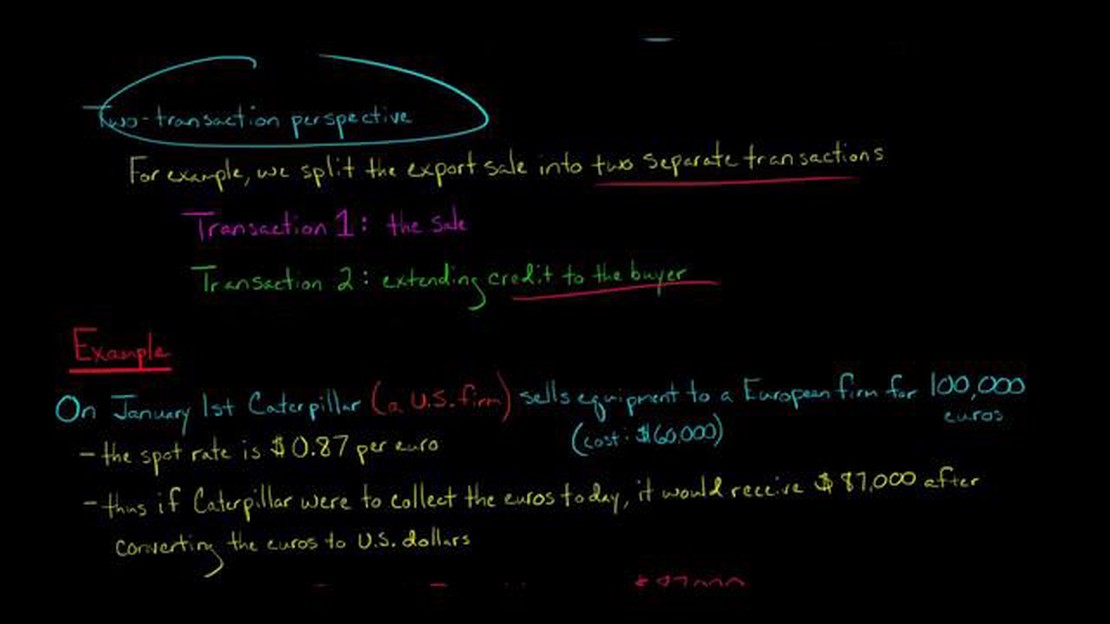

Understanding the Concept of Foreign Exchange Fluctuation Account

Understanding the Foreign Exchange Fluctuation Account When conducting business internationally, companies often face the challenge of dealing with …

Read Article

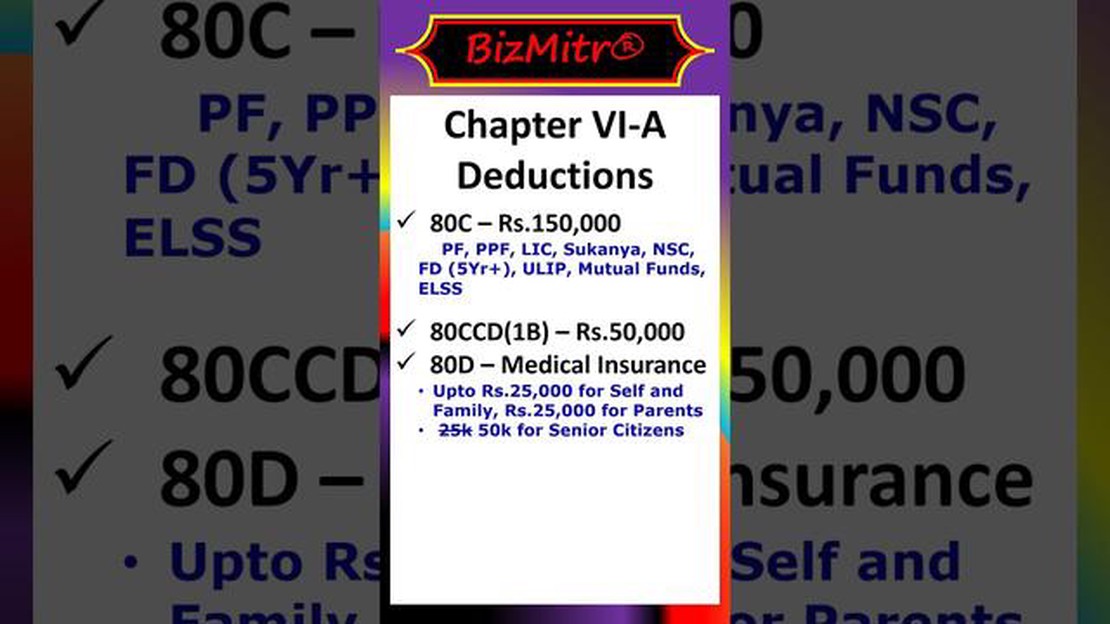

In the world of tax deductions, the 110 1-D deduction stands out as one of the most valuable and widely used. However, many taxpayers struggle to understand the intricacies and requirements of this deduction. In this article, we will dive deep into the details of the 110 1-D deduction, explaining its purpose, eligibility criteria, and how it can benefit taxpayers.

The 110 1-D deduction is designed to provide tax relief to businesses and individuals who invest in certain qualified assets. The deduction allows taxpayers to deduct 110% of the cost of qualified assets from their taxable income, reducing their overall tax liability. This can result in significant savings for eligible taxpayers, making it a highly sought-after deduction.

Eligibility for the 110 1-D deduction is determined by several factors. First and foremost, the asset must be classified as a qualified asset, which typically includes tangible personal property used in the taxpayer’s trade or business. Additionally, the asset must meet the criteria set forth by the tax code, such as being purchased within a certain time frame and being used for a specific purpose.

It’s important to note that the 110 1-D deduction is subject to certain limitations and phase-outs. Taxpayers should consult with a tax professional or refer to the IRS guidelines to ensure they meet all requirements and maximize their deduction.

Overall, the 110 1-D deduction provides a valuable opportunity for taxpayers to reduce their tax liability and increase their bottom line. By understanding the intricacies and requirements of this deduction, taxpayers can make informed decisions about their investments and take full advantage of the tax benefits it provides.

The 110 1-D Deduction is a tax provision that allows businesses to deduct the costs of qualifying assets in the year they are placed in service, rather than depreciating them over several years. This deduction is a valuable tool for businesses, particularly in industries that rely heavily on technology and equipment.

To qualify for the 110 1-D Deduction, the assets must meet certain criteria. They must be tangible personal property, meaning they can be touched, seen, and moved. Additionally, the assets must have a useful life of one year or more and be used for business purposes.

By taking advantage of this deduction, businesses can accelerate the depreciation of their assets and reduce their taxable income. This can result in significant tax savings, allowing businesses to reinvest in growth and innovation.

It’s important to note that the 110 1-D Deduction is different from the Section 179 deduction. While both provisions allow businesses to deduct the cost of qualifying assets, the 110 1-D Deduction has fewer restrictions and can apply to a wider range of assets.

In conclusion, the 110 1-D Deduction is a powerful tax planning tool that can benefit businesses by allowing them to deduct the cost of qualifying assets in the year they are placed in service. Understanding the criteria for qualifying assets is key to maximizing the benefits of this deduction and reducing taxable income.

The 110 1-D Deduction is a tax benefit that allows businesses to deduct the costs associated with qualifying research and development activities. It is named after section 110 of the Internal Revenue Code (IRC), which outlines the specific requirements and guidelines for claiming this deduction.

Under the 110 1-D Deduction, eligible businesses can deduct expenses related to the creation or improvement of a product or process that involves technical uncertainty. This deduction provides an incentive for businesses to invest in research and development, as it helps offset the costs associated with these activities.

Read Also: Can I use Robinhood in Albania? | Guide to Trading in Albania

To qualify for the 110 1-D Deduction, a business must meet certain criteria outlined in section 110 of the IRC. The research and development activities must be conducted in the United States, and the business must demonstrate that there was a technical uncertainty that it needed to resolve.

The deduction is calculated based on the qualified research expenses (QREs) incurred by the business. QREs include expenses such as wages, supplies, and contract research costs that are directly related to the research and development activities. The deduction amount can vary depending on the specific circumstances of the business and the nature of the R&D activities.

It’s important for businesses to carefully document their R&D activities and expenses in order to support their claim for the 110 1-D Deduction. This documentation can include project descriptions, employee time sheets, and records of expenses incurred.

In conclusion, the 110 1-D Deduction is a valuable tax benefit that encourages businesses to invest in research and development. By allowing businesses to deduct the costs associated with qualifying R&D activities, this deduction helps to spur innovation and drive economic growth.

Read Also: Comparing the Best Forex Ma's: Which is the Top Choice?

The 110 1-D Deduction, also known as the De Minimis Safe Harbor election, is a tax provision introduced by the Internal Revenue Service (IRS) to simplify the capitalization and depreciation of certain tangible property. This deduction allows businesses to expense rather than capitalize assets with a depreciable life of 20 years or less and a cost of $5,000 or less per item.

By electing the 110 1-D Deduction, businesses can deduct the full cost of these assets in the year they are placed in service, instead of depreciating them over several years. This provides immediate tax savings and reduces the administrative burden of tracking and calculating depreciation expenses.

However, it’s important to note that the 110 1-D Deduction is optional and businesses may choose not to elect it. In that case, they would continue to follow standard capitalization and depreciation rules for qualifying assets.

To qualify for the 110 1-D Deduction, businesses must have an applicable financial statement (AFS) or follow book-tax conformity rules. This means that the business’s financial statements must be prepared under Generally Accepted Accounting Principles (GAAP) or International Financial Reporting Standards (IFRS) and meet certain requirements.

It’s also worth mentioning that the 110 1-D Deduction is subject to certain limitations. For example, if a business exceeds the annual limit of $2,500 per item, the excess amount must be capitalized and depreciated over its useful life. Additionally, the deduction cannot be used for structural components of a building or certain types of property, such as land, inventory, or intangible assets.

In conclusion, the 110 1-D Deduction provides businesses with a simplified and advantageous method for expensing certain tangible assets. By electing this deduction, businesses can reduce their tax liability and streamline their tax compliance processes.

The 110 1-D deduction is a tax deduction that enables business owners to deduct the full cost of qualifying property in the year it is placed in service, rather than depreciating it over a number of years.

Any business owner who purchases and places qualifying property into service during the tax year is eligible for the 110 1-D deduction.

Yes, certainly. When a business owner purchases qualifying property, they can deduct the full cost of the property on their tax return for the year it is placed in service. This deduction can significantly reduce the business’s taxable income and therefore their tax liability.

Qualifying property includes tangible property such as machinery, equipment, furniture, and certain types of vehicles. It also includes some improvements made to non-residential real property, such as roofs, HVAC systems, and fire protection systems.

Yes, there are certain limits and restrictions to be aware of. For example, there is a dollar limit on the total amount that can be deducted in a given tax year. Additionally, not all types of property qualify for the full deduction, and there are specific rules regarding the timing of when the property must be placed in service.

Understanding the Foreign Exchange Fluctuation Account When conducting business internationally, companies often face the challenge of dealing with …

Read Article

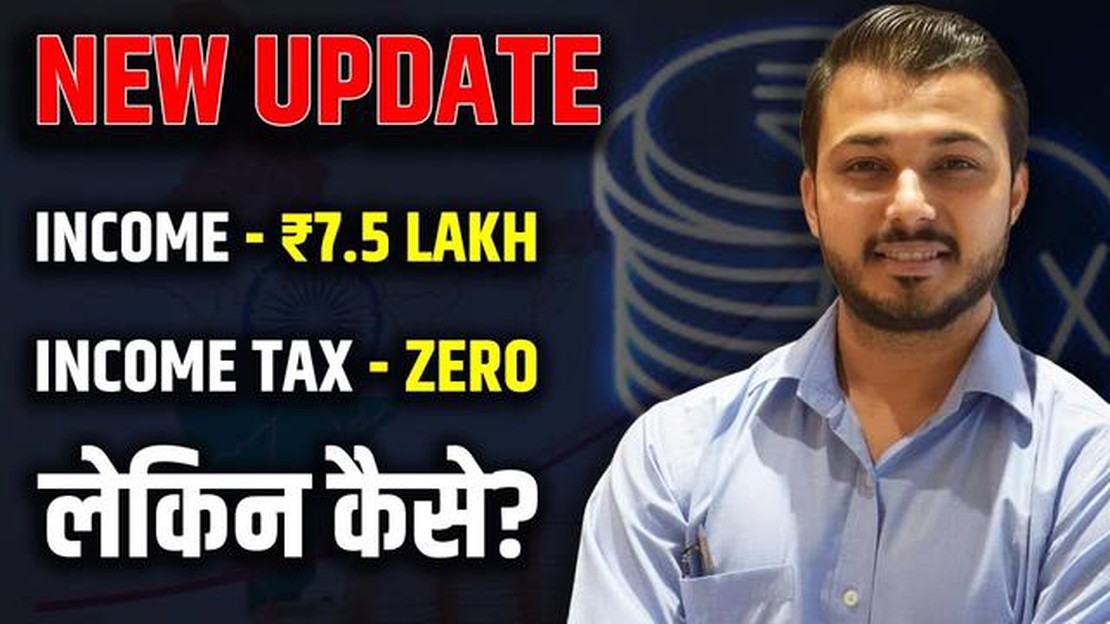

What is the tax rate on 7.5 lakhs? Calculating tax can be a daunting task, especially when it comes to higher incomes. If you earn 7.5 lakhs per year, …

Read Article

Is Kraken trusted? When it comes to investing in cryptocurrencies, one of the most important factors to consider is the reliability and security of …

Read Article

Difference between HDPE and PVC board: Which one is better for your project? When it comes to selecting the right building material for your project, …

Read Article

Examples of Over-the-Counter (OTC) Trades Over-the-Counter (OTC) trading is a decentralized market where financial instruments, such as stocks, bonds, …

Read Article

Examples of E-commerce Systems With the rise of the internet, e-commerce has become an integral part of our daily lives. From buying clothes to …

Read Article