Discover the Formula for the Price Action Indicator

What is the formula for the price action indicator? The price action indicator is a popular tool used by traders and investors to analyze market …

Read Article

Nonqualified stock options (NQSOs) are an increasingly popular form of compensation offered by many companies to their employees. These options give employees the right to buy company stock at a predetermined price, typically lower than the current market price, at a future date. While NQSOs can be a valuable tool for attracting and retaining talent, it’s important for both employers and employees to understand the tax implications associated with these options.

One key consideration is the 409A valuation, a provision added to the Internal Revenue Code in 2004. The purpose of this provision is to ensure that employees receive fair market value when exercising their NQSOs. To comply with 409A, companies must obtain a valuation of their common stock from an independent third-party appraiser, who will determine the fair market value of the stock at the time the option is granted.

The 409A valuation is crucial because it establishes the strike price, or the price at which the employee can purchase the stock. If the strike price is set below the fair market value determined by the 409A valuation, it may trigger significant tax consequences for the employee. The difference between the strike price and the fair market value is considered taxable income and is subject to ordinary income and payroll taxes.

It’s important for employers to carefully consider the implications of 409A when designing their NQSO programs. By ensuring that the strike price is set at or above the fair market value determined by a 409A valuation, employers can minimize the tax burden for their employees. In addition, companies should communicate the tax implications of NQSOs to their employees, providing them with the information they need to make informed decisions about exercising their options.

409A is a section of the Internal Revenue Code that applies to nonqualified deferred compensation plans. This section has significant implications for companies that offer nonqualified stock options to their employees. It was introduced to prevent executives from deferring their income and taxation, which can occur with nonqualified deferred compensation plans.

When it comes to nonqualified stock options, 409A imposes strict rules on the valuation of these options. The fair market value of the stock underlying the options must be determined in a reasonable manner. This is crucial because the exercise price of the options should not be less than the fair market value of the stock on the date the options are granted.

To comply with 409A, companies must use a reasonable valuation method, such as an independent appraisal or the safe harbor provisions outlined in the section. Failure to comply with these rules can result in severe penalties, including inclusion of the option’s full value as ordinary income for the employee, plus an additional 20% of the amount included in income.

In addition to valuation, 409A also imposes restrictions on the timing of the exercise of nonqualified stock options. Under the regulations, the options must have a specified payment date or meet one of the short-term deferral exemptions. This means that employees cannot exercise their options whenever they please; there must be a predetermined date or event for the options to be exercised.

It is important for companies to have a thorough understanding of the 409A implications when offering nonqualified stock options to their employees. Compliance with these rules is vital to avoid significant tax consequences and penalties.

Read Also: Which Indicator Works Best with Bollinger Bands? Discover the Top Choices!

In conclusion, 409A has important implications for companies offering nonqualified stock options. The valuation of the options must be done in a reasonable manner, and there are restrictions on the exercise timing. To avoid penalties and tax consequences, it is crucial for companies to comply with these rules.

Nonqualified stock options (NQSOs) are a type of stock option that is not eligible for special tax treatment under Section 409A of the Internal Revenue Code. They are often used by companies to provide employees with the opportunity to purchase company stock at a predetermined price, known as the exercise price.

Read Also: Understanding the cost basis of exercised stock options: A comprehensive guide

There are several key considerations to keep in mind when it comes to NQSOs:

| Consideration | Explanation |

|---|---|

| Vesting Schedule | NQSOs may have a vesting schedule, which outlines when employees can exercise their options. This can be based on time (e.g., a certain percentage of options vesting each year) or performance milestones. |

| Exercise Price | The exercise price is the price at which employees can purchase the stock. It is typically set at or above the fair market value of the stock on the grant date. |

| Expiration Date | NQSOs have an expiration date, which is the deadline for employees to exercise their options. If the options are not exercised by this date, they will expire and become worthless. |

| Tax Implications | When employees exercise their NQSOs, they may be subject to ordinary income tax on the difference between the fair market value of the stock and the exercise price. It is important to understand the tax implications and consult with a tax advisor. |

| Alternative Minimum Tax (AMT) | Employees who exercise their NQSOs may also be subject to the alternative minimum tax. This is a separate tax calculation that ensures individuals with high deductions or credits still pay a minimum amount of tax. |

| Transferability | In general, NQSOs are not transferable and can only be exercised by the original option holder. However, there may be exceptions for transfers to family members or as part of certain estate planning strategies. |

| Risk of Forfeiture | Employees should be aware that NQSOs may be subject to a risk of forfeiture, meaning they could lose their options if they leave the company before the options have vested. |

Understanding these key considerations is essential for both employers and employees when it comes to nonqualified stock options. It is important to carefully review plan documents and consult with professionals to ensure compliance with tax regulations and make informed decisions.

Nonqualified stock options are a type of stock option that does not qualify for special tax treatment under the Internal Revenue Code. They are typically offered to employees as a form of compensation or incentive.

Section 409A of the Internal Revenue Code imposes certain requirements and restrictions on nonqualified deferred compensation plans, including nonqualified stock options. Failure to comply with these requirements can result in immediate taxation and penalties for both the employee and the employer.

Under 409A, nonqualified stock options must be valued at fair market value at the time of grant. This valuation needs to be done in good faith and may require the use of an independent appraiser. The valuation should take into account various factors such as the company’s financial condition, the market value of its stock, and any restrictions on transferability.

Nonqualified stock options are generally subject to ordinary income tax when they are exercised. Additionally, Section 409A imposes additional taxes on any amount that exceeds the fair market value of the stock option at the time of exercise. These additional taxes can be significant, so it is important for employees to be aware of their potential tax liability.

What is the formula for the price action indicator? The price action indicator is a popular tool used by traders and investors to analyze market …

Read Article

Is Options Alpha Free? Options Alpha has become a popular resource for traders and investors looking to enhance their knowledge and skills in options …

Read Article

What is the daily chart strategy in forex? Forex trading is a complex and highly volatile market, with numerous strategies available to traders. One …

Read Article

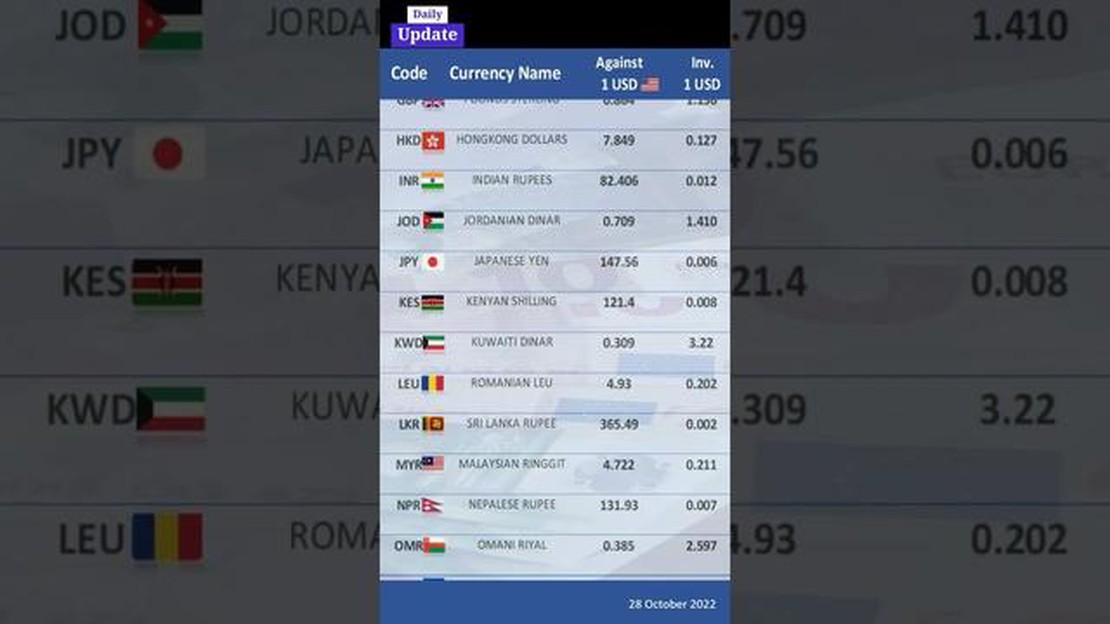

Current exchange rate of $1 USD When it comes to currency exchange rates, the value of the US dollar is a topic of interest for many people around the …

Read Article

Maybank International Transaction Fees: How Much Do They Charge? Sending money abroad can be a convenient way to support loved ones or conduct …

Read Article

Buying Stocks with Call Options: A Comprehensive Guide Buying stocks is a popular way to invest and potentially grow your wealth. However, if you want …

Read Article