advantages of using the moving average method include that it provides a more accurate representation of the true cost of inventory items, helps in stabilizing costs over time, and provides an efficient way to calculate the cost of goods sold.

Yes, the moving average method can be used in all types of businesses that deal with inventory management, regardless of the industry or size of the organization.

The Moving Average method is a forecasting technique used in material management to analyze the average cost of inventory over a specific period of time.

The Moving Average method calculates the average cost of inventory by considering the prices of goods received over a specific period of time. This average cost is then used to value the inventory.

What is a Forex expert? Foreign exchange, or Forex, trading is a fast-paced and highly volatile market where individuals can trade currencies from …

Read Article

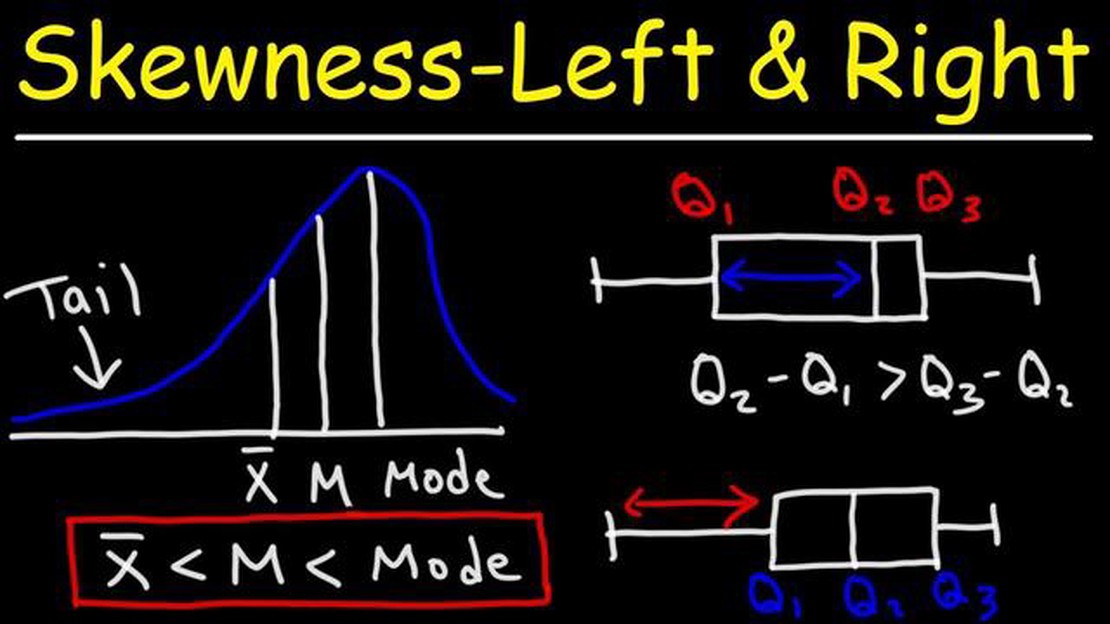

Example of a Positive Skew in Data Distribution Skewness is a statistical concept that measures the asymmetry of a distribution. When a distribution …

Read Article

Important Questions to Ask Before Accepting Options as Compensation When considering a job offer, it’s important to carefully evaluate all aspects of …

Read Article

Is there a monthly fee for forex? Trading on the foreign exchange market, also known as forex, can be a lucrative endeavor. However, before you dive …

Read Article

Understanding Reference Exchange Rates Maintaining stable exchange rates is crucial for the global economy, and reference exchange rates play a vital …

Read Article

Who is a Pro Forex Trader? If you’ve ever wondered what it takes to become a professional forex trader, you’re in the right place. Forex trading is …

Read Article