Understanding D3 Analysis: A Comprehensive Guide

Exploring D3 Analysis: A Comprehensive Overview D3 (Data-Driven Documents) is a JavaScript library that is widely used for creating dynamic and …

Read Article

Options trading can be complex and confusing, especially for beginners. However, two crucial concepts in options trading that every trader should understand are delta and theta. Delta and theta are Greek letters used to measure an option’s sensitivity to changes in the price of the underlying asset and the time decay of the option, respectively.

Delta: Delta measures the rate of change of an option’s price in relation to changes in the price of the underlying asset. It tells us how much an option’s price will change if the underlying asset price changes. A delta of 1 means that the option price will move in lockstep with the underlying asset’s price, while a delta of 0 means that the option price will not be affected by changes in the underlying asset’s price.

Theta: Theta measures how much an option will lose in value over time due to the passage of time alone. It quantifies the time decay of an option’s value. Theta is usually expressed as a negative number because options tend to lose value over time. A higher theta means that the option’s value will decrease at a faster rate due to time decay, while a lower theta implies a slower rate of time decay.

It’s important to note that delta and theta are just two of the many factors that influence an option’s price. Other factors include gamma, vega, and rho. Traders use these Greek letters to assess and manage the risk associated with their options positions.

Understanding delta and theta can help traders make informed decisions when trading options. By knowing how an option’s price will change in relation to changes in the underlying asset’s price and time decay, traders can adjust their strategies accordingly. Whether you’re a beginner or an experienced trader, having a solid understanding of delta and theta is essential for success in the world of options trading.

Delta is a crucial concept in options trading that represents the sensitivity of an options contract’s price to changes in the price of the underlying asset. It measures the degree to which the option price will move in relation to a one-point change in the underlying asset’s price.

The delta value of an option can range from 0 to 1 for call options and from -1 to 0 for put options. A delta of 0 means the option price will not move at all in response to changes in the underlying asset’s price, while a delta of 1 (or -1 for put options) means the option price will move in perfect correlation with the underlying asset’s price.

The delta value also provides an estimate of the probability that an option will finish in-the-money at expiration. For example, if a call option has a delta of 0.6, it means there’s a 60% chance that the option will finish in-the-money. Conversely, there’s a 40% chance that the option will finish out-of-the-money.

Furthermore, the delta value of an option changes as the underlying asset’s price changes. Call options typically have a positive delta, meaning their value will generally increase when the underlying asset’s price rises. Put options, on the other hand, typically have a negative delta, indicating that their value will generally increase when the underlying asset’s price falls.

It’s important to note that the delta of an option is not constant and can fluctuate. This is because the delta value is influenced by other factors such as time to expiration, implied volatility, and interest rates. These factors can impact the option’s sensitivity to changes in the underlying asset’s price.

Read Also: Mastering Currency Trading Online: Tips and Tricks for Success

Overall, understanding the concept of delta is essential for options traders as it helps them assess the potential profitability and risk of a particular options strategy. By analyzing the delta value, traders can make informed decisions regarding market movements and position themselves accordingly.

Delta is a key concept in options trading that measures the sensitivity of an option’s price to changes in the underlying asset’s price. It quantifies the change in the option price for each $1 movement in the underlying asset’s price. Delta ranges from 0 to 1 for call options and from -1 to 0 for put options.

Read Also: Understanding ATR in Forex Trading: Definition, Calculation, and Application

The value of delta can help traders assess the risk and potential profitability of an options position. A delta of 1 indicates that the option price will move in a 1:1 ratio with the underlying asset, while a delta of 0.5 suggests that the option price will move half as much as the underlying asset. For example, if a call option has a delta of 0.7 and the underlying asset’s price increases by $1, the option price is expected to increase by $0.70.

Deltas can also be interpreted as probabilities. A call option with a delta of 0.7 indicates that there is a 70% chance the option will finish in-the-money at expiration. On the other hand, a put option with a delta of -0.3 suggests a 30% chance of finishing in-the-money. This enables traders to assess the potential profitability of their options positions and make informed decisions.

Delta is not a static value and can change as the underlying asset’s price moves. Gamma, another options Greek, measures the rate at which delta changes in response to changes in the underlying asset’s price. This makes delta a dynamic and important metric for options traders to monitor.

Understanding and utilizing delta is essential for options traders as it provides insights into the risk and potential returns of their positions. By monitoring delta and adjusting options positions accordingly, traders can manage risks, hedge against market movements, and potentially maximize profits in options trading.

Delta is a measure of how much the price of an option will move in relation to a $1 change in the price of the underlying asset.

Delta is calculated as the change in the price of the option divided by the change in the price of the underlying asset.

A positive delta means that the price of the option will increase when the price of the underlying asset increases.

Theta is a measure of the time decay of an option. It indicates how much the price of an option will decrease as time passes.

Exploring D3 Analysis: A Comprehensive Overview D3 (Data-Driven Documents) is a JavaScript library that is widely used for creating dynamic and …

Read Article

Guide on how to become a broker in Cyprus Becoming a broker in Cyprus can be a lucrative and rewarding career choice. However, the process can be …

Read Article

Official Exchange Rate for AUD to EUR If you are planning a trip to Australia or Europe, it’s crucial to know the official exchange rate for AUD …

Read Article

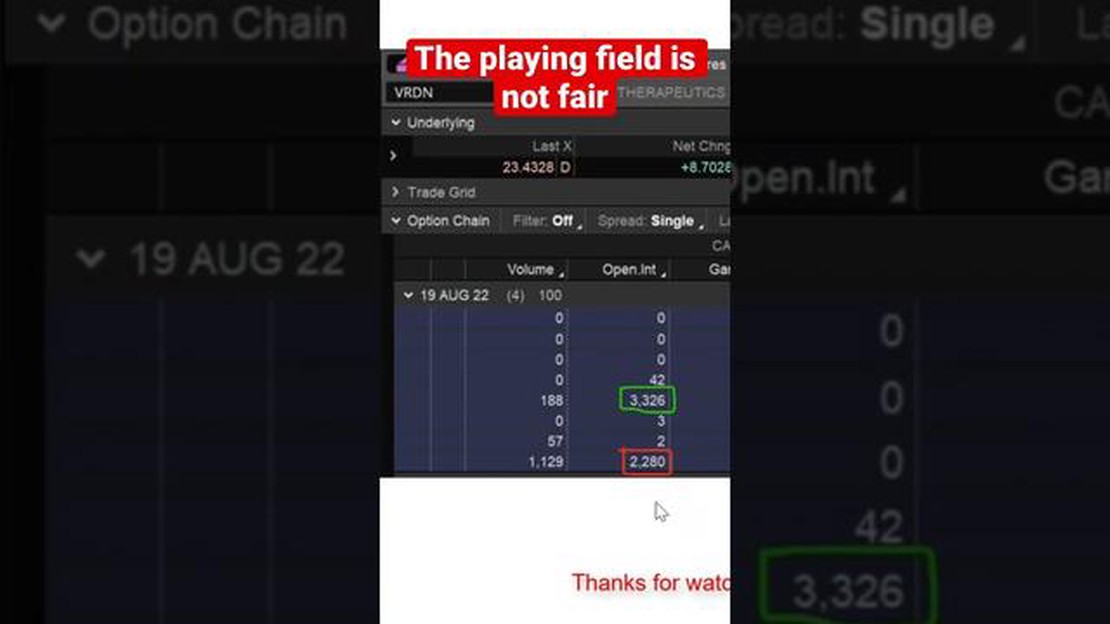

Top Unusual Options Scanner: Which One is the Best? Discover the Best Unusual Options Scanner for Profitable Stock Trading Welcome to our …

Read Article

Best Forex Trading Platforms in Malaysia Forex trading has grown in popularity in Malaysia, with more and more individuals looking to invest in this …

Read Article

Foreign Currency Options Trading Locations Foreign currency options have become an increasingly popular investment tool for traders looking to …

Read Article