Is There Any True 4K Content? Unveiling the Facts and Myths

Is there any true 4K content? In the era of rapidly advancing technology, the term “4K” has become increasingly popular. It promises unparalleled …

Read Article

If you are working with time series data or need to perform exponential weighted moving averages (EWM) calculations in Python, this comprehensive guide will provide you with all the necessary information. EWM is a popular statistical method used to forecast and analyze trends in data. By giving more weight to recent observations, it allows you to capture short-term fluctuations while still considering the overall trend.

In this guide, we will walk you through the EWM function in Python, covering everything from its basic syntax to advanced customization options. You will learn how to calculate EWM for a variety of scenarios, including calculating rolling averages, smoothing noisy data, and detecting anomalies. Whether you are a beginner or an experienced Python programmer, this guide will help you master the EWM function and leverage its power in your data analysis projects.

We will start by explaining the theory behind EWM and its applications in different industries. We will then dive into the code, demonstrating how to use the EWM function from popular Python libraries such as NumPy and Pandas. Throughout the guide, we will provide clear examples and step-by-step instructions, ensuring that you have a solid understanding of the concepts and can apply them to your own data.

If you are looking to enhance your data analysis skills and increase the accuracy of your forecasts, understanding and using the EWM function in Python is a must. By the end of this guide, you will be equipped with the knowledge to confidently incorporate EWM calculations into your data analysis projects, allowing you to make more informed decisions based on accurate trend analysis.

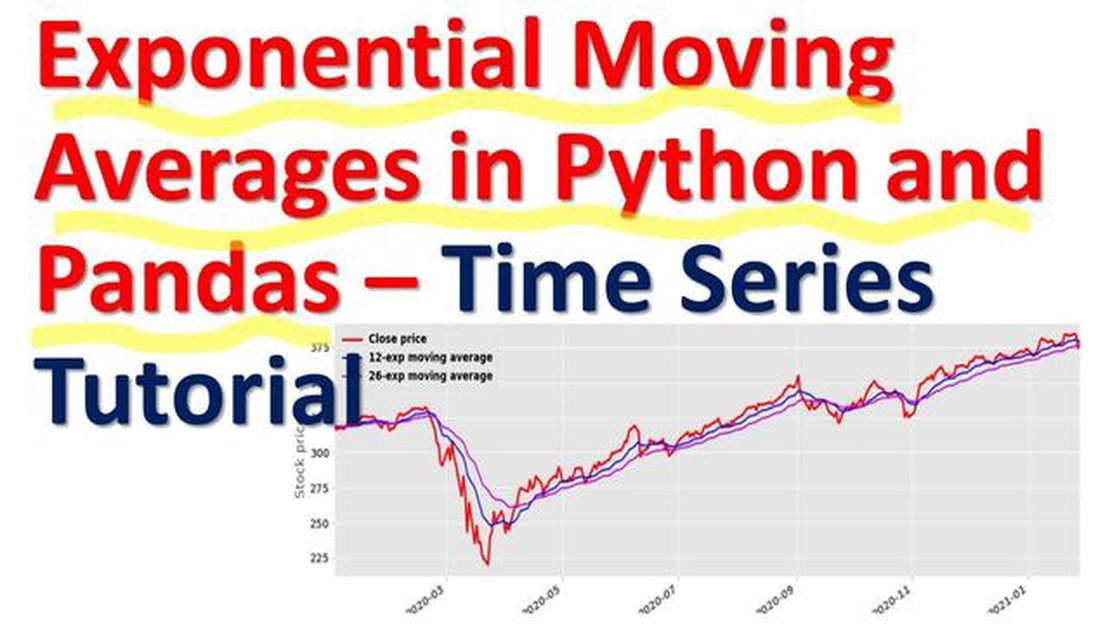

The EWM function in Python is a powerful tool that allows you to calculate the exponential weighted moving average of a time series data. It is commonly used in finance, economics, and statistics to analyze and predict trends in data.

Exponential weighted moving average calculates the average of a sequence of data points, giving more weight to recent data points and less weight to older data points. This weighting factor is determined by a parameter called the smoothing factor.

The EWM function takes several parameters, including the series of data points, the smoothing factor, and an optional parameter for adjusting the bias. By default, the EWM function adjusts the average by dividing it by 1 minus the smoothing factor, which reduces the bias towards the beginning of the series.

One of the key advantages of using the EWM function is its ability to give more importance to recent data points. This is particularly useful when analyzing time series data, where recent data is often more relevant than older data.

Another advantage of the EWM function is its flexibility. It allows you to adjust the smoothing factor to give more or less weight to recent data points, depending on your specific needs. This makes it a versatile tool that can be used in a wide range of applications.

Overall, the EWM function in Python is a valuable tool for analyzing and predicting trends in time series data. By giving more weight to recent data points, it allows you to identify patterns and make informed decisions based on the most up-to-date information.

The EWM (Exponential Weighted Moving) function in Python is a method that calculates the exponentially weighted moving average of a given sequence of values. It assigns different weights to the values based on their recency, giving more weight to the most recent data points. This makes the EWM function particularly useful for analyzing time series data, where recent observations tend to have more predictive power.

Read Also: What Does the 'N' Stand for in Moving Average?

The EWM function is implemented in the pandas library in Python, which is a powerful tool for data manipulation and analysis. The function takes several parameters, including the data series to be averaged and the span, which determines the decay factor of the weights. A smaller span value will give more weight to recent observations, while a larger span value will give equal weight to all observations.

Here is an example of how to use the EWM function in Python:

import pandas as pdimport numpy as np# Create a sample series of valuesdata = pd.Series([1, 2, 3, 4, 5])# Calculate the exponentially weighted moving averageewma = data.ewm(span=2).mean()# Display the resultprint(ewma)In this example, the EWM function is applied to a series of values [1, 2, 3, 4, 5]. The span parameter is set to 2, which means that the weights decrease exponentially with a factor of 0.5 for each preceding value. The resulting exponentially weighted moving average is printed as the output.

The EWM function in Python is a powerful tool for analyzing time series data and can be used in a variety of applications, such as financial forecasting, trend analysis, and anomaly detection. By assigning more weight to recent observations, it allows for more accurate predictions and better understanding of the underlying patterns in the data.

The EWM (Exponentially Weighted Moving Average) function is an important tool in time series analysis and forecasting. It allows us to calculate a weighted average of a series of data points, with more recent observations having a higher weight and older observations having a lower weight. This makes it particularly useful for capturing trends and patterns in data that might otherwise be obscured by noise or fluctuations.

One of the key benefits of the EWM function is its ability to assign different weights to different data points, depending on their relative importance. This means that we can give more weight to recent data points that are more likely to be relevant and representative of the current trend or behavior. By doing so, we can make more accurate predictions and forecasts.

The EWM function also helps to smooth out the data by reducing the impact of random variations or outliers. By assigning higher weights to recent data points, the function gives less importance to isolated or extreme values that might distort the overall trend. This makes it easier to identify and analyze underlying patterns or trends in the data.

Furthermore, the EWM function allows us to adjust the smoothing parameter, which controls the rate at which the weights decrease exponentially over time. By varying this parameter, we can adjust the responsiveness of the function to changes in the data. A smaller smoothing parameter gives more weight to recent data and makes the function more sensitive to short-term variations, while a larger smoothing parameter assigns more weight to older data and provides a smoother estimate of the underlying trend.

Read Also: 10 Steps to Start Investing Aggressively and Grow Your Wealth

In summary, the EWM function is an important tool for time series analysis and forecasting because it allows us to capture trends and patterns in data, reduce the impact of noise and outliers, and adjust the responsiveness of the function to changes in the data. It is a versatile and powerful function that can help us gain valuable insights and make accurate predictions in various domains.

| Advantages | Disadvantages |

|---|---|

| * Captures trends and patterns in data |

EWM stands for Exponentially Weighted Moving Average. It is a statistical method used to calculate the average of a time series dataset with exponentially decreasing weights.

You can calculate EWM in Python using the pandas library. The pandas library provides the ewm() function, which you can apply to a pandas DataFrame or Series to calculate the EWM.

The ewm() function in Python takes several parameters such as span, alpha, halflife, and com. These parameters allow you to customize the weight decay of the EWM calculation.

The main difference between EWM and a simple moving average (SMA) is that EWM gives more weight to recent data points, while SMA gives equal weight to all data points. EWM is more responsive to recent changes in the data, making it suitable for detecting trends or changes over time.

Yes, you can visualize the EWM in Python using libraries such as matplotlib or seaborn. These libraries allow you to plot the EWM along with the original data to visualize the trend or changes over time.

You can explore the EWM (Exponentially Weighted Moving) function in Python by using the pandas library. The pandas library provides a built-in function called ewm(), which allows you to perform exponential weighted moving average calculations on a given time series data. This function takes parameters such as span, decay, and alpha, which determine the weight assigned to each data point. By using the ewm() function, you can easily calculate the exponential weighted moving average of a time series in Python.

The EWM (Exponentially Weighted Moving) function in Python is used to calculate the exponentially weighted moving average of a time series. The exponentially weighted moving average is a popular method for smoothing time series data and is widely used in various fields such as finance, economics, and signal processing. By using the EWM function in Python, you can easily calculate the weighted average of a time series, which assigns more weight to recent data points and less weight to older data points. This helps to reduce noise and emphasize the trend in the data.

Is there any true 4K content? In the era of rapidly advancing technology, the term “4K” has become increasingly popular. It promises unparalleled …

Read Article

Players who have left the Kansas City Chiefs The Kansas City Chiefs, one of the most successful teams in the National Football League (NFL), have seen …

Read Article

Is RoboForex a Good Choice for Traders? RoboForex is a popular forex broker that has been providing financial services since 2009. With its wide range …

Read Article

How Trading Halts Impact Options When trading of securities is halted, it has significant implications for options traders. Options are derivative …

Read Article

How FPGA are Used in Trading Financial markets are fast-paced and highly competitive, where milliseconds can make all the difference. In this …

Read Article

What is BCA Swift code? If you have ever made an international bank transfer, you may have come across the term “Swift Code.” Swift Code, also known …

Read Article