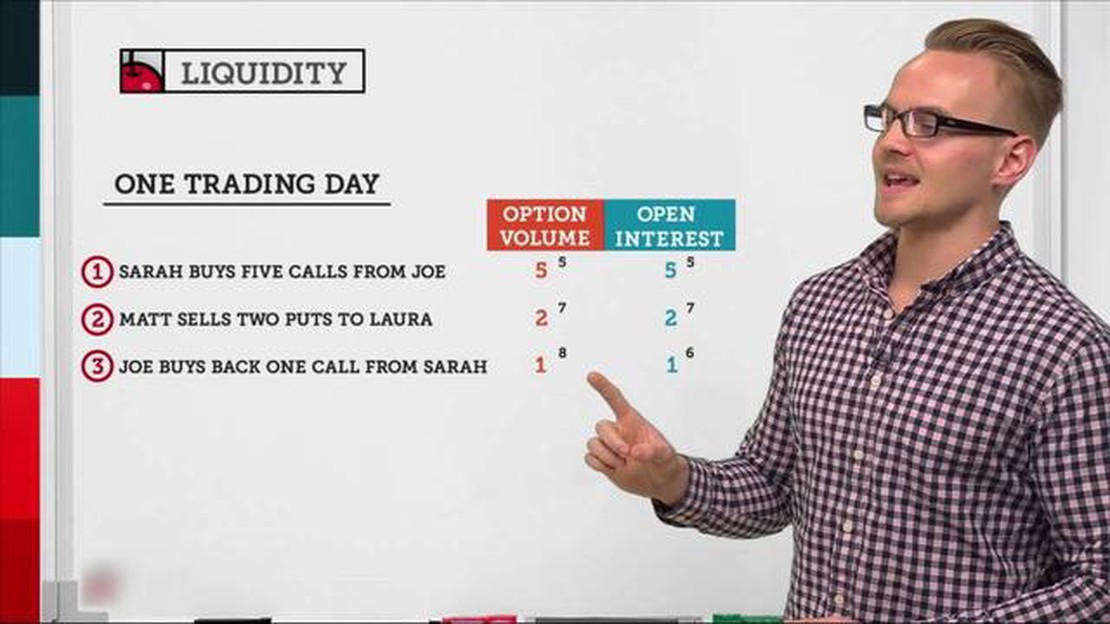

Understanding Open Interest Liquidity for Options: A Comprehensive Guide

What is open interest liquidity for options? Options trading can be a complex endeavor, requiring careful analysis and understanding of various …

Read Article

When it comes to reporting the sale of non-qualified stock options, it’s important to understand the rules and regulations that govern this type of transaction. Non-qualified stock options (NSOs) are a popular form of compensation for employees, but they can also pose some complex reporting requirements for both employers and employees.

One of the key considerations when reporting the sale of NSOs is determining the cost basis for the stock. The cost basis is the amount paid for the stock, including any fees or commissions. This information is important for calculating the capital gain or loss on the sale of the stock.

In addition to determining the cost basis, it’s also important to report the sale of NSOs on the appropriate tax forms. Employees who sell NSOs must report the sale on Schedule D of their individual tax return, using Form 8949 to report the details of each sale. Employers are also required to report the sale on Form W-2, providing employees with the necessary information for completing their tax return.

Overall, reporting the sale of non-qualified stock options can be a complex process. It’s important to consult with a qualified tax professional or financial advisor to ensure compliance with all reporting requirements and to maximize any potential tax benefits.

Non-qualified stock options, also known as NSOs or NQSOs, are a type of stock option that does not qualify for the same tax advantages as incentive stock options (ISOs). These options are typically offered to employees or other service providers as part of their compensation package.

Unlike ISOs, non-qualified stock options are subject to ordinary income tax rates on the difference between the exercise price and the fair market value of the stock at the time of exercise. This means that the recipient of the option will need to pay taxes on the value of the option at the time it is exercised, based on their ordinary income tax rate.

Non-qualified stock options also have different requirements and restrictions compared to ISOs. They may have a shorter exercise period, be subject to different vesting schedules, and have different rules regarding transferability.

Overall, non-qualified stock options can provide a valuable form of compensation for employees and service providers. However, it is important to understand the tax implications and requirements associated with these options in order to effectively manage them. Reporting the sale of non-qualified stock options accurately is crucial for avoiding penalties and ensuring compliance with tax regulations.

Non-qualified stock options (NQSOs) are a type of stock options that are granted to employees as a form of compensation. They have several key features that distinguish them from other types of stock options:

Vesting Schedule: NQSOs typically have a vesting schedule, which is a predetermined timeline over which the employee gains the right to exercise the options. The vesting schedule can be based on time (e.g., four years with a one-year cliff) or performance-based (e.g., achieving certain milestones).

Exercise Price: The exercise price, also known as the strike price, is the price at which the employee can buy the stock when exercising the options. Unlike incentive stock options (ISOs), the exercise price of NQSOs is generally set at the fair market value of the stock on the date of grant.

Tax Treatment: NQSOs are subject to tax at the time of exercise. The difference between the fair market value of the stock at the time of exercise and the exercise price is taxable as ordinary income. Additionally, any subsequent gain or loss from the sale of the stock is subject to capital gains tax.

No Limitations: Unlike ISOs, there are no limitations on who can receive NQSOs. They can be granted to employees, consultants, and even non-employees. This makes NQSOs a more flexible form of equity compensation.

No Alternative Minimum Tax (AMT): NQSOs are not subject to the alternative minimum tax (AMT). This can be advantageous for employees, as the AMT can limit the benefits of ISOs for high-income individuals.

No Qualifying Holding Period: NQSOs do not have a qualifying holding period requirement, unlike ISOs. This means that employees can exercise and sell their NQSOs immediately if they choose to do so.

Read Also: Top LMAX Competitors in the Market | Comparison and Analysis

No Limitations on Exercise Timing: NQSOs do not have a time limit for exercising the options after leaving the company. This gives employees more flexibility in deciding when to exercise their stock options.

In conclusion, non-qualified stock options have certain key features, such as vesting schedules, taxable income at exercise, and no AMT or holding period requirements. These features make NQSOs a popular choice for companies looking to provide equity compensation to their employees.

When it comes to non-qualified stock options (NSOs), reporting the sale is an important task for both the employee and the employer. The following information outlines the reporting requirements for NSOs.

1. Form 3921: The employer is responsible for providing the employee with Form 3921, “Exercise of an Incentive Stock Option Under Section 422(b)”. This form must be provided to the employee by January 31st of the year following the year in which the NSOs were exercised.

Read Also: Beginner's guide: How to trade in options in ICICIdirect

2. Schedule D: The employee needs to report the sale of NSOs on Schedule D of their individual tax return. The sale should be reported as a short-term or long-term capital gain, depending on the holding period of the stock.

3. Reporting the Cost Basis: The employee should report the cost basis of the stock as the exercise price plus any amount included in their income as compensation. This information can be found on Form 3921 provided by the employer.

4. Reporting the Proceeds: The employee should report the proceeds from the sale of the NSOs as the cash received minus any transaction fees or commissions paid.

5. Form 1099-B: The brokerage or financial institution that facilitated the sale of the NSOs should provide the employee with Form 1099-B, “Proceeds from Broker and Barter Exchange Transactions”. This form should be provided to the employee by February 15th of the year following the year in which the sale occurred.

6. Reporting the Sale: The employee needs to report the sale of the NSOs on their individual tax return using the information provided on Form 1099-B. The reported proceeds should match the information reported on Schedule D.

It is important for both the employee and the employer to accurately report the sale of NSOs to ensure compliance with tax regulations. Failure to properly report the sale could result in penalties and additional taxes.

Non-qualified stock options are a type of employee stock option that can be granted to employees as part of their compensation package. Unlike qualified stock options, non-qualified stock options do not meet specific requirements set by the IRS and are therefore subject to different tax treatment.

You should report the sale of non-qualified stock options when you file your annual tax return. The exact reporting requirements may vary depending on your individual circumstances, so it’s best to consult with a tax professional or refer to the IRS guidelines for more specific guidance.

Non-qualified stock options are subject to taxation at the time of exercise. The spread between the fair market value of the stock at the time of exercise and the exercise price is considered taxable income. This income is subject to both ordinary income tax rates and, in some cases, additional Medicare or Social Security taxes.

Yes, you may be able to deduct certain expenses related to the sale of non-qualified stock options. For example, if you incur brokerage fees or commissions when selling the stock, these expenses can generally be deducted on your tax return. However, it’s important to keep detailed records and consult with a tax professional to ensure you are eligible for any deductions.

Yes, if you hold non-qualified stock options in a foreign brokerage account, there may be additional reporting requirements. Generally, if the aggregate value of your foreign financial accounts exceeds certain thresholds, you may be required to file a Report of Foreign Bank and Financial Accounts (FBAR) and disclose the details of your foreign holdings. It’s important to consult with a tax professional or refer to the IRS guidelines for more specific information.

Non-qualified stock options are a type of stock option that do not qualify for special tax treatment. They are typically granted to employees as part of their compensation packages, and allow the holder to purchase company stock at a predetermined price at a future date. When the options are exercised and the stock is sold, any gains are subject to ordinary income tax rates.

When non-qualified stock options are exercised and the stock is sold, the gain from the sale must be reported on the individual’s tax return. The gain is calculated as the difference between the exercise price of the options and the fair market value of the stock at the time of exercise. This gain is subject to ordinary income tax rates and must be reported as income on Form 1040.

What is open interest liquidity for options? Options trading can be a complex endeavor, requiring careful analysis and understanding of various …

Read Article

Trading US Options from India with Interactive Brokers: Everything You Need to Know Are you an investor in India looking to trade US options? Look no …

Read Article

Understanding the Role of Fundamental Analysis in the Stock Market When it comes to investing in the stock market, it’s important to have a thorough …

Read Article

Trade Confirmation: How to Obtain It Trade confirmation is a crucial aspect of any financial transaction, providing both parties involved with an …

Read Article

4h Time Frame Strategy: Everything You Need to Know In the world of trading, time frames play a crucial role in determining the success of a strategy. …

Read Article

Shipping Time: How Long Does It Take for a Cargo Ship to Travel from China? When it comes to shipping goods internationally, one of the most common …

Read Article