Understanding tax deductions for moving expenses in New Jersey

Are moving expenses tax deductible in New Jersey? Moving can be a stressful and expensive process, and one of the ways to alleviate some of the …

Read Article

In the world of securities regulation, Section 16 of the Securities Exchange Act of 1934 is a critical component. This section governs the reporting and liability requirements for insiders who have access to nonpublic information about publicly traded companies.

However, not all transactions conducted by insiders fall under the purview of Section 16. There are a number of exemptions in place that allow certain transactions to be exempted from reporting and liability requirements.

One such exemption is the “technical nonpublic” exemption, which applies when an insider trades in securities that are not listed on a national securities exchange. In these cases, the transactions are not considered to be material, and therefore fall outside the scope of Section 16.

Another exemption is the “private transaction” exemption, which applies when an insider engages in a transaction with another person that is not subject to the reporting and liability requirements of Section 16. This exemption is often used in situations where the insider is selling securities in a private placement or to a family member.

Understanding these exemptions is crucial for insiders and their legal advisors to ensure compliance with securities regulations. By knowing which transactions are exempt from Section 16, insiders can confidently navigate the complexities of securities law while also protecting their interests.

Section 16 of the Securities Exchange Act of 1934 requires individuals who are directors, officers, or beneficial owners of more than 10% of a registered class of equity securities to report their transactions in those securities to the Securities and Exchange Commission (SEC). However, there are certain exemptions and exceptions that may apply to these individuals, allowing them to avoid certain reporting requirements under Section 16.

One exemption from Section 16 reporting is the “ordinary business transactions” exemption. This exemption allows individuals to avoid reporting transactions that are made in the ordinary course of business and not intended to evade the provisions of Section 16.

Another exemption is the “gift or inheritance” exemption. Under this exemption, individuals are not required to report transactions in securities that are acquired through a gift or inheritance. However, if the individual subsequently sells or transfers these securities, they may be subject to reporting requirements.

Section 16 also includes an exemption for transactions involving employee benefit plans. This exemption applies to transactions made by individuals in connection with employee benefit plans, such as employee stock purchase plans or stock option plans. These transactions are exempt from Section 16 reporting, as long as they are made in accordance with the terms of the plan and not for the purpose of avoiding reporting requirements.

In addition, there are exemptions for transactions made by non-residents and transactions involving certain types of securities, such as options and warrants. These exemptions recognize that certain types of transactions may not have the same impact as other transactions and, therefore, may not need to be reported under Section 16.

It is important for individuals who may be subject to Section 16 reporting requirements to be aware of these exemptions and exceptions. By understanding which transactions are exempt, individuals can avoid unnecessary reporting and potential penalties for non-compliance. Consulting with legal counsel or seeking guidance from the SEC can help ensure compliance with Section 16 requirements.

Read Also: Learn How to Identify Support and Resistance in Forex Trading

Section 16 of the law specifies certain transactions that are exempt from its requirements. These exemptions include:

1. Gifts and charitable contributions: Transactions that involve the transfer of securities as a gift or charitable contribution are exempt from the reporting obligations under Section 16. However, it is important to note that the recipient of such securities may still need to report their ownership and other relevant information.

2. Involuntary transactions: Transactions that are the result of a merger, acquisition, or other corporate reorganization are considered involuntary transactions and are exempt from Section 16 requirements. This exemption ensures that individuals are not penalized for transactions that are beyond their control.

3. Securities acquired through exercise of stock options: When securities are acquired through the exercise of stock options, they are exempt from the reporting requirements of Section 16. This exemption recognizes that such transactions are a common practice among employees and executives and should not be subject to additional reporting obligations.

Read Also: Factors that Correlate with the Euro (EUR)

4. Certain transactions by non-executive officers and directors: Non-executive officers and directors are subject to different reporting requirements under Section 16. Certain transactions by these individuals, such as the acquisition or disposition of securities, are exempt from the reporting obligations that apply to executive officers.

5. Transactions pursuant to dividend or interest reinvestment plans: Transactions made as a result of a dividend or interest reinvestment plan, where the securities are acquired as a result of the reinvestment of dividends or interest payments, are exempt from Section 16 requirements. These transactions are typically automatic and do not involve the exercise of discretion by the individual.

6. Transactions made under employee benefit plans: Transactions made under employee benefit plans, such as retirement plans or stock purchase plans, are generally exempt from the reporting requirements of Section 16. This exemption recognizes that these transactions are made as part of an employee’s compensation and are not indicative of improper trading activity.

It is important for individuals to familiarize themselves with the specific exemptions provided under Section 16 and to consult legal advice if there is uncertainty about whether a transaction is exempt or subject to reporting requirements.

Section 16 is a provision of the Securities Exchange Act of 1934 that requires certain individuals or entities that own more than 10% of a company’s stock to file regular reports with the Securities and Exchange Commission (SEC) detailing their transactions in that stock.

No, not all transactions are covered by Section 16. There are certain exemptions that allow individuals or entities to be exempt from the reporting requirements.

Some of the exemptions from Section 16 include transactions that are made pursuant to an employee benefit plan, transfers between immediate family members, certain acquisitions resulting from a merger or acquisition, and acquisitions made in open market transactions.

Exemptions from Section 16 are provided to avoid unnecessary regulatory burdens on certain transactions that do not pose a threat to the integrity of the securities markets. They recognize certain common-sense situations where reporting requirements may not be necessary.

Determining if a transaction is exempt from Section 16 can be complex, as it requires a thorough understanding of the different exemptions and the specific circumstances of the transaction. Consulting with a securities lawyer or compliance professional is recommended to ensure compliance with the law.

Section 16 of the Securities Exchange Act of 1934 covers the reporting and liability requirements for insiders who buy or sell securities of a publicly traded company. It requires insiders to disclose their transactions to the Securities and Exchange Commission (SEC) and imposes liability for certain transactions.

Are moving expenses tax deductible in New Jersey? Moving can be a stressful and expensive process, and one of the ways to alleviate some of the …

Read Article

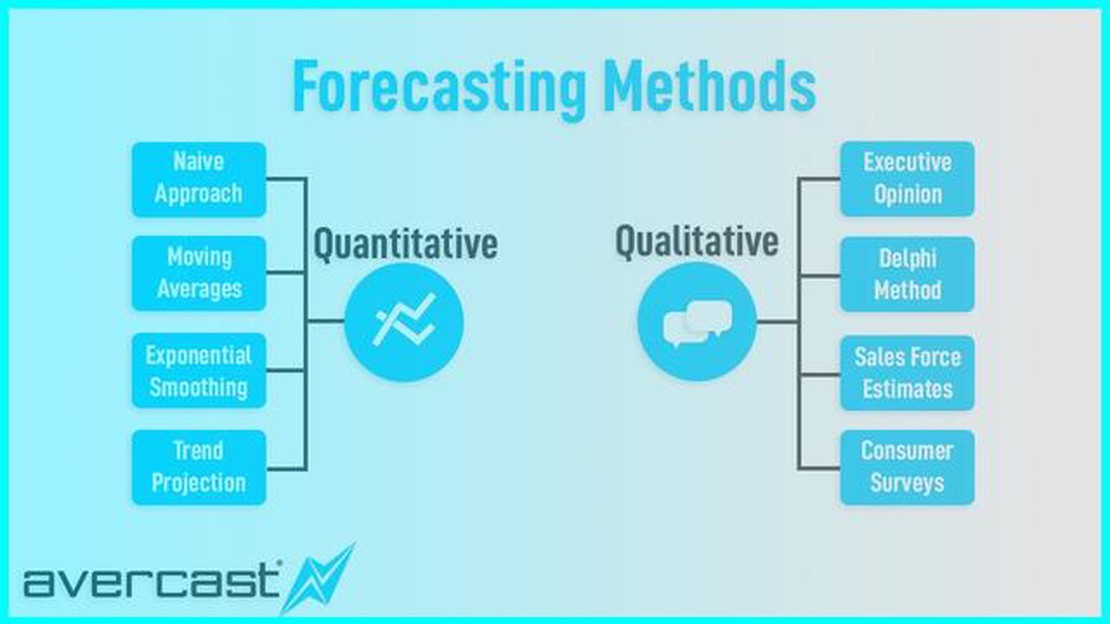

Methods for Sales Forecasting Accurate sales forecasting and revenue prediction are crucial for the success of any business. Properly anticipating …

Read Article

How to Calculate Pips in Forex PDF Are you new to forex trading and unsure how to calculate pips? Don’t worry, our comprehensive PDF guide will walk …

Read Article

How to Join the Exchange Student Program Welcome to our step-by-step guide on how to join the exchange student program! Studying abroad can be an …

Read Article

Choosing the Most Accurate EA for MT4 In the competitive world of forex trading, having the right tools can make all the difference. One of the most …

Read Article

Understanding the Foreign Exchange Market in Nigeria Nigeria, often referred to as the “Giant of Africa”, is not only the largest economy on the …

Read Article