Guide to Hedging Currency with Options: Effective Strategies and Tips

How to Hedge Currency with Options When investing in foreign markets, the fluctuation of currency exchange rates can significantly impact the returns …

Read Article

When it comes to trading options, it’s important to understand the tax implications and know how to report your option sales on your tax return. Options trading can be a lucrative venture, but it can also lead to complex tax situations if not properly reported.

First and foremost, it’s essential to keep track of all your options transactions throughout the year. This includes recording the dates of sale, the strike price, the number of contracts bought or sold, and the premium received or paid. By maintaining accurate records, you’ll have the necessary information when it’s time to report your option sales to the Internal Revenue Service (IRS).

When reporting option sales on your tax return, you’ll need to determine whether the sale results in a capital gain or loss. If you held the option for less than a year before selling, it’s considered a short-term capital gain or loss. On the other hand, if you held the option for more than a year, it’s categorized as a long-term capital gain or loss. This classification affects the tax rate you’ll pay on the transaction.

It’s important to note that options trading involves unique tax rules and requirements that differ from other types of investments. The IRS treats options as either “covered” or “uncovered.” Covered options are those for which the underlying security is owned, while uncovered options are not backed by an existing position in the underlying security.

Understanding the tax implications of options trading and properly reporting your option sales is crucial for avoiding unnecessary penalties and ensuring compliance with tax laws. By carefully keeping track of your transactions and seeking professional help if needed, you can navigate the complex world of options trading taxes with confidence.

Reporting option sales on your tax return correctly is essential to ensure compliance with IRS regulations and avoid any potential penalties. In this comprehensive guide, we will walk you through the steps involved in reporting option sales on your tax return, from determining the correct form to use to understanding how to report the relevant information accurately.

Determine the Correct Form: The form you should use to report your option sales depends on your specific situation. If you sold options through a brokerage account, you will typically receive a Form 1099-B from the broker. This form will include the necessary information needed to report your option sales on your tax return.

Identify the Type of Option: It is important to identify whether the options you sold were classified as non-qualified or incentive stock options. Non-qualified options are more common and typically subject to ordinary income tax rates. Incentive stock options may qualify for special tax treatment.

Report the Sale: On your tax return, you will report the sale of options in the appropriate section. If you received a Form 1099-B, the information from the form will be used to complete the necessary sections accurately. Be sure to review the information before entering it on your tax return to ensure accuracy.

Calculate the Gain or Loss: To calculate the gain or loss from the sale of options, you will need to know the cost basis and the sale price. The cost basis is usually the price you paid for acquiring the options, including any fees or commissions. The sale price is the amount you received from selling the options. Subtract the cost basis from the sale price to determine the gain or loss.

Report the Gain or Loss: Report the gain or loss from the sale of options on the appropriate tax form. Non-qualified options are reported on Schedule D of Form 1040, while incentive stock options may require additional forms, such as Form 6251. Make sure to follow the instructions provided by the IRS and accurately report the gain or loss.

Read Also: How to Log into MetaTrader 4 with Forex.com: A Step-by-Step Guide

Keep Records: It is crucial to keep detailed records of your option sales, including the date of purchase, the date of the sale, the cost basis, and the sale price. These records will help you accurately report your option sales on your tax return and provide documentation in case of an audit.

Seek Professional Advice: If you are unsure about how to report option sales on your tax return or have complex transactions, it is always beneficial to seek the advice of a qualified tax professional. They can guide you through the reporting process and help ensure that you are in compliance with IRS regulations.

Reporting option sales on your tax return may seem intimidating, but by following these guidelines and seeking professional advice when needed, you can accurately report your option sales and avoid any unnecessary stress. Remember to keep accurate records and review your tax return before filing to ensure accuracy.

When it comes to reporting option sales on your tax return, it’s important to have a clear understanding of what exactly an option sale is. An option is a contract that gives the owner the right, but not the obligation, to buy or sell an underlying asset at a specific price, known as the strike price, within a certain period of time.

Read Also: How much ground coffee can you carry to the United States?

There are two types of options – call options and put options. A call option gives the owner the right to buy the underlying asset, while a put option gives the owner the right to sell the underlying asset. Option sales occur when the owner of an option decides to exercise their right to buy or sell the underlying asset.

When you sell an option, you are essentially giving someone else the right to buy or sell the underlying asset at the strike price. The sale of an option is considered a capital transaction and may result in a capital gain or loss, depending on the price at which the option was sold and the price at which it was bought.

It’s important to note that option sales are subject to specific IRS reporting rules. If you sell options, you are required to report the transaction on Schedule D of your tax return. The information you need to report includes the date of the sale, the number of contracts sold, the sales price, the cost or basis, and the gain or loss.

Understanding the basics of option sales and the reporting requirements can help ensure that you accurately report your transactions and comply with the IRS rules. If you have any questions or are unsure about how to report your option sales, it’s always best to consult with a tax professional or seek guidance from the IRS.

To report option sales on your tax return, you need to use Form 8949 and Schedule D. Start by completing Form 8949 to report the details of each individual option transaction, including the date acquired, date sold, sales price, and cost basis. Then, transfer the total gain or loss from Form 8949 to Schedule D, which is used to calculate your overall capital gains or losses for the year.

Yes, to report option sales on your tax return, you need to use Form 8949 and Schedule D. Form 8949 is used to report the details of each individual option transaction, while Schedule D is used to calculate your overall capital gains or losses for the year.

To report option sales on your tax return, you will need to gather several pieces of information, including the date acquired, date sold, sales price, and cost basis for each individual option transaction. You will also need to know whether the transaction resulted in a short-term or long-term gain or loss.

Yes, there are specific rules for reporting option sales on your tax return. For example, if you sold options that you held for one year or less, the resulting gain or loss is considered short-term and should be reported on Part I of Schedule D. If you sold options that you held for more than one year, the resulting gain or loss is considered long-term and should be reported on Part II of Schedule D.

Failing to report option sales on your tax return can have serious consequences. The IRS has the ability to track your option transactions, and if they discover that you have unreported income, you could face penalties and interest on the unpaid taxes. It is important to report all of your option sales accurately to avoid any potential issues with the IRS.

How to Hedge Currency with Options When investing in foreign markets, the fluctuation of currency exchange rates can significantly impact the returns …

Read Article

Best Times to Trade Forex in Australia If you are interested in forex trading and live in Australia, it’s important to know when the market is open …

Read Article

Is a 4 Year Vesting Period Normal? When it comes to employee stock options, one term that often comes up is “vesting period.” The vesting period is …

Read Article

What to Expect with Stock Options After Termination Stock options can be a valuable part of an employee’s compensation package, but what happens to …

Read Article

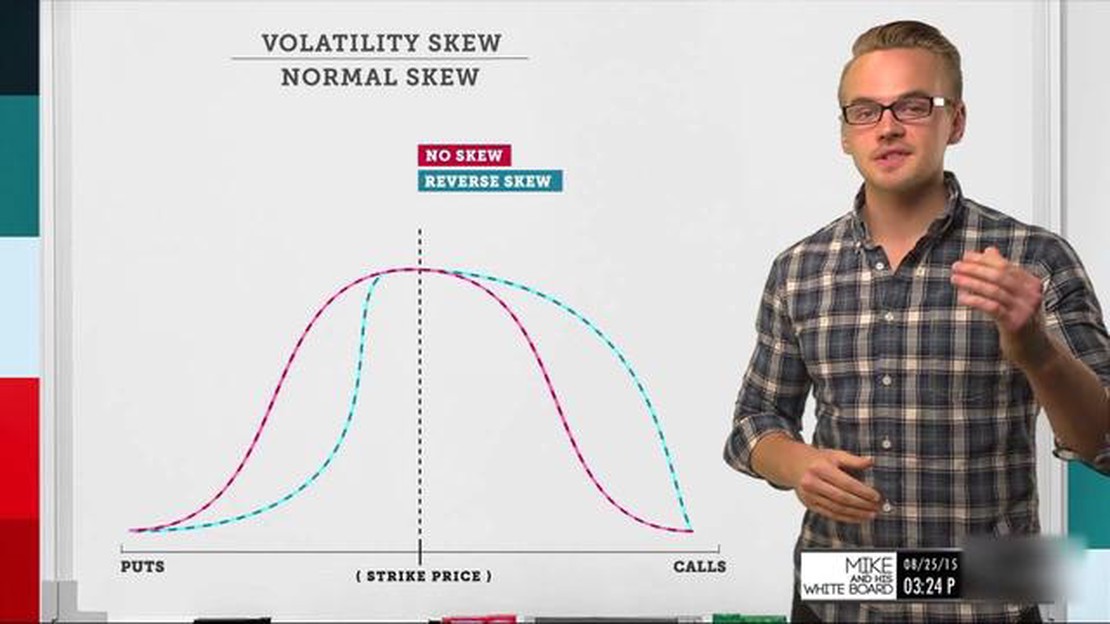

Understanding the Basics of a Skew Strategy Investing in the stock market can be a daunting task, as there are constantly new strategies and trends to …

Read Article

Is there a future for Citrix? Citrix Systems is a well-known software company that specializes in virtualization, networking, and cloud computing …

Read Article