Stock Distribution at Meta: What Employees Can Expect

Stock options for Meta employees: How much do they receive? When it comes to working at Meta, formerly known as Facebook, there are many benefits that …

Read Article

Call options are financial instruments that give the holder the right, but not the obligation, to purchase an underlying asset at a specified price within a specific period of time. For investors and businesses, accounting for call options is an essential aspect of financial reporting. Understanding how to account for call options is crucial for accurately valuing and reporting a company’s financial position.

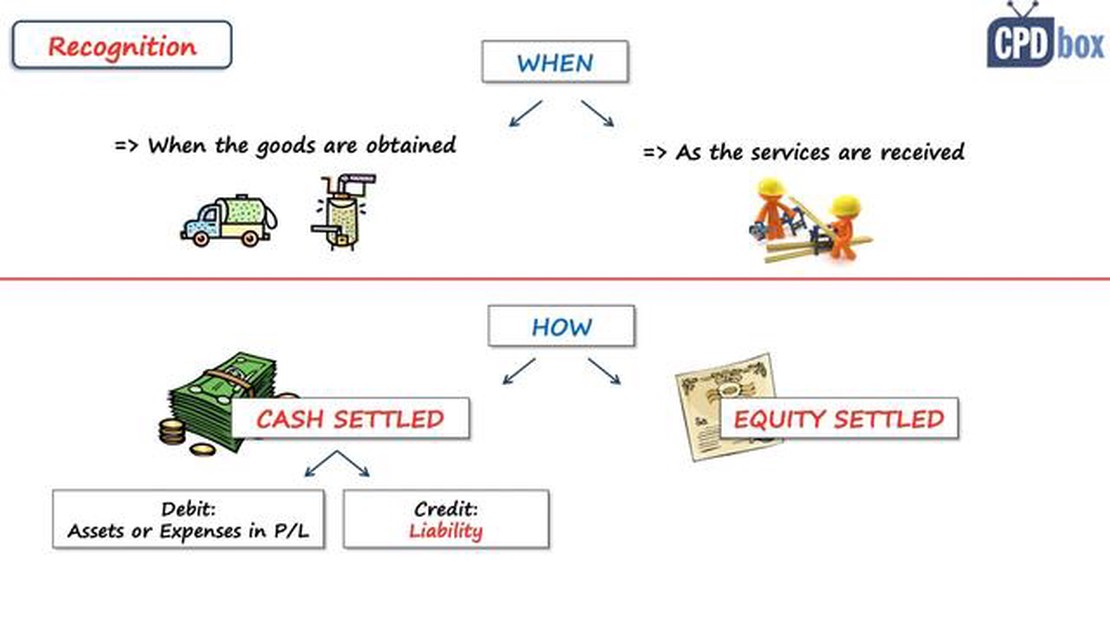

When accounting for a call option, it is important to consider the initial recognition, subsequent measurement, and disclosure requirements. Firstly, the call option should be recognized as a financial instrument on the balance sheet at its fair value at the date of acquisition. The fair value is determined based on market prices or using appropriate valuation techniques.

Subsequently, the call option should be measured at fair value in the balance sheet at each reporting date, with changes in fair value recognized in the income statement. This ensures that the call option is reflected at its current market value, providing a more accurate representation of the entity’s financial position. It is important to note that fair value changes are classified as either realized gains or losses, which occur when options are exercised, or unrealized gains or losses, which occur when the value of the option changes without exercise.

In addition to measurement, proper disclosure of call options is also necessary. The financial statements should include adequate disclosures regarding the nature and extent of risks arising from call options, including information about the terms and conditions of the options, as well as any relevant hedging activities. These disclosures help users of the financial statements understand the impact of call options on the entity’s financial performance and risk exposure.

In conclusion, accounting for call options requires careful consideration of their initial recognition, subsequent measurement, and disclosure requirements. By accurately accounting for call options, companies can provide users of financial statements with a clear understanding of their financial position and the risks associated with these financial instruments.

A call option is a financial contract that gives the owner the right, but not the obligation, to buy a specific quantity of an underlying asset at a predetermined price, known as the strike price, within a specified time period. This underlying asset can be a stock, a bond, a commodity, or even a currency.

Call options are considered bullish because they provide the opportunity to profit from price increases in the underlying asset. As the price of the underlying asset rises, the value of the call option also increases. However, if the price of the underlying asset does not rise above the strike price within the specified time period, the call option may expire worthless.

Read Also: When My Stock Options Vest: A Guide to Making the Right Decisions

When an investor buys a call option, they pay a premium to the option seller. This premium is the price of the option contract and is determined based on several factors, including the current price of the underlying asset, the strike price, the time remaining until expiration, and market volatility.

There are several key terms and concepts related to call options that investors should understand:

Understanding call options is essential for investors looking to participate in options trading. By understanding these key concepts and terms, investors can make informed decisions and effectively manage their risk. Whether used for speculation or hedging purposes, call options can be a valuable tool in a diversified investment strategy.

Call options are a type of financial instrument that give the holder the right, but not the obligation, to buy an underlying asset at a specified price within a certain period of time. When accounting for call options, it is important to understand the key elements and how to properly classify and report them in financial statements.

There are several key considerations when accounting for call options:

| 1. Initial Measurement | When a call option is purchased, it is initially measured at its fair value. The fair value of the call option is determined by considering various factors such as the underlying asset price, strike price, time to expiration, and market volatility. |

| 2. Classification | Call options can be classified as either financial liabilities or derivatives depending on their specific characteristics. If the call option meets certain criteria, it is classified as a financial liability and is subsequently measured at fair value with changes in fair value recognized in the income statement. If the call option is classified as a derivative, it is accounted for at fair value with changes in fair value recognized in other comprehensive income. |

| 3. Subsequent Measurement | After initial measurement, call options are subsequently measured at fair value. Changes in the fair value of call options that are classified as financial liabilities are recognized in the income statement, while changes in the fair value of call options that are classified as derivatives are recognized in other comprehensive income. |

| 4. Disclosure | Companies are required to disclose information about call options in their financial statements. This includes providing details about the nature and extent of call option arrangements, the measurement and classification of call options, and any significant changes in fair value. |

Read Also: Learn about the Apple covered call strategy | All you need to know

Accounting for call options requires a thorough understanding of the specific rules and regulations governing financial reporting. It is important for companies to consult with accounting professionals and ensure compliance with applicable standards.

A call option is a financial contract that gives the holder the right, but not the obligation, to buy an underlying asset at a specific price within a certain period of time.

Accounting for a call option depends on whether it is classified as a hedge, a speculative investment, or a financial instrument. Generally, a call option is recorded at cost and updated to fair value at the end of each reporting period.

Calculating the fair value of a call option involves considering factors such as the current price of the underlying asset, the strike price of the option, the time to expiration, volatility, and interest rates. There are various mathematical models available, such as the Black-Scholes model, that can be used to estimate the fair value.

If a call option is designated as a hedge for a specific risk, such as interest rate risk or foreign exchange risk, it may qualify for special hedge accounting treatment. In this case, the changes in the fair value of the option are recognized in the income statement together with the changes in the fair value of the hedged item.

Stock options for Meta employees: How much do they receive? When it comes to working at Meta, formerly known as Facebook, there are many benefits that …

Read Article

How to Determine Whether a Forex Factory Has High Impact News Forex Factory is an online platform that provides traders with valuable information …

Read Article

Valuing Share Option Plans According to IFRS 2 Valuing share options is a complex and critical task for companies that offer these plans to their …

Read Article

Understanding Forex Charges on American Express Credit Card In today’s global economy, international travel and online shopping have become more …

Read Article

What are the necessary requirements for trading? Starting a career in trading can be an exciting and potentially profitable venture. However, it is …

Read Article

Is MasterCard exchange rate good? When it comes to traveling abroad or making international purchases, it’s important to consider the foreign exchange …

Read Article