Is Golden Cross a Reliable Trading Strategy? Analyzing its Effectiveness

Is Golden Cross a good strategy? When it comes to trading strategies, the golden cross is one that has gained significant attention in the financial …

Read Article

Forex trading, also known as foreign exchange trading, is a popular investment option for individuals and businesses looking to profit from fluctuations in currency exchange rates. However, one important aspect that traders need to consider is taxes. Are taxes required for forex trading? The answer to this question largely depends on the country you reside in and the specific tax regulations in place.

In many countries, forex trading falls under the category of capital gains or investment income. This means that any profits you make from forex trading may be subject to taxes. However, the tax rates and rules regarding forex trading can vary significantly from country to country. For example, some countries may tax forex trading as ordinary income, while others may provide certain tax exemptions or benefits for forex traders.

It is important for forex traders to consult with a tax expert or accountant who is familiar with the tax laws in their country. They can provide guidance on the specific tax obligations related to forex trading and help ensure that traders comply with all applicable laws and regulations. Failure to report forex trading income or pay the required taxes can result in penalties, fines, or even legal consequences.

Additionally, it is worth noting that tax regulations and laws can change over time. What may be considered tax-exempt or subject to certain tax benefits today may be different tomorrow. Traders should stay informed about any updates or changes to tax laws that may affect their forex trading activities. By staying compliant with tax regulations, traders can trade with peace of mind and avoid any potential legal issues.

While taxes are an important consideration for forex traders, it is essential to remember that they are not the only factor to consider. Traders should also pay attention to other aspects such as risk management, market analysis, and trading strategies to achieve long-term success in forex trading.

Forex trading can be an exciting and potentially profitable venture, but it’s important to understand the tax implications before you dive in. The tax treatment of forex trading can vary depending on your country of residence, so it’s crucial to consult with a tax professional or accountant to ensure compliance with local regulations.

In most countries, forex trading is treated as a type of investment activity, and any profits made are subject to taxation. You will need to report your forex trading income and gains on your annual tax return. It’s important to keep track of all your trading activity, including profits, losses, and expenses, so that you can accurately calculate your taxable income.

The tax rate applied to forex trading profits can vary depending on several factors, including the duration of your trades, the amount of income earned, and the specific tax laws in your jurisdiction. Some countries may have a separate tax rate for short-term capital gains or trading income, so it’s important to be aware of any distinct tax rules that may apply to forex trading.

In addition to income tax, forex traders may also be subject to other taxes, such as capital gains tax or stamp duty. These additional taxes can further impact your overall tax liability, so it’s important to understand all the potential tax obligations associated with forex trading in your country.

Read Also: Is Smart Trader free? Learn about the pricing options and features

It is worth noting that tax regulations for forex trading can be complex and can change over time, so it’s important to stay up to date with any changes in legislation that may affect your tax obligations. Consulting with a tax professional can help you navigate these complexities and ensure that you are in compliance with all relevant tax laws.

In conclusion, understanding the tax implications of forex trading is essential for any trader. By consulting with a tax professional and keeping detailed records of your trading activity, you can ensure that you are fulfilling your tax obligations and minimizing your tax liability.

Read Also: Is It a Good Time to Trade Forex? Expert Advice and Insights

When it comes to forex trading and taxes, there are several important things you need to know:

Remember, tax regulations vary from country to country, so it’s crucial to consult with a tax professional who specializes in forex trading to ensure you comply with all applicable laws and regulations.

Yes, taxes are required for forex trading. Profits from forex trading are subject to taxation in most countries. Traders must report their gains and losses to the relevant tax authorities.

The taxes you need to pay for forex trading depend on your country of residence. In some countries, such as the United States, you may need to pay capital gains tax on your forex profits. Other countries may have different tax rates or classify forex trading as regular income. It is recommended to consult with a tax professional or accountant to understand your specific tax obligations.

In many countries, if you’re making losses from forex trading, you may not be required to pay taxes on those losses. However, it is still important to report your losses to the tax authorities and follow the necessary procedures to claim them as deductions. Again, consulting with a tax professional is recommended to ensure compliance with tax regulations.

If you fail to pay taxes on your forex trading profits and you are caught by the tax authorities, you may be subject to penalties and fines. These penalties can vary depending on the country and the amount of unpaid taxes. It is always best to fulfill your tax obligations to avoid any legal consequences.

Some countries provide tax advantages for forex traders. For example, in certain jurisdictions, forex traders may be eligible for lower tax rates or certain deductions related to their trading activities. However, these advantages are specific to each country and may require meeting certain criteria. It is advisable to consult with a tax professional to explore any available tax advantages for forex trading in your jurisdiction.

Is Golden Cross a good strategy? When it comes to trading strategies, the golden cross is one that has gained significant attention in the financial …

Read Article

Simple Steps to Download MT4 on Android MetaTrader 4 (MT4) is a popular trading platform among forex traders, known for its advanced features and …

Read Article

Ownership of Tadawul: Exploring the Key Stakeholders and Investors The Tadawul, also known as the Saudi Stock Exchange, holds a crucial role in the …

Read Article

What kind of material is FOREX? FOREX stands for Foreign Exchange, and it refers to the global market where currencies are traded. This decentralized …

Read Article

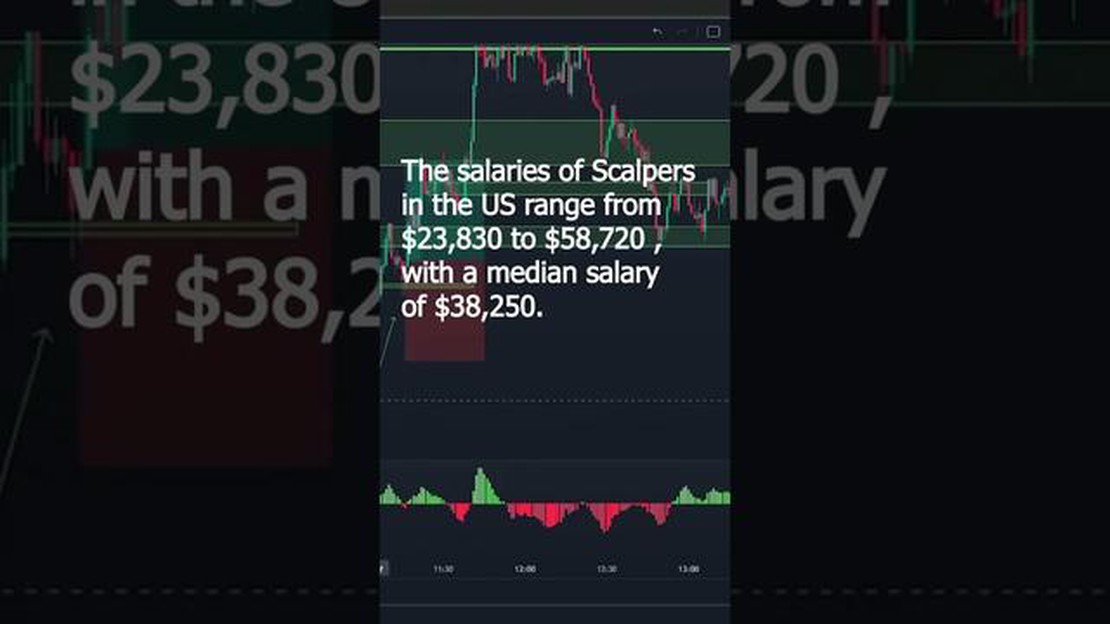

How much does the average scalper make? Scalping is a controversial practice where individuals buy tickets or merchandise at face value and then …

Read Article

Discover the Best EMA Crossover Strategy for Optimal Results When it comes to trading in the financial markets, having a solid strategy is key to …

Read Article