Is Kontakt software free or must it be purchased?

Is Kontakt Software Free or Paid? Kontakt is a powerful software sampler developed by Native Instruments, widely used in the music production …

Read Article

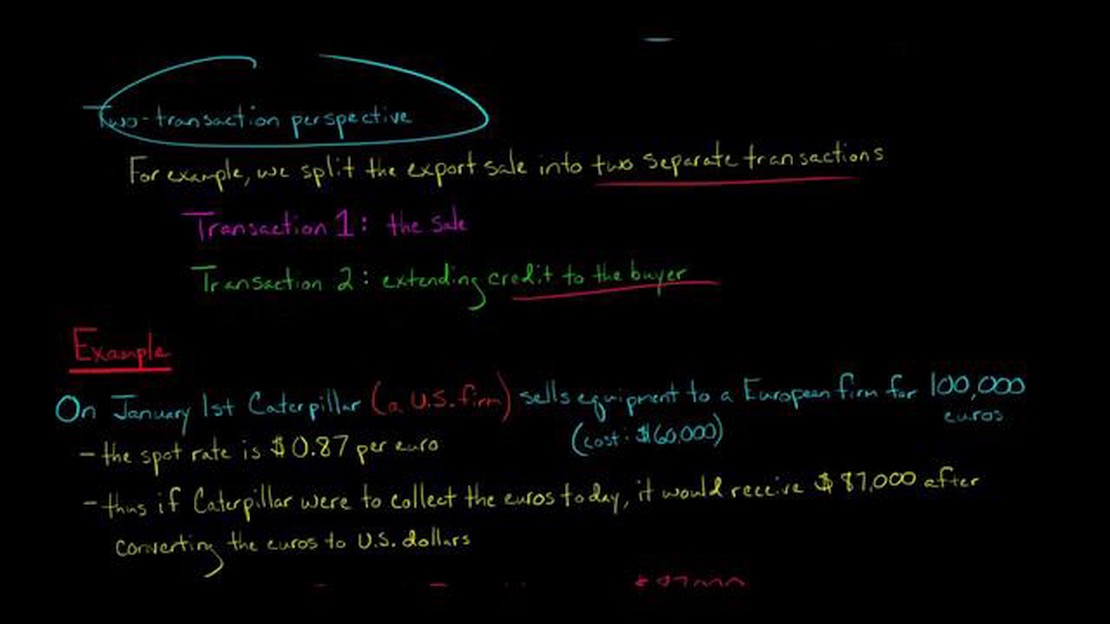

Reporting currency gain or loss can be a complex task, especially for individuals or businesses involved in international transactions. Understanding how to properly report these gains or losses is crucial for accurate financial reporting and compliance with tax laws. This comprehensive guide outlines the key steps and considerations for reporting currency gain or loss.

Step 1: Determine the Transaction Type

Before reporting currency gain or loss, it is important to determine the type of transaction involved. Currency gain or loss can result from various transactions, such as foreign currency exchange, foreign investments, or international sales. Each transaction type may have different reporting requirements, so it is essential to identify the specific transaction and its corresponding reporting rules.

Step 2: Calculate the Gain or Loss

To report currency gain or loss, it is necessary to calculate the amount. This involves determining the exchange rate used for the transaction and comparing it to the rate at the time of the transaction. The resulting difference in value is the gain or loss. It is important to use accurate and up-to-date exchange rates to ensure precise calculations.

Step 3: Determine the Tax Treatment

Once the gain or loss is calculated, it is necessary to determine the tax treatment. Currency gains or losses may be treated differently for tax purposes, depending on various factors such as the nature of the transaction, the tax jurisdiction, and any applicable tax treaties. Consulting a tax professional or referring to tax guidelines can help determine the correct tax treatment for reporting purposes.

Note: This guide provides general information on reporting currency gain or loss. It is always advisable to consult with a tax professional or refer to specific tax guidelines to ensure accurate reporting and compliance with tax laws.

Step 4: Prepare the Tax Forms

Once the gain or loss and its tax treatment are determined, the next step is to prepare the necessary tax forms. This may include forms such as Schedule D, Form 8949, or other specific forms for reporting currency transactions. Carefully review the instructions and guidelines provided with the tax forms to ensure accurate reporting and avoid any penalties or audit risks.

Step 5: File the Tax Return

Finally, include the reported currency gain or loss on the appropriate section of the tax return. Ensure that all necessary forms and schedules are attached, and that the reporting is consistent with other financial statements and disclosures. It is advisable to keep copies of all relevant documents, including exchange rate records and supporting documentation, in case of any future inquiries or audits.

Read Also: Step-by-Step Guide: How to Trade Nigerian Stocks Online

In conclusion, reporting currency gain or loss requires a thorough understanding of the transaction type, accurate calculation, proper tax treatment determination, and meticulous completion of tax forms. By following this comprehensive guide, individuals and businesses can ensure accurate reporting and compliance with tax laws.

When it comes to reporting currency gain or loss, it’s important to have a clear understanding of what this means. A currency gain occurs when you convert one currency into another and the value of the currency you converted into increases. On the other hand, a currency loss occurs when the value of the currency you converted into decreases.

There are several factors that can contribute to currency fluctuations and ultimately result in currency gain or loss. These factors include economic indicators, such as interest rates, inflation rates, and trade balances, as well as market speculation and geopolitical events.

It’s important to note that currency gain or loss is not limited to individuals or businesses involved in international trade. Anyone who engages in foreign currency exchange transactions, such as travelers, investors, or importers and exporters, may be subject to currency gain or loss.

When it comes to reporting currency gain or loss, the Internal Revenue Service (IRS) requires individuals and businesses to include these transactions on their tax returns. The specific forms and reporting requirements may vary depending on the nature and volume of the transactions, so it’s important to consult with a tax professional or refer to IRS guidelines for accurate reporting.

| Reporting Currency Gain or Loss |

|---|

| 1. Determine the amount and date of the currency conversion. |

| 2. Calculate the gain or loss by subtracting the original value of the currency from the converted value. |

| 3. Report the gain or loss on the appropriate tax form, such as Schedule D for individuals or Form 8949 for businesses. |

| 4. Keep detailed records of the currency conversion, including exchange rates and transaction fees, as these may be needed for accurate reporting. |

| 5. Consider consulting with a tax professional to ensure compliance with IRS guidelines and to maximize deductions or credits related to currency gain or loss. |

Read Also: Understanding the Stock Index Signals: Everything You Need to Know

By understanding currency gain or loss and properly reporting these transactions, individuals and businesses can ensure compliance with tax regulations and potentially minimize their tax liabilities. It’s important to stay informed about currency market trends and seek professional advice when necessary to make informed decisions about currency conversion and reporting.

When it comes to taxes, it is important to accurately report any currency gain or loss you may have incurred throughout the year. The Internal Revenue Service (IRS) requires individuals and businesses to report these gains or losses on their tax returns to ensure compliance with tax laws.

If you have engaged in foreign currency transactions, such as buying or selling foreign currency, traveling abroad, or investing in foreign assets, you may have to report any gains or losses associated with these activities. It is crucial to keep detailed records and receipts of these transactions to accurately calculate your currency gain or loss.

To report currency gain or loss on your tax return, you will need to use Form 8949, Sales and Other Dispositions of Capital Assets. This form is used to report the details of your transactions, including the date of acquisition or sale, the cost or basis of the currency, the sale proceeds, and the resulting gain or loss. You will also need to indicate whether the transaction was a short-term or long-term gain or loss.

In addition to Form 8949, you may also need to fill out Form 1040, Schedule D, Capital Gains and Losses. This form is used to summarize the information reported on Form 8949 and calculate your overall capital gain or loss for the year. It is important to accurately complete both forms to avoid any potential penalties or scrutiny from the IRS.

When reporting currency gain or loss on your tax return, it is essential to consult with a tax professional or financial advisor who specializes in international tax matters. They can provide guidance on properly reporting your gains or losses and help you navigate any complex tax laws or regulations.

It is important to note that tax laws and reporting requirements may vary depending on your specific situation and jurisdiction. Therefore, it is crucial to stay updated on the latest tax regulations and consult with a professional to ensure compliance when reporting currency gain or loss on your tax return.

Currency gain or loss refers to the increase or decrease in value of one currency against another currency. It occurs when you buy or sell currencies and the exchange rate fluctuates, resulting in a profit or loss.

To report currency gain or loss on your taxes, you need to keep track of all your foreign currency transactions throughout the year. You will then need to convert the amounts into your local currency and calculate the gain or loss. You report this information on the appropriate tax forms, such as Form 8949 and Schedule D.

Yes, there are certain exemptions and special rules for reporting currency gain or loss. For example, if you are an individual and your total gain or loss from all your transactions is $200 or less, you may not need to report it. Additionally, different rules may apply if you are a trader or a business.

The penalties for failing to report currency gain or loss can vary depending on the country and the specific circumstances. In the United States, for example, the penalties can range from fines to criminal charges. It’s important to consult with a tax professional or review the specific tax laws in your country to understand the consequences of not reporting currency gain or loss.

Is Kontakt Software Free or Paid? Kontakt is a powerful software sampler developed by Native Instruments, widely used in the music production …

Read Article

What is a master password key? In the digital age, where we rely on various online services and platforms for communication, banking, and …

Read Article

Trading Pokemon Black with Black 2: Is it Possible? Are you a fan of the Pokemon franchise? Have you been wondering if you can trade Pokemon between …

Read Article

Understanding the Most Favored Nation (MFN) Trade System The Most-Favored Nation (MFN) trade system is an integral part of the global trading …

Read Article

Current Dollar Selling Rate in Jamaica Get the Latest Updates Are you planning a trip to Jamaica? Want to know the current dollar selling rate? Look …

Read Article

How much money do you have to give Moxxi for her gun in Borderlands 2? In the popular video game Borderlands 2, players are introduced to a wide …

Read Article