Discover the Forex Session with the Highest Trading Volume

Which Forex Session Has the Most Volume? Forex, also known as foreign exchange, is the largest and most liquid financial market in the world. It …

Read Article

In the world of data analysis and forecasting, two popular techniques stand out: weighted moving average and exponential smoothing. While both methods aim to predict future data points, they differ in their approach and calculations.

Weighted moving average is a technique that assigns different weights to each data point in a time series based on their importance. The weights determine the contribution of each data point to the final average. This method is often used when there is a need to give more significance to recent data points compared to older ones.

Exponential smoothing, on the other hand, is a technique that emphasizes recent data points more than older ones. It uses a constant smoothing factor, also known as the decay factor, to decrease the weights of older data points exponentially. This method is particularly useful when there is a need to react quickly to changes in the data and when recent trends are more important than historical patterns.

In terms of calculation, weighted moving average requires the determination of weights for each data point. These weights can be determined based on subjective information or statistical techniques. The data points are then multiplied by their corresponding weights, and the weighted values are summed up and divided by the sum of the weights to obtain the final weighted moving average.

Exponential smoothing involves a recursive calculation that starts with an initial level and trend. It then adjusts these values based on the difference between the predicted and actual values. The smoothing factor determines the extent to which the latest data point affects the forecasted value. The exponential smoothing equation updates the forecast by taking into account the previous forecasted value and the difference between the predicted and actual values.

Weighted moving average and exponential smoothing have their own strengths and weaknesses. Weighted moving average is relatively simple to understand and implement but may not capture abrupt changes or seasonality in the data. On the other hand, exponential smoothing considers recent trends but may be less intuitive and may require more complex calculations.

In summary, both weighted moving average and exponential smoothing are valuable tools in data analysis and forecasting. The choice between the two depends on the specific requirements of the problem at hand and the nature of the data being analyzed. Understanding the differences between these methods allows analysts to make informed decisions and produce more accurate forecasts.

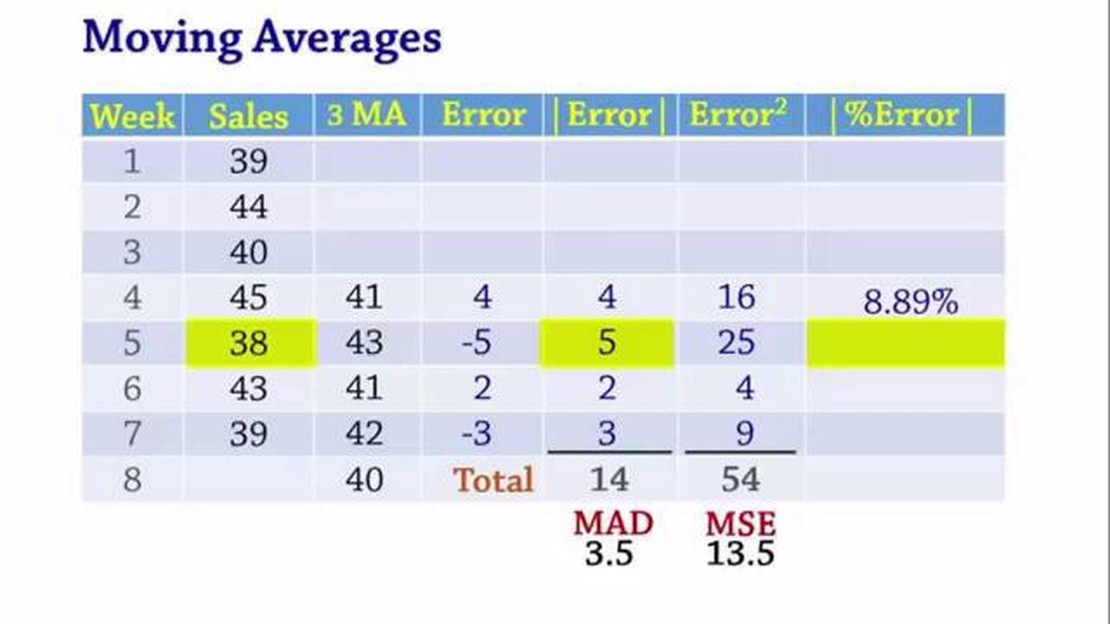

Weighted Moving Average (WMA) is a forecasting method that is widely used in finance and economics. It is a simple but effective technique for smoothing out data and identifying trends. WMA assigns different weights to different data points based on their importance or significance.

The concept behind WMA is to give more weight to recent data points and less weight to older ones. The purpose of this weighting is to emphasize the most recent information and minimize the impact of outliers or random fluctuations in the data.

To calculate the WMA, you multiply each data point by a weight factor and then sum them up. The weight factors are typically assigned based on a predefined formula or criteria. A commonly used method is to give higher weights to more recent data points and lower weights to older ones. The sum of the weights is usually equal to one.

Read Also: Comparing RSI and stochastic: Which technical indicator is more effective?

Using WMA can provide a smoother forecast compared to other averaging techniques, such as simple moving average. It helps in detecting trends and identifying underlying patterns in the data. However, it is important to choose the appropriate weighting factors for your specific situation, as they can greatly influence the results.

Advantages of Weighted Moving Average:

Example:

Suppose you want to forecast the sales of a product based on historical data. You could use WMA to give more weight to recent sales figures and less weight to older ones. This would help you in predicting future sales more accurately and making informed decisions.

Read Also: Understanding the Stock Option Collar Strategy: A Comprehensive Guide

Exponential smoothing is a statistical method used in time series forecasting to predict future values based on historical data. Unlike weighted moving average, which assigns different weights to each data point, exponential smoothing gives more weight to recent observations and less weight to older ones. This makes it particularly useful for forecasting in situations where the most recent data is a better indicator of future trends.

One key difference between exponential smoothing and weighted moving average is the way in which the weights are assigned. In weighted moving average, the weights are typically assigned in a linear or uniform manner. On the other hand, exponential smoothing assigns weights exponentially, with the most recent observations having the highest weight and the importance of older observations diminishing over time.

Another difference is the level of complexity. Exponential smoothing is generally considered to be a simpler and more intuitive method compared to weighted moving average. While weighted moving average requires the determination of appropriate weights for each data point, exponential smoothing only requires the selection of a smoothing factor or coefficient. This means that exponential smoothing can often be easier to implement and interpret.

Additionally, exponential smoothing allows for the inclusion of trend and seasonality components in the forecast. By using suitable variations of the method, such as Holt’s linear trend or Holt-Winters’ method, it is possible to incorporate trend and seasonality factors into the forecast. This can be beneficial in situations where the data exhibits a clear trend or seasonal patterns.

Overall, exponential smoothing and weighted moving average are both effective methods for time series forecasting, but they differ in terms of the weight assignment approach and the complexity of implementation. Depending on the specific requirements and characteristics of the data, one method may be more suitable than the other. It is important for forecasters to understand the strengths and limitations of each method in order to make informed decisions when selecting the most appropriate technique for their forecasting needs.

Weighted moving average is a forecasting method that assigns different weights to historical data points based on their significance.

Exponential smoothing differs from weighted moving average in that it assigns exponentially decreasing weights to historical data points, placing more emphasis on recent data.

The choice between weighted moving average and exponential smoothing depends on the specific needs and characteristics of the data being analyzed. Weighted moving average may be more appropriate when more weight should be given to certain data points, while exponential smoothing may be better at capturing short-term trends.

Yes, weighted moving average and exponential smoothing can be used together in certain forecasting models. For example, a hybrid approach may involve using exponential smoothing to capture short-term trends and weighted moving average to give more weight to specific data points.

Which Forex Session Has the Most Volume? Forex, also known as foreign exchange, is the largest and most liquid financial market in the world. It …

Read Article

Is China a $20 trillion dollar economy? China has long been regarded as one of the world’s fastest-growing economies, but is it really worth $20 …

Read Article

Creating a Comprehensive Employee Stock Option Plan: Best Practices and Structure+ Employee stock option plans are a valuable tool for companies to …

Read Article

ISO Stock Option: A Detailed Example and Explanation ISO stock options, also known as incentive stock options, are a type of employee stock option …

Read Article

What is the best single moving average? In the world of technical analysis, moving averages are widely used to identify trends and generate trading …

Read Article

Challenges in Pricing Options: Exploring the Complexity Option pricing is a crucial aspect of financial markets. It enables investors to determine the …

Read Article