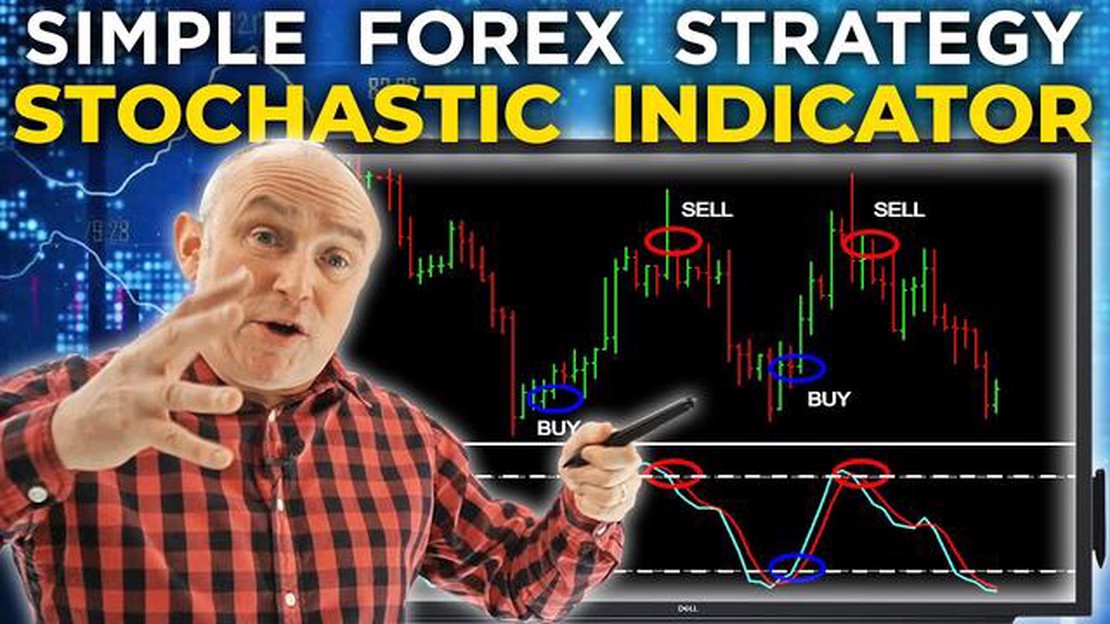

Understanding the Stochastic Strategy in Forex Trading: A Comprehensive Guide

Understanding the Stochastic Strategy in Forex Trading When it comes to forex trading, having a reliable strategy is crucial for success. One popular …

Read Article

In signal processing, the Exponentially Weighted Moving Average (EWMA) filter is a commonly used method for smoothing time-series data. It is a type of low-pass filter that reduces noise and random variations in the data, while preserving the overall trend and important features.

The EWMA filter calculates the weighted average of the previous data points, with exponentially decreasing weights as the data points get older. This means that recent data points have more influence on the smoothed result, while older data points have less influence. The choice of weight decay factor determines the balance between responsiveness to recent changes and stability against noise.

One of the main advantages of the EWMA filter is its simplicity and ease of implementation. It does not require a large amount of memory or computational resources, making it suitable for real-time applications and embedded systems. Additionally, it can be easily adjusted to different time scales by changing the value of the weight decay factor.

The EWMA filter has a wide range of applications in various fields, including finance, engineering, and healthcare. For example, it can be used to smooth financial market data to identify trends and make predictions, to filter noise from sensor measurements in engineering systems, or to analyze patient vital signs in medical monitoring devices.

In conclusion, the Exponentially Weighted Moving Average (EWMA) filter is a simple yet powerful tool for smoothing time-series data. Its ability to reduce noise while preserving important features makes it valuable in a wide range of applications. Understanding the principles and characteristics of the EWMA filter can help improve data analysis and decision-making processes in many domains.

The Exponentially Weighted Moving Average (EWMA) filter is a method used to smooth or reduce noise in a time series data. It is commonly used in finance, signal processing, and other fields where data analysis is required.

The EWMA filter works by giving more weight to recent data points and gradually decreasing the weight of older data points. This is done using an exponential decay function, where the weight of each data point decreases exponentially as it gets older.

The EWMA filter is often used to calculate the moving average of a time series data, where the average is calculated over a specific window of time. The window size can be adjusted based on the desired level of smoothing.

One of the main advantages of the EWMA filter is its ability to react quickly to changes in the data. Since more weight is given to recent data points, the filter can quickly adapt to new trends or patterns in the data.

Another advantage is that the EWMA filter does not require storing all the data points in memory. It only needs to store the most recent data point and the current value of the filter output, making it more memory-efficient compared to other types of filters.

Read Also: Understanding the FTSE MIB 40 Index: Everything You Need to Know

Overall, the EWMA filter is a simple yet effective method for smoothing time series data. It provides a good balance between responsiveness to changes and reducing noise in the data, making it a popular choice in various fields of data analysis and signal processing.

The Exponentially Weighted Moving Average (EWMA) filter is a useful tool in various fields and industries. Here are a few reasons why the EWMA filter is widely used:

In conclusion, the EWMA filter is a versatile tool that offers a range of benefits in smoothing, trend identification, forecasting, real-time data analysis, and risk management. Its ability to reduce noise, capture trends, and adapt to changing data characteristics makes it a valuable asset in many applications.

The Exponentially Weighted Moving Average (EWMA) filter is a commonly used mathematical method for smoothing data or time series. It provides a weighted average of the past observations, with more recent observations receiving higher weights. This makes the EWMA filter particularly useful for reducing noise and identifying underlying trends or patterns in the data.

Read Also: What is the new price target for Ford stock? | Latest updates and forecasts

At its core, the EWMA filter assigns exponentially decreasing weights to each observation, based on its recency. The weights are determined by a smoothing factor, often denoted as α (alpha), which lies between 0 and 1. A smaller α value gives more weight to older observations, whereas a larger α value gives more weight to recent observations.

The calculation of the EWMA filter involves three main steps:

The effectiveness of the EWMA filter depends on the choice of the smoothing factor α. A low α value results in a smoother filter output with a longer memory of past observations, while a high α value leads to a more responsive filter that quickly adapts to changes in the data.

The EWMA filter is widely used in various applications, including finance, engineering, and signal processing. It is particularly valuable for analyzing noisy or volatile data, as it helps extract the underlying trends and patterns that may be hidden in the raw observations.

In summary, the EWMA filter works by assigning exponentially decreasing weights to past observations, based on their recency. It provides a smoothed version of the data, helping to reduce noise and identify underlying trends. The filter’s performance can be adjusted by choosing an appropriate smoothing factor α.

A Moving Average Filter is a method used in signal processing to remove noise from a signal by averaging the values over a certain time window.

The main difference is in how the averages are calculated. A SMA takes the average of a fixed number of data points over a specified time period, while an EWMA assigns weights to the data points, with more recent data having higher weights. This allows an EWMA to react more quickly to changes in the data.

An EWMA filter can be used in finance to analyze time series data, such as stock prices or market returns. It can help to smooth out noisy data, identify trends, and detect changes in volatility. This can be useful in making trading decisions and risk management strategies.

In an EWMA filter, the weights are assigned using a decay factor that determines the rate at which the weights decrease exponentially. The decay factor is usually chosen based on the desired responsiveness of the filter. A higher decay factor will place more emphasis on recent data, while a lower decay factor will give more weight to older data.

Understanding the Stochastic Strategy in Forex Trading When it comes to forex trading, having a reliable strategy is crucial for success. One popular …

Read Article

Does Pfizer Pay Monthly Dividends? If you are a shareholder or are considering investing in Pfizer, you may be wondering whether the company pays …

Read Article

Exploring the 3 Efficiency Ratios for Effective Financial Analysis Efficiency ratios are important tools for financial analysis that can help assess a …

Read Article

Thunder Waived Players: Who Got Cut? The Oklahoma City Thunder have recently made some significant roster moves by waiving several players. These …

Read Article

What is the most accurate indicator for intraday? When it comes to intraday trading, having the right indicator is crucial. Intraday traders rely on …

Read Article

Discover How Many Days the 30-Week Moving Average Lasts A moving average is a popular technical analysis tool used by traders and investors to …

Read Article