Understanding Trading Lots: Explained and Simplified

Understanding Trading Lots: What You Need to Know Trading lots are a fundamental concept in the world of trading. Whether you’re a novice trader or an …

Read Article

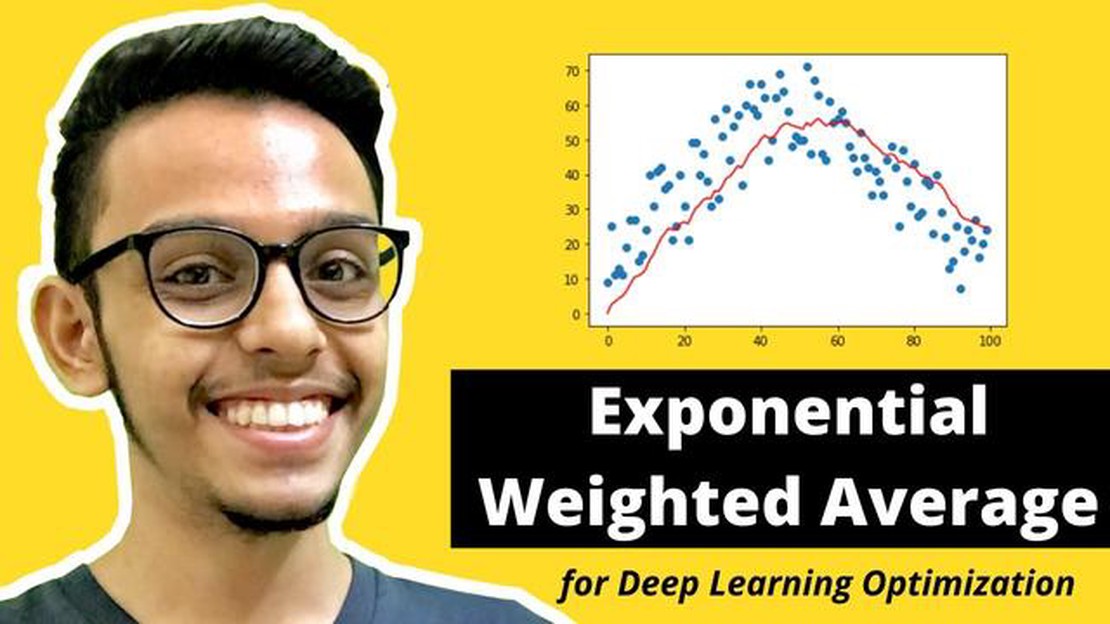

Exponential weighted moving average (EWMA) is a popular statistical method used in time series analysis and forecasting. It is a weighted average calculation in which recent data points are given more weight compared to older data points. EWMA is widely used for smoothing noisy data and filtering out random variations.

Calculating EWMA in Python is fairly straightforward and can be done using the pandas library. Pandas provides a built-in function called .ewm() that allows us to calculate the EWMA of a given time series. Additionally, we can specify the span or alpha parameter to control the weight assigned to each data point.

Using the .ewm() function, we can quickly calculate the EWMA of a column in a pandas DataFrame. This makes it easy to incorporate the EWMA calculation into our data analysis pipeline. By applying EWMA to our data, we can get a smoother representation that highlights the underlying trends and patterns.

Here is a simple example of how to calculate the exponential weighted moving average in Python:

import pandas as pd

data = pd.read_csv(’example.csv')

ewma = data[‘value’].ewm(span=10).mean()

In the above example, we are loading a csv file into a pandas DataFrame and then using the .ewm() function with a span of 10 to calculate the EWMA of the ‘value’ column. The resulting EWMA values are stored in the ’ewma’ variable.

By understanding how to calculate the exponential weighted moving average in Python, you can gain valuable insights from your time series data and make more accurate predictions. EWMA is a powerful tool for smoothing noisy data and uncovering hidden trends, and its implementation in Python is both simple and efficient.

The exponential weighted moving average (EWMA) is a popular statistical technique used to analyze time series data. It is a type of moving average that places more emphasis on recent data points and assigns exponentially decreasing weights to older data points. This means that more recent data points have a greater impact on the average than older ones.

The EWMA is commonly used in finance and economics to analyze stock prices, market indices, and other financial data. It is also used in other fields such as engineering, supply chain management, and epidemiology to analyze trends and patterns in data.

The calculation of the EWMA involves two main components: the smoothing factor and the previous average. The smoothing factor determines the weight assigned to each data point, with higher values giving more weight to recent data. The previous average is the weighted average of previous data points, which helps to smooth out fluctuations and highlight underlying trends.

Read Also: Headquarters of G5 - Where is the global hub located?

The formula for calculating the EWMA is:

EWMA = (1 - α) * previous average + α * current value

Where:

The choice of the smoothing factor depends on the specific problem and data being analyzed. Generally, smaller values of α place more weight on older data points, resulting in a smoother average. Larger values of α place more weight on recent data points, making the average more sensitive to recent changes.

The EWMA is a useful tool for analyzing time series data because it provides a balance between the short-term and long-term trends. By giving more weight to recent data, it captures short-term fluctuations and reacts quickly to changes. At the same time, it also considers the long-term trends by giving some weight to older data points, helping to smooth out noise and highlight underlying patterns.

In conclusion, the exponential weighted moving average is a valuable statistical technique for analyzing time series data. It is widely used across various industries to analyze trends, identify patterns, and make informed decisions based on historical data.

The exponential weighted moving average (EWMA) is a popular method used to calculate a weighted average of a time series data, where more recent data points are given higher weights. It is commonly used in finance and statistics to analyze trends and identify patterns.

To calculate the EWMA in Python, you can use the pandas library, which provides a built-in function called ewm(). The ewm() function takes the parameter “alpha” to specify the decay factor, which defines the weight of each data point.

Read Also: Understanding Forex Options: A Comprehensive Guide for Traders

Here is an example of calculating the EWMA for a given pandas Series:

import pandas as pd# Create a pandas Series with some random datadata = pd.Series([1, 2, 3, 4, 5, 6, 7, 8, 9, 10])# Calculate the EWMA with a decay factor of 0.5ewma = data.ewm(alpha=0.5).mean()print(ewma)

In the example above, the ewm() function is used to calculate the EWMA for the given data Series. The parameter “alpha” is set to 0.5, which means that each data point is given a weight of 0.5 times the weight of the previous data point.

The result, ewma, is a new pandas Series that contains the calculated EWMA values. You can print the result to see the output.

By adjusting the value of the “alpha” parameter, you can control the smoothing factor and the sensitivity of the EWMA to the recent data points. A smaller “alpha” value will give more weight to the historical data, while a larger “alpha” value will give more weight to the recent data.

In conclusion, calculating the exponential weighted moving average in Python is straightforward using the pandas library. By adjusting the decay factor, you can fine-tune the weighting of the data points and analyze the time series data effectively.

The exponential weighted moving average (EWMA) is a statistical calculation that gives more weight to recent data points and less weight to older data points. It is commonly used in finance and time series analysis to track trends and smooth out noise in data.

The exponential weighted moving average is calculated by multiplying each data point by a weight factor, which decreases exponentially as the data gets older. The weighted average is then calculated by summing up the weighted data points and dividing by the sum of the weight factors.

The smoothing factor, also known as the decay factor or alpha, determines the rate at which the weights decrease exponentially as the data gets older. A higher smoothing factor gives more weight to recent data points, while a lower smoothing factor gives more weight to older data points.

Yes, exponential weighted moving average can be used for forecasting future values. The weighted average gives more weight to recent data points, so it is more responsive to recent changes in the data. However, it is important to note that EWMA is a smoothing technique and may not be the most accurate method for forecasting future values in all cases.

Yes, there are several Python libraries that can calculate exponential weighted moving average. Some popular libraries include Pandas, NumPy, and SciPy. These libraries provide functions and methods to easily calculate EWMA for time series data.

An exponential weighted moving average is a type of moving average that assigns more weight to recent data points and less weight to older data points. This is achieved by applying a smoothing factor that determines the contribution of each data point to the moving average.

Understanding Trading Lots: What You Need to Know Trading lots are a fundamental concept in the world of trading. Whether you’re a novice trader or an …

Read Article

The Importance of BCM: Understanding the Significance of Business Continuity Management In today’s fast-paced and ever-changing business landscape, …

Read Article

What country is CAC futures? When it comes to trading financial futures, it’s important to understand where the market originates from. One of the …

Read Article

Which is the best indicator for gold? When it comes to investing in gold, having the right indicator is crucial. Gold is a highly volatile commodity …

Read Article

Forex Trading vs Stocks: Which is Easier to Learn and Master? When it comes to financial markets, two major players stand out: Forex and stocks. Both …

Read Article

How much is $100 in Baku? When traveling to Baku, the capital of Azerbaijan, many tourists wonder how much their money is worth in the local currency. …

Read Article