Exploring the Wealth of Rogue Traders: From Small-Time Hustlers to Mega-Fortunes

How much money do rogue traders earn? Rogue traders have long fascinated and captivated both the general public and financial experts alike. These …

Read Article

The Vanna-Volga method is a popular approach used to price and hedge options in the foreign exchange (FX) market. Developed by Nassim Taleb and Dominique Carreau in the late 1990s, this method provides a reliable framework for estimating the fair value of options, taking into account market volatility and the relationship between the option’s delta, vega, and vanna.

The Vanna-Volga pricing methodology is based on the principle that options prices are determined not only by their delta and vega, but also by the vanna, which measures the sensitivity of the option’s delta to changes in implied volatility. By incorporating this additional greek, the Vanna-Volga method aims to provide more accurate pricing estimates compared to traditional models.

In this comprehensive guide, we will delve into the intricacies of Vanna-Volga option pricing, exploring the key concepts, assumptions, and calculations involved. We will discuss the role of vega risk, the significance of vanna, and how to implement the Vanna-Volga approach in practice. Whether you are a seasoned options trader or a newcomer to the field, this guide will equip you with the knowledge and tools to understand and apply Vanna-Volga option pricing effectively.

“The Vanna-Volga method offers a robust framework for estimating the fair value of options, taking into account the complex interplay between delta, vega, and vanna.” - Nassim Taleb and Dominique Carreau

Vanna-Volga option pricing is a method used to price vanilla options in the foreign exchange market. It combines two concepts: vanna and volga.

Vanna measures the sensitivity of the option’s delta to changes in the spot rate. It represents the risk of changes in the option’s value due to a movement in the underlying asset.

Volga, on the other hand, measures the sensitivity of the option’s vega to changes in volatility. It represents the risk of changes in the option’s value due to changes in the market’s expectation of future volatility.

The Vanna-Volga model estimates the fair price of a vanilla option by adjusting the Black-Scholes formula to account for vanna and volga risks. It assumes that the option’s delta and vega are constant, meaning that the option is sufficiently hedged against changes in the spot rate and volatility. This simplification allows for a straightforward calculation of the option’s price using a combination of spot rates and implied volatilities at different strikes.

The Vanna-Volga model is widely used in the foreign exchange market, where vanilla options are extensively traded. It provides a more accurate pricing approach than the traditional Black-Scholes model, which assumes constant delta and vega. By incorporating vanna and volga risks into the pricing calculation, the Vanna-Volga model offers a better reflection of the market reality and improves the accuracy of option valuations.

To implement the Vanna-Volga model, traders use a combination of spot rates and implied volatilities obtained from the market. These input parameters allow for the estimation of the option’s fair price, which can be used for trading decisions, risk management, and hedging strategies.

In conclusion, Vanna-Volga option pricing is a valuable tool for accurately pricing vanilla options in the foreign exchange market. It incorporates vanna and volga risks into the pricing calculation and provides a more realistic representation of option valuations. Traders can utilize this model to make informed trading decisions and manage their risk effectively.

Vanna-Volga option pricing is a widely used methodology in the financial industry for valuing and hedging options. It provides a comprehensive approach to pricing options that takes into account the risks associated with changes in the underlying asset price, the volatility of that price, and the volatility skew.

The Vanna-Volga method is particularly important in the foreign exchange market, where options on currency pairs are frequently traded. These options are often used by corporations and financial institutions to hedge their exposure to currency risk.

By accurately pricing options using the Vanna-Volga method, market participants can ensure that they are fairly compensated for the risks they are taking. This is crucial for maintaining a well-functioning market and for ensuring the stability of financial institutions.

Read Also: Understanding Risk Overlay: Definition, Benefits, and Implementation

Furthermore, the Vanna-Volga method allows market makers and traders to determine appropriate hedging strategies. By understanding the sensitivities of option prices to changes in the underlying asset price, volatility, and skew, market participants can hedge their positions effectively and reduce their risk exposure.

Without accurate option pricing models like Vanna-Volga, market participants would be unable to accurately value options and hedge their positions, leading to increased uncertainty and potential losses. The Vanna-Volga method provides a robust and reliable framework for pricing options and managing risk in the financial markets.

Read Also: Understanding CPC in Banking: What Does CPC Stand for and Why Is It Important?

| Benefits of Vanna-Volga Option Pricing |

|---|

| Accurate pricing of options |

| Improved risk management |

| Effective hedging strategies |

| Enhanced market stability |

1. Implied Volatility: Implied volatility is a crucial factor in Vanna-Volga option pricing. It represents the market’s expectation of future price fluctuations and is an input used to calculate option prices. Higher implied volatility leads to higher option prices, while lower implied volatility leads to lower option prices.

2. Spot Price: The spot price of the underlying asset is another important factor in Vanna-Volga option pricing. The spot price refers to the current market price of the asset. An increase in the spot price leads to higher call option prices and lower put option prices, while a decrease in the spot price has the opposite effect.

3. Strike Price: The strike price, also known as the exercise price, is the price at which the underlying asset can be bought or sold. It plays a significant role in Vanna-Volga option pricing. In general, call options with lower strike prices have higher prices than those with higher strike prices. Conversely, put options with higher strike prices have higher prices than those with lower strike prices.

4. Time to Expiration: The time to expiration is the remaining time until an option contract expires. It directly affects option prices in Vanna-Volga option pricing. Longer time to expiration leads to higher option prices, while shorter time to expiration results in lower option prices.

5. Risk-Free Interest Rate: The risk-free interest rate is the rate at which an investor can borrow or lend money without any risk of default. It is an essential factor in Vanna-Volga option pricing. Higher risk-free interest rates lead to higher call option prices and lower put option prices, while lower risk-free interest rates have the opposite effect.

6. Dividend Yield: The dividend yield is the dividend per share divided by the price per share of the underlying asset. It affects option prices in Vanna-Volga option pricing. Higher dividend yields result in lower call option prices and higher put option prices, while lower dividend yields lead to higher call option prices and lower put option prices.

Understanding these key factors is crucial for accurately pricing options using the Vanna-Volga model. Traders and investors can use this insight to make informed decisions and manage their options portfolios effectively.

Vanna-Volga option pricing is a method used to price and hedge exotic options, which are options with complex features or payoffs that differ from standard options.

Vanna-Volga option pricing incorporates the risk factors of the options market, such as the volatility smile and the risk reversal, into the pricing model. Traditional models, such as the Black-Scholes model, assume constant volatility and do not account for these factors.

The Vanna risk factor represents the sensitivity of the option’s delta to changes in the underlying spot price. It measures the change in the option’s delta for a given change in the spot price.

The Vanna risk factor is used to adjust the prices of the hedging instruments, such as options and spot positions, in order to accurately hedge the exotic option. By accounting for the Vanna risk factor, the Vanna-Volga model provides a more accurate pricing and hedging framework.

Yes, there are limitations to Vanna-Volga option pricing. The model assumes that the volatility smile and risk reversal are constant over time, which may not hold true in all market conditions. Additionally, the model does not account for jumps in the underlying spot price, which could impact the pricing and hedging accuracy.

How much money do rogue traders earn? Rogue traders have long fascinated and captivated both the general public and financial experts alike. These …

Read Article

Is FBS compatible with MT4? If you are interested in trading forex and other financial instruments, you have probably heard of MetaTrader 4 (MT4), one …

Read Article

Understanding the Process of Closing a Stock Option Closing a stock option is an essential step in the world of investing. It refers to the act of …

Read Article

Best Forex Trading Platforms in Malaysia Forex trading has grown in popularity in Malaysia, with more and more individuals looking to invest in this …

Read Article

Top providers of paper trading Practicing trading is a crucial step for anyone looking to enter the financial markets. However, it can be daunting to …

Read Article

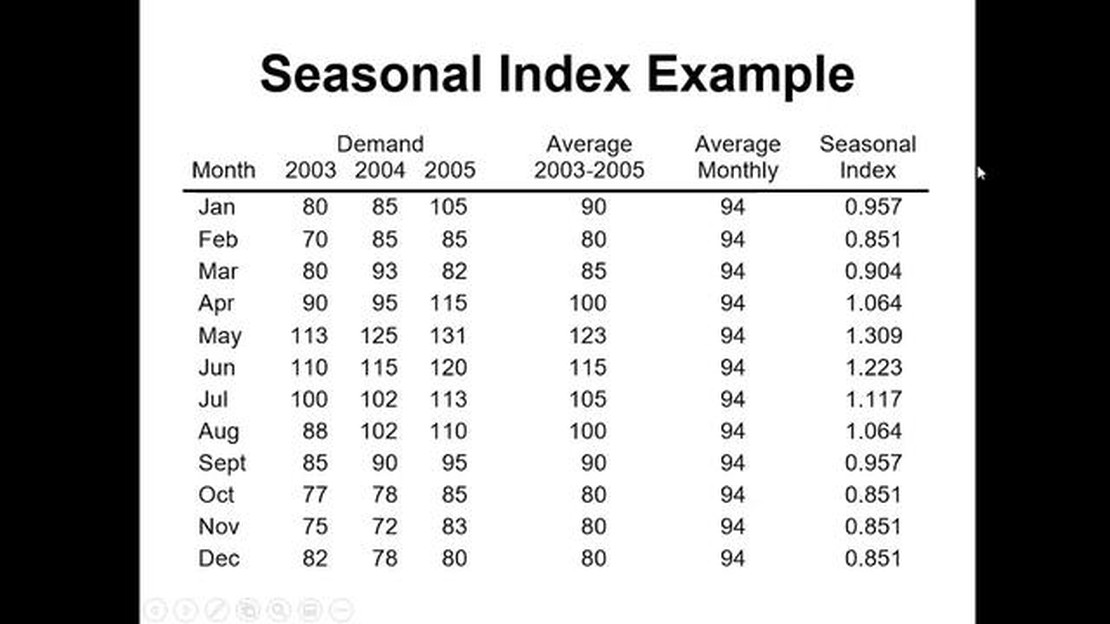

Understanding the Importance of Seasonal Index Calculation Calculating seasonal indexes is a vital aspect in understanding and analyzing trends in …

Read Article