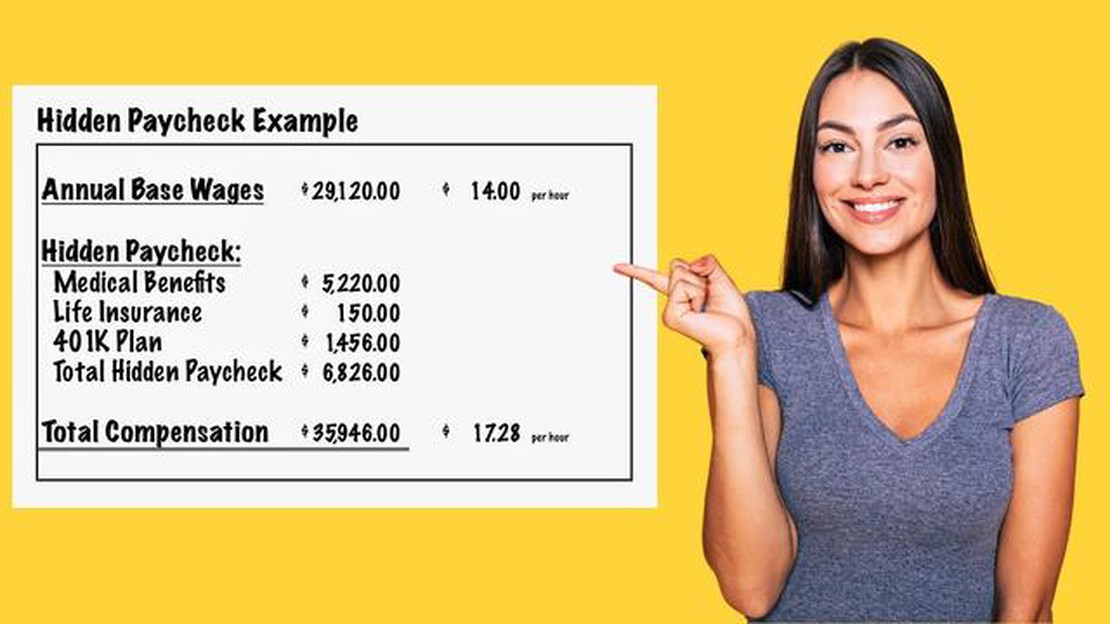

What is Total Compensation Cost? Understanding the Impact on Employee Benefits

What Is Total Compensation Cost? When considering employee benefits, it is crucial for organizations to understand the concept of total compensation …

Read Article

The Reserve Bank of India (RBI) plays a crucial role in regulating and supervising financial matters in the country, including forex trading. Forex trading refers to the buying and selling of different currencies with the aim of making profits. It is a popular form of investment, but it is subject to various rules and regulations imposed by the RBI to ensure the stability and security of the financial system.

One of the key guidelines set by the RBI is the prohibition of forex trading on a margin basis. This means that individuals or entities are not allowed to trade forex in India using borrowed money or leverage. The RBI aims to prevent excessive speculation and potential risks to the economy by discouraging leveraged trading. Therefore, traders must use their own funds for forex trading transactions.

Additionally, the RBI has imposed limits on the amount of foreign currency that individuals can acquire or sell. These limits are known as foreign exchange limits and individuals must adhere to them when engaging in forex trading. These limits aim to control the flow of foreign exchange, prevent money laundering, and ensure the stability of the Indian rupee.

Furthermore, the RBI requires forex trading transactions to be conducted through authorized dealers or banks. Individuals or entities cannot engage in forex trading with unauthorized entities or platforms. This measure is in place to protect traders from fraudulent activities and to ensure that transactions are conducted in a transparent and regulated environment.

In conclusion, understanding the RBI guidelines and regulations on forex trading is crucial for anyone wishing to engage in this form of investment. By following these guidelines, traders can ensure that they operate within the legal framework and contribute to the stability and security of the Indian financial system.

The Reserve Bank of India (RBI) plays a crucial role in regulating and supervising the foreign exchange market in India. The guidelines and regulations set by the RBI are aimed at ensuring the stability of the forex market and protecting the interests of investors and the economy as a whole.

One of the main objectives of the RBI guidelines on forex trading is to control and monitor the flow of foreign exchange in and out of the country. The RBI sets limits on the amount of foreign currency that can be traded by individuals and businesses, and also regulates the methods through which foreign currency can be acquired or remitted.

The RBI guidelines also aim to prevent money laundering and other illegal activities that may be associated with forex trading. The RBI mandates Know Your Customer (KYC) norms for all customers engaging in forex transactions, and requires banks and financial institutions to keep proper records of all forex transactions for a specified period of time.

In addition, the RBI guidelines cover areas such as risk management, leverage limits, and the conduct of market participants. The RBI sets guidelines for authorized dealers, banks, and other entities involved in forex trading to follow in order to maintain market integrity and avoid excessive risk taking.

Furthermore, the RBI guidelines also provide clarity on the eligibility criteria for individuals and businesses to engage in forex trading. The RBI lays down the requirements for obtaining a forex trading license or registering as a forex broker, and also specifies the qualifications and experience needed to be a forex trader.

Read Also: Are stock options considered assets? Find out here

Overall, the scope of RBI guidelines on forex trading is comprehensive and covers various aspects that are essential for the smooth functioning of the forex market in India. By following these guidelines, investors can ensure that their forex transactions comply with the regulations set by the RBI, thereby contributing to a more transparent and secure forex trading environment.

India has a strict regulatory environment when it comes to forex trading. The Reserve Bank of India (RBI) governs and regulates all foreign exchange transactions in the country.

Forex trading in India is mainly regulated under the Foreign Exchange Management Act (FEMA), which was introduced in 1999. The RBI is responsible for ensuring that all forex transactions comply with the FEMA guidelines.

One of the key regulations in India is that forex trading can only be done through authorized dealers or brokers. Individuals are not allowed to directly participate in the forex market. This is to prevent unauthorized foreign exchange trading and ensure the safety of investors.

Only a few selected currency pairs are allowed for trading in India. The RBI has specified a list of currencies that can be exchanged, and individuals are not allowed to trade other currencies. This is done to control the flow of foreign exchange and prevent speculation on certain currencies.

In order to participate in forex trading in India, individuals and businesses need to comply with certain requirements. They are required to have a valid bank account, known as an Authorized Dealer Category-I (AD Cat-I) account, with an authorized bank. This account is used for all forex transactions and ensures that the transactions are compliant with the RBI regulations.

Read Also: What time does the Sydney forex market open?

Additionally, individuals and businesses need to provide necessary documents and information, such as proof of identity and address, to the authorized dealer. This is a part of the know your customer (KYC) process and is mandatory for all forex traders in India.

The RBI also imposes restrictions on the amount of foreign exchange that can be bought or sold by individuals and businesses. These limits are periodically reviewed and revised by the RBI to suit the economic conditions of the country. It is important for forex traders to stay updated with the latest restrictions and guidelines to ensure compliance with the regulations.

Failure to comply with the forex trading regulations in India can result in penalties and legal consequences. The RBI is authorized to take strict actions against individuals or businesses that violate the regulations. Therefore, it is important for all forex traders in India to adhere to the guidelines and regulations set forth by the RBI.

In summary, forex trading in India is subject to strict regulations governed by the RBI. Individuals and businesses need to comply with the requirements, trade only authorized currency pairs, and engage with authorized dealers. It is crucial to stay updated with the latest regulations to ensure a smooth and legal forex trading experience in India.

RBI guidelines and regulations on Forex Trading are rules set by the Reserve Bank of India to govern the trading of foreign currencies in India. These guidelines are aimed at ensuring transparency, accountability, and stability in the forex market.

The purpose of RBI guidelines and regulations on Forex Trading is to protect the interests of individual investors, maintain the stability of the Indian financial system, and prevent the misuse of foreign exchange for illegal activities such as money laundering and terrorism financing.

The key features of RBI guidelines and regulations on Forex Trading include restrictions on the amount of foreign currency that can be bought or sold, requirement of KYC (Know Your Customer) documentation for all forex transactions, prohibition of forex trading on margin, and the need to trade through authorized dealers only.

The penalties for non-compliance with RBI guidelines and regulations on Forex Trading can range from monetary fines to imprisonment, depending on the severity of the violation. It is important for individuals and businesses to be aware of and adhere to these guidelines to avoid legal consequences.

What Is Total Compensation Cost? When considering employee benefits, it is crucial for organizations to understand the concept of total compensation …

Read Article

Are stock options taxed as a bonus? Stock options are a common form of incentive compensation offered by many companies to their employees. They …

Read Article

Italy: Country of the FTSE MIB Index The FTSE MIB Index is a market index that represents the performance of Italy’s major companies listed on the …

Read Article

Understanding the CAD JPY Quote and Its Significance When it comes to trading in the foreign exchange market, it’s essential to understand the …

Read Article

Where to Exchange Currency in Kuala Lumpur Kuala Lumpur, the capital city of Malaysia, is a vibrant metropolis known for its modern skyscrapers, rich …

Read Article

Forex Trading: Skill or Gambling? Forex trading has always been a topic of debate among investors and financial experts. Some argue that it is a …

Read Article