Who is the owner of XM? Discover the company behind XM and its ownership structure

Who is the owner of XM? XM is a globally recognized financial services provider that offers online trading on the forex and CFD markets. The company …

Read Article

Forex tax can be a complex and confusing topic for many traders. Understanding the rules and regulations surrounding taxes on foreign exchange trading is crucial for staying compliant and avoiding unnecessary penalties. This comprehensive guide will provide you with all the information you need to navigate the world of forex tax.

First and foremost, it’s important to understand that forex tax laws can vary from country to country. Each country has its own tax regulations governing forex trading, and it’s essential to familiarize yourself with the specific rules in your jurisdiction. Failure to comply with these regulations can lead to hefty fines and legal consequences.

One of the key factors that determine forex tax liability is your trading status. Are you a casual trader or a professional trader? The distinction between the two can have significant tax implications. Casual traders are typically subject to capital gains tax, while professional traders may be classified as self-employed and subject to income tax.

Keeping accurate and detailed records of all your forex transactions is crucial when it comes to tax time. This includes records of every trade you make, including dates, times, and amounts. In addition, you should also keep track of any expenses related to your forex trading, such as trading platform fees, educational resources, and internet costs. These records will help ensure that you report your earnings and deductions correctly and avoid any potential audits or penalties.

In conclusion, paying forex tax requires careful attention to detail and compliance with the specific tax regulations in your country. By understanding the rules that govern forex tax, determining your trading status, and keeping accurate records, you can navigate the tax landscape confidently and avoid any potential issues. Remember to consult with a tax professional to ensure that you understand the specific requirements and guidelines for forex tax in your jurisdiction.

Forex trading can bring significant profits, but it also comes with various tax obligations. Understanding how forex taxation works is crucial for traders to comply with tax regulations and avoid penalties. Here are some key points to consider:

Read Also: Easy Ways to Make $1,000 in a Day: Tried and Tested Methods

It is important for forex traders to consult with a tax professional or accountant who has knowledge and experience in forex taxation. They can provide guidance on how to correctly report and pay taxes on forex trading activities based on the relevant tax laws and regulations.

By understanding forex taxation and staying compliant with tax obligations, traders can focus on their trading strategies and goals without the worry of facing tax-related issues and penalties.

When it comes to paying forex tax, there are several key factors that you need to consider. These factors can help ensure that you are accurately calculating and reporting your forex income and paying the appropriate taxes.

By considering these key factors, you can navigate the process of paying forex tax more effectively and minimize the risk of errors or potential penalties. Remember, tax regulations can be subject to change, so staying informed and seeking professional advice is essential for successful forex tax compliance.

Read Also: How to Withdraw Money from FXOpen: Step-by-Step Guide

Forex tax refers to the taxes paid on profits made through forex trading. It is a form of tax that individuals or businesses trading in the foreign exchange market may have to pay.

Yes, in most countries, forex gains are subject to taxation. The specific tax rules and rates may vary depending on your jurisdiction, so it is important to consult with a tax professional or regulator to understand your obligations.

Forex taxes are generally calculated based on the net profit or loss from your forex trading activities. This means that you would subtract your total losses from your total gains to determine the taxable amount. The tax rate applied to the taxable amount will depend on your country’s tax laws.

Some countries may offer tax exemptions or special tax treatment for forex traders. For example, in the United States, traders who qualify as “traders in securities” may be eligible for certain tax advantages. However, these exemptions and treatments are often subject to specific criteria and conditions, so it is important to consult with a tax professional to determine if you qualify.

The consequences of not paying forex taxes can vary depending on your jurisdiction. In some countries, failure to pay taxes on forex gains could result in penalties, fines, or even legal action. It is important to comply with your tax obligations to avoid any potential consequences.

Who is the owner of XM? XM is a globally recognized financial services provider that offers online trading on the forex and CFD markets. The company …

Read Article

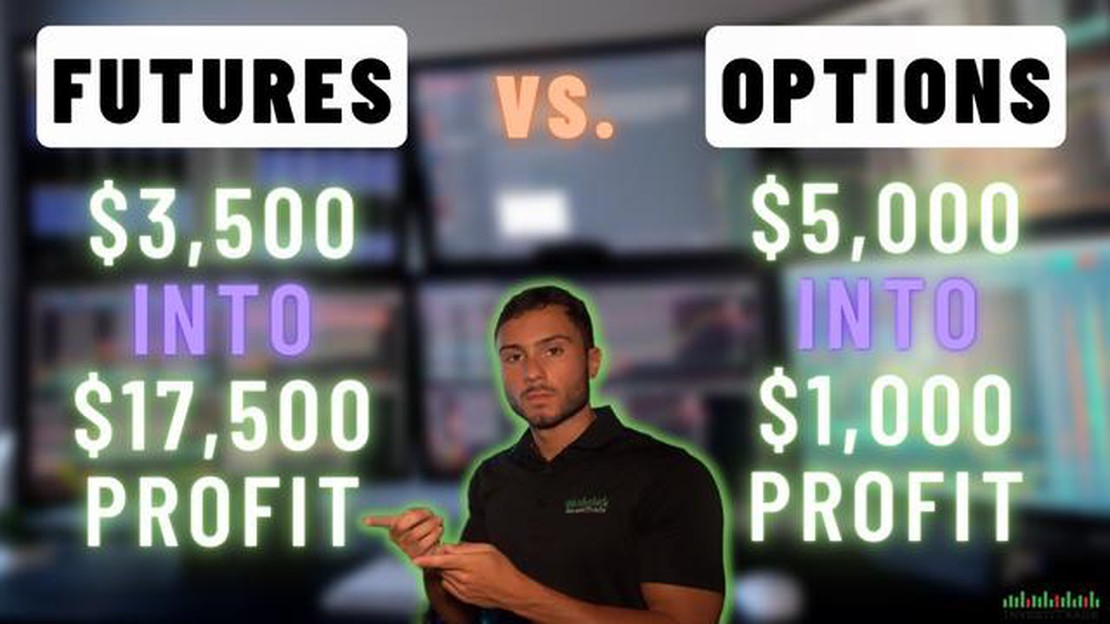

Which is better: Futures or Options? Investing in the financial markets can be a daunting task, especially when it comes to choosing between different …

Read Article

How to Withdraw from Meta Trader 5 Withdrawing funds from your Meta Trader 5 account is a simple and straightforward process. Whether you want to cash …

Read Article

RSO Restricted Stock Options Explained In the world of finance, there are various ways for employees to receive compensation from their employers. One …

Read Article

Is Forex Factory Legit? Find Out the Truth Here Forex Factory is a popular online platform that provides traders with access to a wealth of …

Read Article

Beginner’s guide to trading options on ICICIdirect Options trading can be a lucrative investment opportunity if you have the right knowledge and …

Read Article