Exploring Gold Market Analysis: Tips and Techniques

Analyzing the Gold Market: A Comprehensive Guide Gold market analysis is a crucial skill for investors and traders looking to navigate the complex …

Read Article

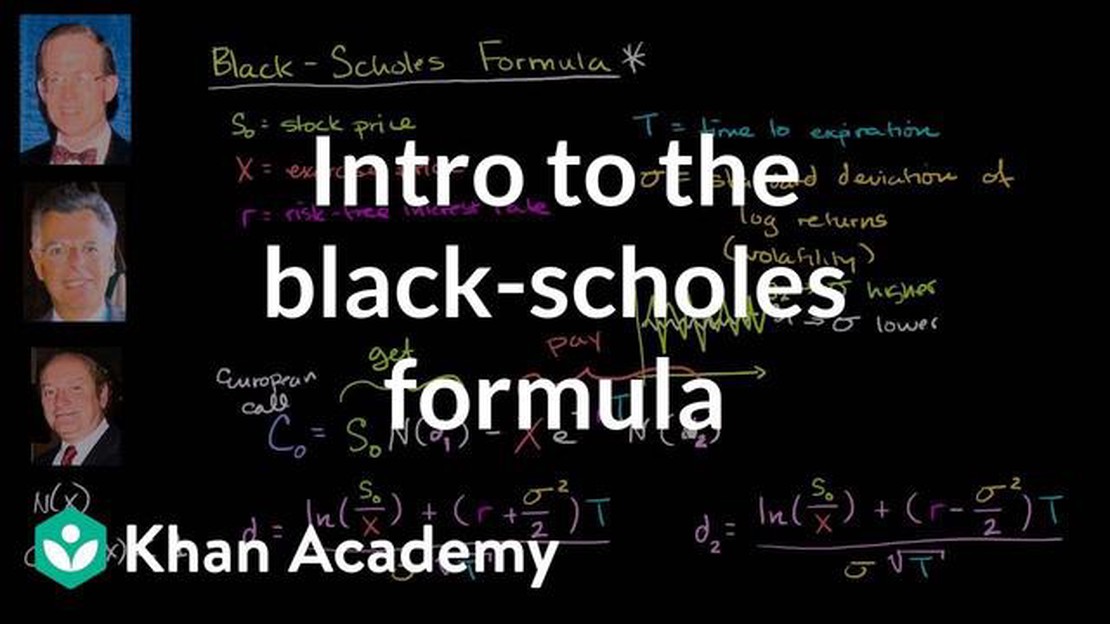

Options are a popular financial instrument that allows investors to profit from the movement of underlying assets without actually owning them. However, understanding options pricing can be complex. Luckily, the Black-Scholes model provides a comprehensive framework for valuing options and understanding their underlying dynamics.

The Black-Scholes model, developed by economists Fisher Black and Myron Scholes in 1973, revolutionized options pricing. It is based on the assumption that financial markets are efficient and that the price of an underlying asset follows a random walk. The model takes into account various factors, such as the current price of the underlying asset, the strike price, the time remaining until expiration, the volatility of the underlying asset, and the risk-free interest rate.

Using the Black-Scholes model, investors can calculate the fair value of an option and determine whether it is overpriced or underpriced in the market. The model provides formulas to calculate the value of both European options (which can only be exercised at expiration) and American options (which can be exercised at any time until expiration).

However, it’s important to note that the Black-Scholes model has its limitations. It assumes constant volatility, which may not always reflect the realities of the market. Additionally, the model assumes that the underlying asset follows a log-normal distribution, which may not accurately capture extreme market events.

In conclusion, understanding options pricing is crucial for investors looking to profit from the movement of underlying assets. The Black-Scholes model provides a comprehensive framework for valuing options and understanding their underlying dynamics. While the model has its limitations, it remains a valuable tool for investors in the world of options trading.

Options are financial instruments that give investors the right, but not the obligation, to buy or sell an underlying asset at a predetermined price within a specified time period. The underlying asset can be a stock, index, commodity, or currency.

Options can be classified into two types: calls and puts. A call option gives the holder the right to buy the underlying asset, while a put option gives the holder the right to sell the underlying asset.

When an investor buys an option, they pay a premium to the seller. The premium amount is determined by various factors, including the current price of the underlying asset, the strike price, the time until the option expires, and market volatility.

Options provide investors with the opportunity to profit from price movements in the underlying asset without actually owning it. For example, a call option can be used to profit from an expected increase in the price of the underlying asset, while a put option can be used to profit from an expected decrease in price.

Read Also: The Best Time Frame to Sell Puts: A Comprehensive Guide

Options can be used for speculative purposes, to hedge against potential losses, or to generate income through writing options. They are commonly traded on exchanges, and their prices are determined by supply and demand factors.

It’s important to note that options trading involves risk, and investors should carefully consider their risk tolerance and financial goals before trading options. It’s also recommended to have an understanding of the Black-Scholes model, which is commonly used to calculate the theoretical value of options.

Options are financial derivatives that provide investors with the opportunity to make strategic investments and manage risk. They can be used for a variety of purposes, but here are three key reasons why investors use options:

1. Speculation: Options allow investors to speculate on the direction of an underlying asset’s price movement without actually owning the asset itself. This allows for leveraged bets on the price of the asset, potentially leading to larger profits compared to investing in the asset directly. Investors can use options to profit from both rising and falling prices, depending on whether they buy call options (betting on a price increase) or put options (betting on a price decrease).

2. Hedging: Options offer a valuable tool for hedging against potential price fluctuations and reducing the impact of market volatility. Investors can use options to reduce their risk and protect their investments by buying or selling options contracts that provide the right to buy or sell the underlying asset at a predetermined price within a specific timeframe. By using options to hedge, investors can limit their downside risk while still maintaining the potential for upside gain.

3. Income Generation: Options can be used to generate income through a strategy called writing covered options. In this strategy, an investor who owns the underlying asset sells call options on that asset to generate additional income. If the price of the asset remains below the strike price of the call options, the options expire worthless, and the investor keeps the premium received from selling the options. This income generation strategy can be particularly attractive in sideways or declining markets.

Overall, options provide investors with flexibility and the ability to tailor their investment strategies to their specific goals and risk tolerance. Whether it is for speculation, hedging, or income generation, options can be a valuable tool in an investor’s arsenal.

The Black-Scholes model is a mathematical model used to calculate the theoretical price of financial options. It is based on several key principles that are essential for understanding and using the model effectively.

Read Also: Understanding additive models in time series analysis: a comprehensive guide

| 1. Risk-neutral valuation | The Black-Scholes model assumes that the financial markets are efficient and that there are no arbitrage opportunities. It uses risk-neutral valuation to calculate the option price based on the expected value of the option’s future payoffs. |

| 2. Continuous trading | The model assumes that trading in the underlying asset is continuous, meaning that there are no restrictions on when the asset can be bought or sold. This assumption allows for the use of continuous compounding in the calculation of the option price. |

| 3. Log-normal distribution | The model assumes that the underlying asset follows a log-normal distribution of prices, meaning that the asset’s price movements are normally distributed when observed over small time intervals. This assumption allows for the calculation of the probability of different future price levels. |

| 4. Constant volatility | The model assumes that the volatility of the underlying asset is constant over the life of the option. This assumption allows for the calculation of the option price using a single volatility value. |

| 5. No dividends | The model assumes that the underlying asset does not pay any dividends during the life of the option. This assumption simplifies the calculation of the option price, as there are no additional cash flows to consider. |

| 6. Risk-free interest rate | The model assumes that there is a risk-free interest rate that is constant over the life of the option. This assumption allows for the calculation of the present value of the expected future payoffs of the option. |

By understanding these key principles, traders and investors can use the Black-Scholes model to calculate the theoretical prices of options and make informed decisions about their trading strategies.

The Black-Scholes model is a mathematical model used to calculate the theoretical price of options. It takes into account various factors such as the stock price, strike price, time to expiration, risk-free rate, and volatility.

The Black-Scholes model is important because it provides a framework for pricing options and understanding how different factors affect their value. It is widely used by traders, investors, and financial institutions to determine fair prices and make informed decisions.

The Black-Scholes model calculates the fair value of options by using a formula that takes into account the current stock price, the strike price, the time to expiration, the risk-free rate, and the volatility of the underlying asset. It assumes that stock prices follow a log-normal distribution and that there are no transaction costs or taxes.

The Black-Scholes model is based on several assumptions, including that stock prices follow a log-normal distribution, there are no transaction costs or taxes, the risk-free rate is constant, and the market is efficient. These assumptions may not always hold in real-world scenarios, but the model still provides a useful framework for understanding options pricing.

The Black-Scholes model is a widely used and respected tool for options pricing, but it does have its limitations. It assumes a constant volatility and a log-normal distribution for stock prices, which may not always hold true. Additionally, the model does not take into account factors such as market liquidity and market impact, which can affect option prices. Traders and investors often use the model as a starting point and make adjustments based on market conditions and their own judgment.

The Black-Scholes model is a mathematical model used to calculate the price of options. It was developed by economists Fischer Black and Myron Scholes in the 1970s.

Analyzing the Gold Market: A Comprehensive Guide Gold market analysis is a crucial skill for investors and traders looking to navigate the complex …

Read Article

Can you negotiate a stock option? Stock options can be a valuable form of compensation, allowing employees to potentially reap significant financial …

Read Article

Is Forex trading fraud? Forex trading is a popular form of investment that has gained significant attention in recent years. However, with the rise in …

Read Article

The Best Strategy for Futures Trading in India Developing a winning futures trading strategy is crucial for traders looking to navigate the Indian …

Read Article

Understanding ADR in Trading When it comes to trading, it is crucial to understand the concept of ADR (Average Daily Range) and its significance. ADR …

Read Article

The Significance of Forex Management In the fast-paced world of foreign exchange trading, effective forex management is crucial for both individual …

Read Article