What is ESMA and its meaning explained

ESMA: Meaning, Functions, and Importance ESMA stands for the European Securities and Markets Authority. It is an independent EU authority that ensures …

Read Article

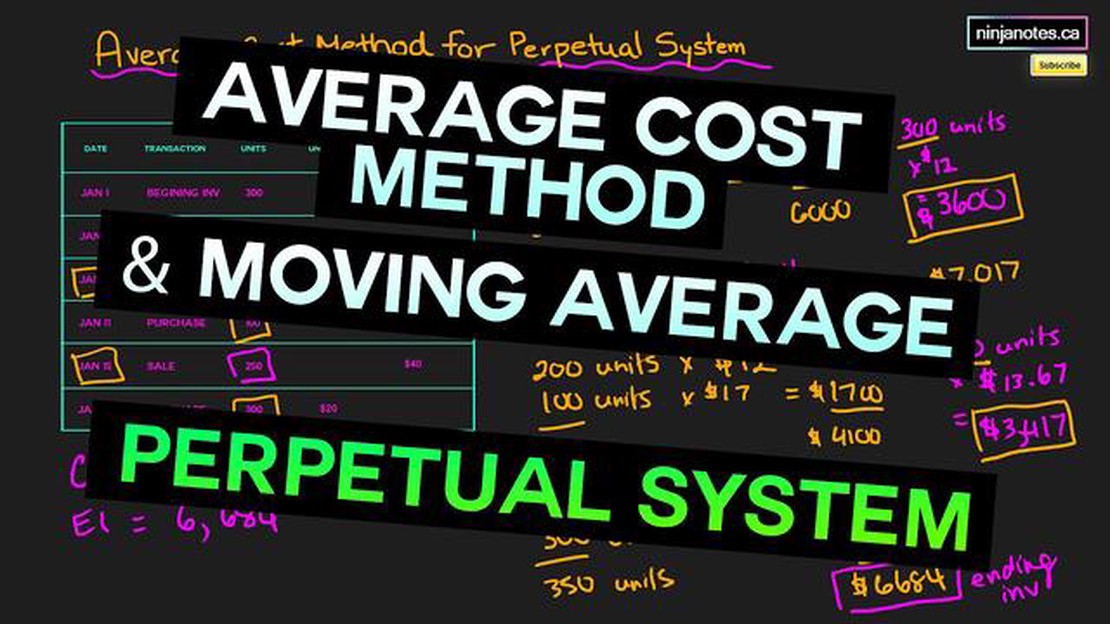

Inventory valuation is an essential aspect of accounting for any business that deals with physical products. It refers to the process of assigning a monetary value to the inventory on hand at a given point in time. There are various methods for inventory valuation, and one commonly used approach is the moving average method.

The moving average method calculates the average cost of the inventory by considering the cost of goods purchased or produced over a period of time. This period can be a week, a month, or any other suitable duration. The average cost is determined by dividing the total cost of inventory by the total quantity of units in stock.

By using the moving average method, a business can smooth out the fluctuations in the cost of inventory. This is especially useful in industries where the cost of raw materials or goods can vary significantly over time. The moving average method allows for a more accurate representation of the inventory value, eliminating the impact of sharp price changes.

It’s important to note that the moving average method is often used in conjunction with other inventory valuation methods, such as the first-in, first-out (FIFO) or last-in, first-out (LIFO) methods. Each method has its advantages and disadvantages, and businesses may choose the most appropriate one based on their specific needs and industry requirements.

Inventory valuation is the process of calculating the worth of a company’s inventory by assigning a monetary value to the goods or products that it has on hand. This valuation is important because it determines the value of the company’s assets and impacts various financial ratios and statements.

Inventory valuation is necessary for accurate financial reporting and decision-making. It helps businesses in determining their cost of goods sold (COGS), gross profit margins, and overall profitability. Additionally, it ensures that inventory levels are properly valued on the balance sheet.

Read Also: Is Binary Trading a Good Option for Beginners?

There are several methods that businesses can use to value their inventory, including the moving average method. This method calculates the average cost of each unit of inventory by dividing the total cost of goods available for sale by the total number of units. The moving average is then used to assign a value to the inventory on hand.

Inventory valuation affects the financial statements of a company. For example, it affects the balance sheet, where inventory value is reflected as an asset. It also affects the income statement through the calculation of COGS, which is deducted from revenue to determine gross profit. Lastly, it impacts the statement of cash flows by affecting the cash flows from operations.

| Advantages of Inventory Valuation | Disadvantages of Inventory Valuation |

|---|---|

| Provides an accurate measure of a company’s assets | Can be time-consuming and complex |

| Aids in better decision making | Inventory values may fluctuate based on market conditions |

| Ensures compliance with accounting standards | Requires regular monitoring and adjustments |

In conclusion, inventory valuation is a critical process for businesses as it determines the value of their inventory and impacts financial statements. It helps businesses make informed decisions, comply with accounting standards, and accurately report their financial position. By using methods like the moving average method, businesses can assign a value to their inventory that reflects its true worth.

Accurate inventory valuation is crucial for businesses to effectively manage their operations and make informed financial decisions. Inventory represents a significant investment for most companies, and its value directly impacts the financial statements.

Here are some key reasons why accurate inventory valuation is important:

| 1. Financial Reporting |

|---|

| Accurate inventory valuation is essential for preparing accurate financial statements. The value of inventory is included in the balance sheet as an asset and affects metrics such as gross profit and net income. If inventory is overvalued or undervalued, it can distort the financial picture and mislead investors and stakeholders. |

| 2. Cost of Goods Sold |

| Accurate inventory valuation is critical for calculating the cost of goods sold (COGS). COGS is a key component of the income statement and directly influences the gross profit. Incorrectly valuing inventory can lead to inaccurate COGS calculations and may result in misleading profitability metrics. |

| 3. Taxation |

| Inventory valuation also affects the tax liability of a company. Different valuation methods can have varying tax implications. For example, using the LIFO (Last-In, First-Out) method may result in lower taxable income in a period of rising prices, while using FIFO (First-In, First-Out) may result in higher taxable income. |

| 4. Decision Making |

| Accurate inventory valuation provides important information for decision-making processes. It helps management determine optimal pricing strategies, identify slow-moving or obsolete inventory, and plan for future purchases and production. Making decisions based on inaccurate inventory values can lead to financial losses and inefficiencies. |

| 5. Comparison and Analysis |

| Accurate inventory valuation enables meaningful comparisons and analysis. Companies can compare their inventory turnover ratios and other financial metrics with industry benchmarks or previous periods to assess their performance. Inaccurate inventory valuation can skew these comparisons and make it difficult to evaluate the company’s efficiency and profitability. |

In conclusion, accurate inventory valuation is vital for businesses to ensure accurate financial reporting, make informed decisions, and comply with taxation requirements. Employing appropriate valuation methods and regularly reviewing and updating inventory records can help maintain the accuracy of inventory valuation.

Read Also: Did Ally Financial acquire TradeKing?

Inventory valuation is the process of assigning a monetary value to the inventory a company has on hand. It is important for financial reporting purposes and can impact a company’s profitability.

The moving average method of inventory valuation is a technique used to calculate the average cost of inventory by considering the cost of each item purchased over a period of time. The average cost is then used to assign a value to the inventory.

The moving average is calculated by dividing the total cost of inventory by the total number of units in inventory. This provides the average cost per unit, which is then used to value the inventory.

The moving average method is often used for inventory valuation because it provides a more accurate representation of the cost of inventory over time. It smooths out fluctuations in purchase prices and can result in a more stable and consistent valuation of inventory.

ESMA: Meaning, Functions, and Importance ESMA stands for the European Securities and Markets Authority. It is an independent EU authority that ensures …

Read Article

Calculating Average with VBA: Step-by-Step Guide Calculating the average of a set of values is a common task in data analysis. Whether you’re working …

Read Article

How to Extract Stock Data from GOOGLEFINANCE When it comes to monitoring stock prices and analyzing market trends, having access to accurate and …

Read Article

4 Types of Forex Traders: Exploring Different Trading Styles When it comes to forex trading, everyone has their own unique approach. Some traders …

Read Article

Understanding UTP in Trading When it comes to trading, having a comprehensive understanding of UTP (Unlisted Trading Privileges) is essential. UTP is …

Read Article

What is the lowest rate of yen to MYR? Are you a forex trader looking to get the best rates for your trades? Look no further! Our expert forex …

Read Article