How to Obtain Forex Data for Analysis: A Comprehensive Guide

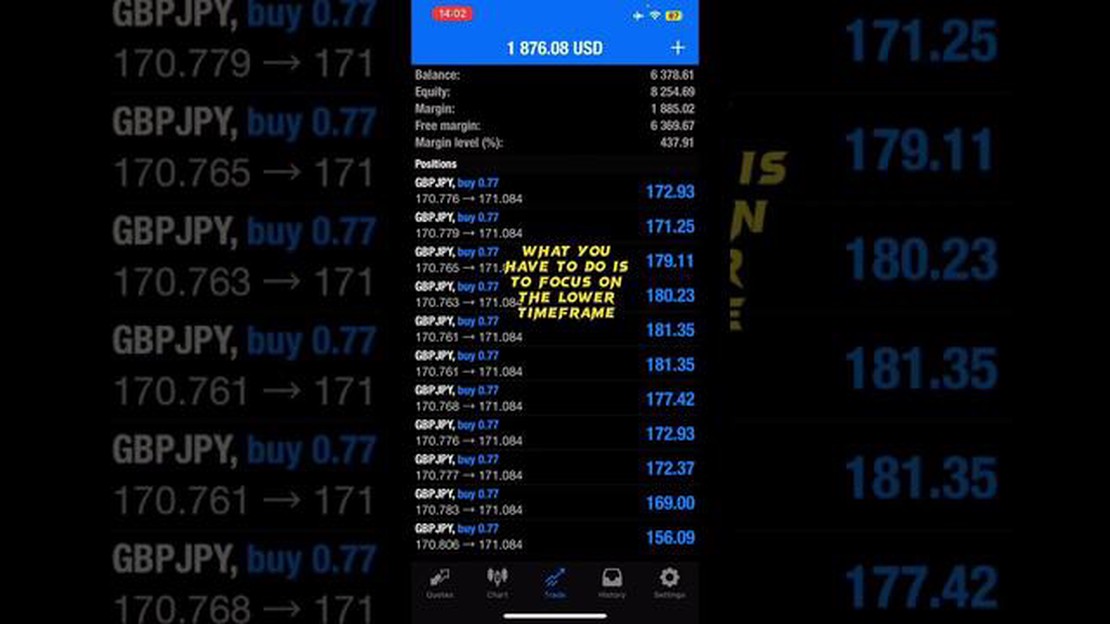

Get Forex Data for Analysis: Step-by-Step Guide When it comes to analyzing the foreign exchange market, having access to accurate and reliable forex …

Read Article

Welcome to our comprehensive guide on ASC 718 10 25 15! Whether you’re an accounting professional or a business owner, understanding ASC 718 10 25 15 is essential for properly accounting for stock-based compensation. In this article, we will provide you with everything you need to know about ASC 718 10 25 15, from its definition to its key provisions and impact on financial statements.

ASC 718 10 25 15, also known as Accounting Standards Codification Topic 718 Section 10 Subsection 25 Subsection 15, is a set of guidelines established by the Financial Accounting Standards Board (FASB) for accounting for stock-based compensation. It specifically addresses the accounting treatment for equity-based compensation arrangements, such as stock options, restricted stock units, and stock appreciation rights.

This accounting standard requires companies to recognize the fair value of stock-based compensation expense on their financial statements. It provides detailed guidance on the measurement, valuation, and timing of the recognition of stock-based compensation expense. By following the principles outlined in ASC 718 10 25 15, companies can ensure accurate and transparent reporting of their stock-based compensation activities.

Understanding and correctly implementing ASC 718 10 25 15 is crucial for companies to comply with accounting standards and provide relevant and reliable financial information to investors and stakeholders. In this article, we will delve into the key provisions of ASC 718 10 25 15, including the determination of fair value, recognition of compensation expense, and the impact on the income statement and balance sheet. Stay tuned to gain a comprehensive understanding of ASC 718 10 25 15 and its implications for financial reporting.

ASC 718, also known as the Accounting Standards Codification 718, is a set of guidelines issued by the Financial Accounting Standards Board (FASB) that specifically pertains to the accounting treatment of share-based payment transactions.

These guidelines were established to provide clarity and consistency in how companies account for stock compensation and other forms of equity-based compensation. ASC 718 aims to ensure that financial statements accurately reflect the economic impact of share-based payment awards, such as stock options, restricted stock units, and employee stock purchase plans.

Under ASC 718, companies are required to measure and recognize the compensation cost associated with share-based payment awards, which includes the fair value of the awards on the grant date. The fair value of the awards is determined through various valuation methods, such as Black-Scholes-Merton, lattice model, or other appropriate methodologies.

One important aspect of ASC 718 is the requirement to expense the cost of share-based payment awards over their vesting period, which is the period of time over which employees become entitled to the awards. This ensures that the expense is recognized as the employees render service to the company and reflects the true cost of the awards.

Read Also: Common Issues and Challenges with Moving Average Calculation

ASC 718 also requires companies to disclose specific information related to share-based payment arrangements in their financial statements. This includes information about the method used to value the awards, the assumptions made in determining their fair value, and the amount of compensation expense recognized in each reporting period.

Overall, ASC 718 provides companies with a clear framework for accounting for share-based payment transactions. Adhering to these guidelines helps ensure transparency and consistency in financial reporting, allowing investors and other stakeholders to make informed decisions based on accurate and comparable financial information.

It is important for companies to stay updated on any changes or updates to ASC 718, as the guidelines may evolve over time. Compliance with ASC 718 is crucial for accurate financial reporting and for demonstrating adherence to the Generally Accepted Accounting Principles (GAAP).

Note: The information provided in this article is for informational purposes only and should not be considered as professional advice. Consult with a qualified accounting professional for assistance with interpreting and applying ASC 718.

ASC 718, also known as Accounting Standards Codification Topic 718, is a set of accounting rules that specifically pertains to stock compensation. This accounting standard provides guidance on how companies should account for and report their stock-based compensation plans, including stock options, restricted stock units (RSUs), and other forms of equity-based compensation.

Under ASC 718, companies are required to measure the fair value of their stock-based compensation awards on the date of grant and recognize the related expense over the requisite service period. The fair value of the awards is typically determined using an option pricing model, such as the Black-Scholes-Merton model or a lattice-based model.

Read Also: How Much Is 0.01 Lot? Explained | Learn Forex Trading Basics

In addition to measuring and recognizing the expense, ASC 718 also requires companies to disclose certain information about their stock-based compensation plans in the footnotes to their financial statements. This includes information such as the assumptions used to calculate the fair value of the awards, the vesting period, and any applicable forfeiture rates.

ASC 718 applies to both public and private companies, although certain practical expedients may be available to private companies. It is important for companies to carefully follow the guidance outlined in ASC 718 to ensure that they are properly accounting for their stock-based compensation and providing accurate and transparent financial reporting.

By understanding the basics of ASC 718, companies can ensure compliance with the accounting standards and provide accurate financial statements to investors and other stakeholders.

ASC 718 stands for Accounting Standards Codification Topic 718. It is a set of accounting rules that provides guidelines for the accounting and reporting of stock-based compensation. ASC 718 requires companies to recognize the fair value of stock options and other equity-based compensation as an expense on their financial statements.

ASC 718 impacts companies that offer stock-based compensation to their employees. Under ASC 718, companies are required to recognize the fair value of this compensation as an expense on their financial statements. This can affect a company’s reported earnings and financial position. It also requires companies to provide additional disclosures in their financial statements related to stock-based compensation.

ASC 718 has several key provisions. Some of the main provisions include: the requirement to recognize stock-based compensation as an expense on the financial statements, the use of fair value to determine the expense, the need for companies to estimate the expected term of stock options, the requirement to measure the compensation cost on the grant date, and the need to provide additional disclosures related to stock-based compensation.

ASC 718 requires companies to provide various disclosures related to stock-based compensation in their financial statements. Some of the key disclosure requirements include: the method used to determine the fair value of stock options, the expected term of stock options, the assumptions used to estimate the fair value, the amount of stock-based compensation expense recognized in each financial statement, and the effect of stock-based compensation on reported earnings.

Get Forex Data for Analysis: Step-by-Step Guide When it comes to analyzing the foreign exchange market, having access to accurate and reliable forex …

Read Article

When was USD equal to CAD? The exchange rate between the United States dollar (USD) and the Canadian dollar (CAD) has fluctuated throughout history, …

Read Article

Comparison of straddle, strangle, and other options strategies A straddle and a strangle are two popular options trading strategies that involve …

Read Article

Should You Use a Stop Loss on Options? Options trading can be a highly lucrative investment strategy, allowing investors to leverage their capital and …

Read Article

Understanding Credit Spread Strategies In the world of investing, credit spread strategies are becoming increasingly popular and are being employed by …

Read Article

Which leverage is better 1 100 or 1 30? In the world of trading, leverage is a powerful tool that allows traders to amplify their potential profits. …

Read Article