Discover the Most Effective Trading Strategy for Consistent Profits

Discover the Ultimate Trading Strategy for Consistent Profits Are you tired of guessing which trades will bring you profits and which ones will result …

Read Article

Autoregressive (AR) and Moving Average (MA) models are two commonly used time series models in statistics and econometrics. These models have been extensively used in various fields, such as finance, economics, and engineering, to analyze and forecast time series data.

An autoregressive model is a linear regression model that uses lagged values of the dependent variable as predictors. It assumes that the current value of the variable is a linear combination of its past values and a random error term. The order of the autoregressive model, denoted by AR(p), specifies the number of lagged values included in the model. A higher order AR model captures more complex dependencies in the data, but it also increases the number of parameters and computational complexity.

A moving average model, on the other hand, is a linear regression model that uses lagged values of the error term as predictors. It assumes that the current value of the variable is a linear combination of past error terms and a random error term. The order of the moving average model, denoted by MA(q), specifies the number of lagged error terms included in the model. Similar to the autoregressive model, a higher order moving average model captures more complex dependencies but increases the complexity of the model.

AR and MA models can be combined to create an autoregressive moving average (ARMA) model, which combines the dependencies on past values of the variable and past error terms. The ARMA model is widely used in the analysis of time series data because it provides a flexible and powerful framework for modeling complex dependencies and making accurate forecasts.

In summary, autoregressive and moving average models are essential tools for analyzing and forecasting time series data. By understanding the basics of these models, analysts and researchers can gain valuable insights into the underlying patterns and dynamics of the data, and make informed decisions based on reliable forecasts.

In time series analysis, an autoregressive (AR) model is a type of statistical model used to understand and predict patterns in a sequence of data points. Autoregressive models are based on the idea that future values of a variable can be predicted using past values of the same variable. The word “autoregressive” indicates that the regression is performed on a variable with itself as the predictor.

Autoregressive models are commonly used in various fields such as economics, finance, meteorology, and engineering to analyze and forecast time-dependent data. They are particularly useful for modeling data with trends and patterns that persist over time.

An autoregressive model of order p, denoted AR(p), is represented by the equation:

Xt = β0 + β1Xt-1 + β2Xt-2 + … + βpXt-p + εt

Where:

For example, an AR(1) model can be written as:

Xt = β0 + β1Xt-1 + εt

This equation states that the value of the variable at time t depends on its previous value at time t-1, along with an error term εt. The parameter β1 represents the influence or weight of the previous value on the current value.

Read Also: Who did the Penguins trade in 2023? Learn the latest trades and transfers

The order of the autoregressive model, p, determines how many previous values of the variable are considered in the model. A higher value of p captures more complex patterns and dependencies in the data, but may also introduce more parameters to estimate.

Autoregressive models can be estimated using time series data and various statistical techniques, such as ordinary least squares regression or maximum likelihood estimation. Once the model parameters are estimated, the model can be used to predict future values of the variable.

Overall, autoregressive models provide a flexible and powerful approach to analyze and predict time series data. By capturing patterns and dependencies in the data, they offer valuable insights into the underlying dynamics and can be used for forecasting and decision-making in a wide range of applications.

Autoregressive and moving average models are statistical models used to analyze time series data. These models are commonly used in fields such as economics, finance, and meteorology to make predictions and understand the underlying patterns in a dataset.

An autoregressive (AR) model is a time series model in which the current value of a variable is linearly dependent on its previous values, along with a random error term. The order of the AR model, denoted as p, represents the number of previous values taken into account. The AR(p) model can be written as:

X_t = c + φ_1 * Xt-1 + φ_2 * Xt-2 + … + φ_p * Xt-p + ε_t

where X_t is the current value of the variable, c is a constant term, φ_1, φ_2, …, φ_p are the autoregressive coefficients, Xt-1, Xt-2, …, Xt-p are the previous values, and ε_t is the random error term.

A moving average (MA) model is a time series model in which the current value of a variable is linearly dependent on the previous error terms, along with a random error term. The order of the MA model, denoted as q, represents the number of previous error terms taken into account. The MA(q) model can be written as:

Read Also: Can I Trade Crude Oil 24 Hours? Discover the Trading Hours for Crude Oil

X_t = c + θ_1 * εt-1 + θ_2 * εt-2 + … + θ_q * εt-q + ε_t

where X_t is the current value of the variable, c is a constant term, θ_1, θ_2, …, θ_q are the moving average coefficients, εt-1, εt-2, …, εt-q are the previous error terms, and ε_t is the random error term.

Autoregressive and moving average models can be combined to form autoregressive moving average (ARMA) models, which allow for the analysis of both the previous values and error terms in a time series. The ARMA(p, q) model can be written as:

X_t = c + φ_1 * Xt-1 + φ_2 * Xt-2 + … + φ_p * Xt-p + θ_1 * εt-1 + θ_2 * εt-2 + … + θ_q * εt-q + ε_t

where X_t is the current value of the variable, c is a constant term, φ_1, φ_2, …, φ_p are the autoregressive coefficients, Xt-1, Xt-2, …, Xt-p are the previous values, θ_1, θ_2, …, θ_q are the moving average coefficients, εt-1, εt-2, …, εt-q are the previous error terms, and ε_t is the random error term.

Autoregressive and moving average models are valuable tools for understanding time series data and can be used for forecasting future values, identifying trends and patterns, and detecting outliers or anomalies in a dataset. By analyzing the autoregressive and moving average coefficients, we can gain insights into the underlying dynamics of a time series and make informed decisions based on the patterns observed.

An autoregressive model is a time series model that uses past observations to predict future observations. It assumes that the current value of a time series is a linear combination of its past values.

A moving average model is a time series model that uses the average of past observations to predict future observations. It assumes that the current value of a time series is a linear combination of its past error terms.

Autoregressive models are useful for analyzing and forecasting time series data. They can capture the linear relationships between a time series and its past values, making them suitable for predicting future values.

No, autoregressive models assume a linear relationship between a time series and its past values. If the relationship is non-linear, other types of models such as neural networks or support vector machines may be more appropriate.

The main difference between autoregressive and moving average models is how they use past observations to make predictions. Autoregressive models use past values of the time series, while moving average models use past error terms. Additionally, autoregressive models capture the relationship between a time series and its past values, while moving average models capture the relationship between a time series and its past errors.

An autoregressive (AR) model is a type of time series model that uses past values of a variable to predict future values. It assumes that the future values of the variable can be explained by a linear combination of its past values.

Discover the Ultimate Trading Strategy for Consistent Profits Are you tired of guessing which trades will bring you profits and which ones will result …

Read Article

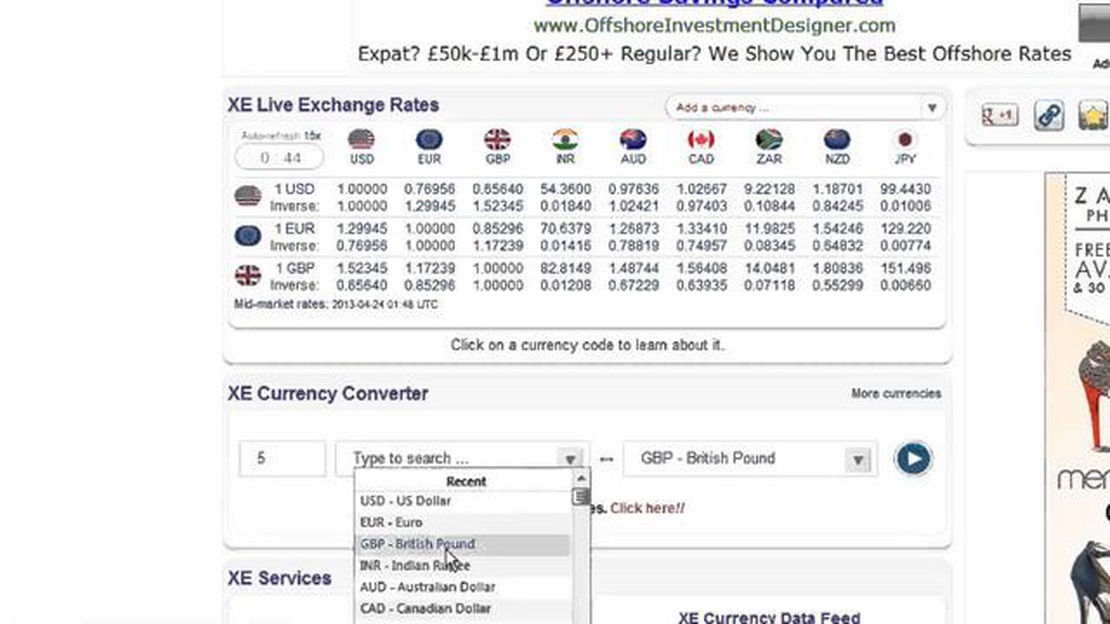

Best App to Check Dollar Rate If you frequently deal with currency conversions or often travel to countries where the dollar rate is different, having …

Read Article

What is the best EMA for 4h? When it comes to trading in the financial markets, having the right indicators is crucial. One popular indicator that …

Read Article

Discover the Fascinating World of Forex Trading Forex trading, also known as foreign exchange trading, is a popular and exciting investment option …

Read Article

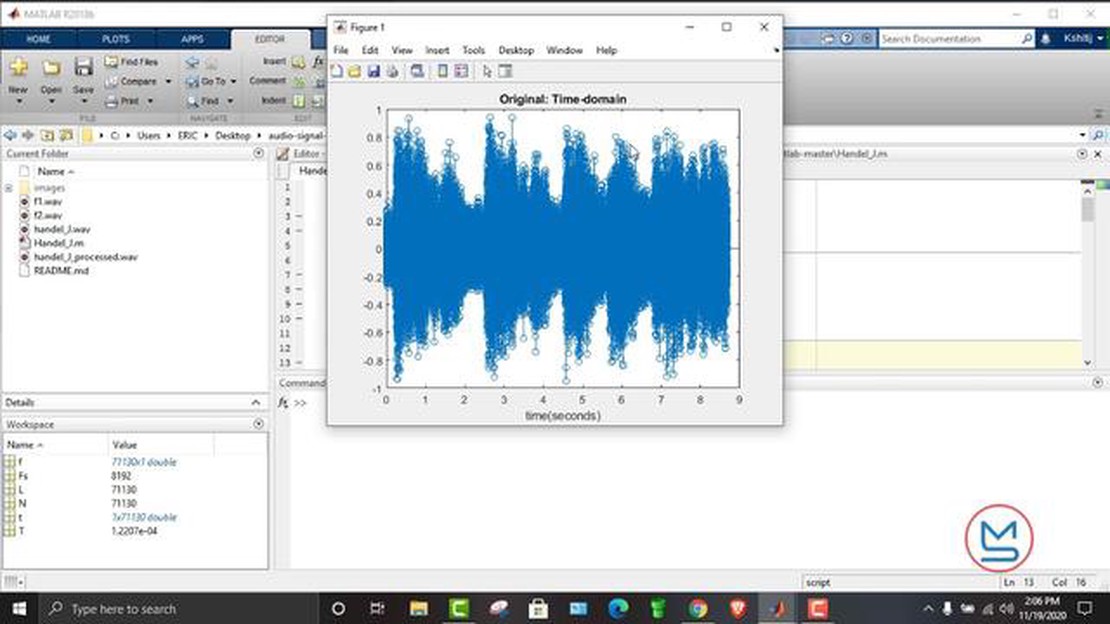

Guide: Filtering Noise from Data Noise is a common and often unavoidable problem when working with data. It can significantly distort or obscure the …

Read Article

When is the Right Time to Sell Employee Stock Options? Employee stock options can be a valuable benefit that many companies offer to their employees. …

Read Article