What is an IV option? - An in-depth explanation and analysis

Understanding IV Options: A Comprehensive Guide IV options, also known as implied volatility options, are a type of financial derivative that allow …

Read Article

In the world of global finance, foreign exchange (FX) and currency options are two essential tools that provide individuals and businesses with the ability to manage and mitigate risks associated with international trade. These financial instruments have been around for decades, but it wasn’t until the late 20th century that they truly gained widespread popularity and recognition.

The year 1998 holds a significant place in the history of FX and currency options. It marked a turning point and reshaped the way these instruments were understood and utilized. This comprehensive guide aims to provide a thorough understanding of the 1998 FX and currency option crisis, its causes, consequences, and the lessons learned from it.

At the heart of the 1998 crisis was the collapse of Long-Term Capital Management (LTCM), a hedge fund that heavily relied on complex trading strategies involving foreign exchange and currency options. LTCM’s downfall sent shockwaves throughout the financial industry, leading to a global liquidity crisis and a profound reassessment of risk management practices.

The 1998 FX and Currency Option refers to a financial instrument that was widely used during the late 1990s. It was designed to provide investors with the ability to hedge against foreign exchange and currency risks. This instrument allowed investors to establish predetermined exchange rates for buying or selling currencies in the future.

The 1998 FX and Currency Option was a derivative instrument, meaning its value was derived from an underlying asset or currency. It provided investors with a way to speculate on the future movements of foreign exchange rates without having to actually own the underlying asset. This made it attractive for both hedging and trading purposes.

One of the key features of the 1998 FX and Currency Option was its flexibility. Investors could choose to enter into either a call option or a put option, depending on whether they wanted to buy or sell a currency at a specified exchange rate. Additionally, investors could choose the expiration date of the option, allowing them to tailor the instrument to their specific needs.

The 1998 FX and Currency Option played a significant role in the global financial markets during the late 1990s, especially during the Asian financial crisis. It allowed investors to hedge their exposure to foreign exchange risks and protected them from unexpected movements in exchange rates. However, it also exposed investors to the risk of options expiry and the potential loss of the premium paid for the option.

Read Also: Understanding Discounted Options: A Comprehensive Guide

Overall, the 1998 FX and Currency Option provided investors with a valuable tool for managing and speculating on foreign exchange risks. It allowed them to establish predetermined exchange rates and protect themselves from sudden fluctuations in currency prices. However, it also carried its own set of risks and required careful consideration and understanding before its use.

The 1998 FX and Currency Option is a financial contract that provides the right but not the obligation to buy or sell a specified amount of currency at a predetermined exchange rate on a specific date in the future. This instrument was developed as a way for businesses and investors to manage the risks associated with fluctuations in foreign currency exchange rates.

Here are some key features of the 1998 FX and Currency Option:

1. Exchange rate: The option contract specifies the exchange rate at which the currency will be bought or sold. This rate is determined at the time the contract is entered into and remains fixed until the expiration date of the option.

2. Option premium: The buyer of the option pays a premium to the seller in exchange for the right to buy or sell the currency at the specified exchange rate. The premium is determined by various factors, such as the current exchange rate, volatility, and time to expiration.

3. Expiration date: The option contract has a predetermined expiration date, which is the last day that the option can be exercised. After this date, the option becomes invalid and the right to buy or sell the currency at the predetermined exchange rate is lost.

4. Exercise style: The 1998 FX and Currency Option typically follows a European exercise style, which means that the option can only be exercised on the expiration date.

5. Hedging and speculation: The 1998 FX and Currency Option can be used for both hedging and speculation purposes. Businesses can use these options to manage their currency risks and protect against adverse exchange rate movements. On the other hand, speculators can use these options to profit from anticipated currency movements.

Read Also: Should You Let Options Expire? Understanding the Pros and Cons

6. Customization: The 1998 FX and Currency Option can be customized to meet the specific needs of the buyer and seller. This includes choosing the currency pair, the contract size, the exercise price, and the expiration date.

Overall, the 1998 FX and Currency Option provides a flexible and efficient way to manage currency risks and take advantage of currency market opportunities. It is an important tool for businesses and investors operating in the global marketplace.

The 1998 FX and Currency Option had a significant impact on global financial markets, particularly in relation to the currencies of emerging markets. It provided a comprehensive framework for the trading and settlement of foreign exchange and currency options, which were becoming increasingly popular financial instruments at the time. The guide helped establish standard practices, regulations, and risk management strategies for participants in these markets.

The 1998 FX and Currency Option guide was published by the International Foreign Exchange Committee (IFEC), an organization composed of central banks and private sector participants in the foreign exchange market. The IFEC is responsible for promoting best practices, fostering market development, and addressing issues related to foreign exchange and currency trading.

The 1998 FX and Currency Option guide encompasses a wide range of topics related to foreign exchange and currency option trading. Some of its key features include guidelines for trading and settlement procedures, best execution practices, risk management strategies, and regulatory considerations. The guide also addresses topics such as documentation requirements, counterparty credit risk, and market integrity.

The 1998 FX and Currency Option guide played a crucial role in shaping the development of currency markets in emerging economies. By providing a comprehensive framework for trading and settlement, the guide increased transparency, reduced transaction costs, and improved risk management practices. It helped attract foreign investors to emerging markets, leading to increased liquidity and stability in their currency markets.

Understanding IV Options: A Comprehensive Guide IV options, also known as implied volatility options, are a type of financial derivative that allow …

Read Article

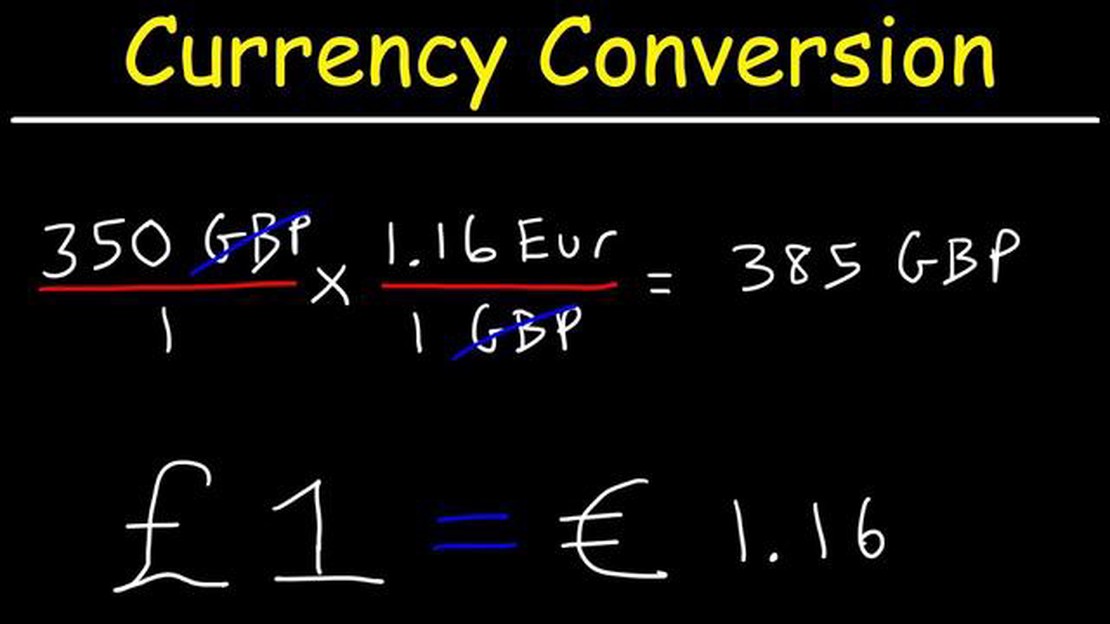

1 USD to BGN: Current Exchange Rate and Conversion Do you need to know the current exchange rate of the US dollar (USD) to the Bulgarian lev (BGN)? …

Read Article

What is chicken stock stock? When it comes to cooking, chicken stock is an essential ingredient that can elevate the flavor of any dish. But what …

Read Article

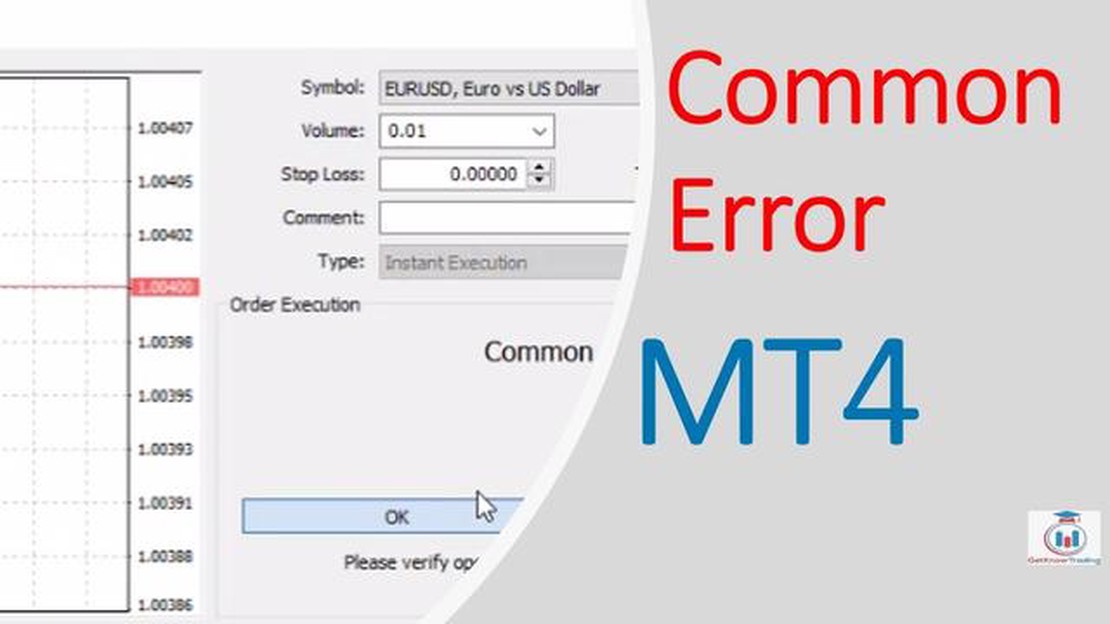

Understanding Error Code 138 on MT4: Common Causes and Solutions Error code 138, also known as “requote” error, is a common issue faced by traders …

Read Article

First 4 digits of an IBAN explained An International Bank Account Number (IBAN) is a standardized numbering system used to identify bank accounts …

Read Article

Understanding the 100000 Contract Size in Forex Trading In the world of Forex trading, it’s essential to have a clear understanding of contract sizes. …

Read Article